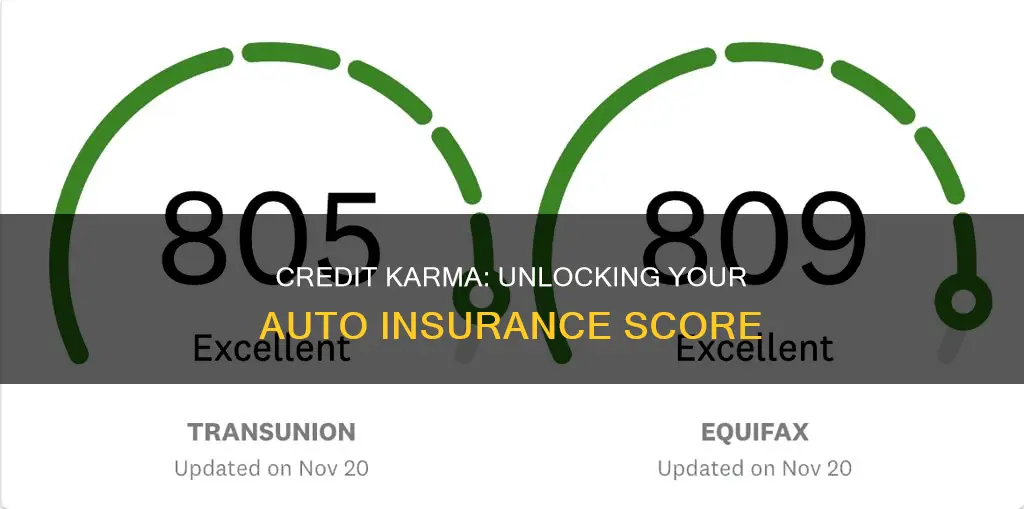

Credit Karma offers a free service that allows users to check their auto insurance scores. These scores are used by auto insurance companies to assess the risk of insuring an individual by predicting the likelihood that they will file a claim. A person's auto insurance score is calculated using information from their credit reports, and it can influence their premium rate. Credit Karma provides users with access to their auto insurance scores from TransUnion, which typically range from 200 to 997. A good auto insurance score is usually considered to be 770 or higher, according to TransUnion. By understanding their auto insurance score, individuals can work towards improving their credit health and potentially lowering their insurance premiums.

| Characteristics | Values |

|---|---|

| What is an auto insurance score? | A numerical score used to predict the likelihood of a person having an accident or making a claim. |

| How is it calculated? | Based on information in a person's credit reports, including payment history, outstanding debt, length of credit history, pursuit of new credit, and mix of credit experience. |

| How does it affect insurance rates? | The better the insurance score, the lower the auto insurance rate. A poor insurance score may result in a higher insurance rate. |

| How to improve it? | Make all debt payments on time, keep credit utilization low, and have numerous accounts in good standing. |

| How to find it on Credit Karma? | Credit Karma provides free access to auto insurance scores from TransUnion. |

Explore related products

What You'll Learn

![]()

How auto insurance scores are calculated

Auto insurance scores are ratings based on information from credit reports that insurers use to estimate how likely drivers are to file a claim. While auto insurance scores are based on your credit history, they are not based on your driving history.

Auto insurance scores are calculated from information on your credit reports. They are used to predict the likelihood that you’ll have an accident or file a claim. Car insurers use auto insurance scores as one of many factors to determine how much you’ll pay for car insurance in states where that is allowed.

Each company uses its own methodology to interpret the credit information that builds your insurance score, so exact insurance score ranges and how they affect rates are unknown. However, some insurers purchase credit-based insurance scores from companies like FICO. FICO weighs the following factors to determine its auto insurance scores:

- Payment history (roughly 40%)

- Outstanding debt (roughly 30%)

- Length of credit history (roughly 15%)

- Pursuit of new credit (roughly 10%)

- Mix of credit experience (roughly 5%)

Your auto insurance scores are calculated based on the information in your credit reports. So your credit information could potentially have an impact on your auto insurance rates. That said, your auto insurance scores aren’t directly tied to your credit scores. While both are calculated using information from the same source, they aren’t technically related.

However, data shows that your credit scores and auto insurance rates correlate. According to The Zebra’s “The State of Auto Insurance Report for 2020,” drivers with poor credit scores (300 to 579) pay more than twice as much for their auto insurance compared to people with exceptional credit scores (800 to 850). Additionally, improving from one credit tier to the next, such as from poor to average, can save drivers up to 19% per credit tier each year, the report says.

Calculating Composite Auto Insurance Rates: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How to improve your auto insurance score

Auto insurance scores are numerical scores used to predict the likelihood that you’ll have an accident or make a claim. They are calculated based on information in your credit reports, including your credit history, and are used by car insurers to determine how much you’ll pay for car insurance.

A good auto insurance score can benefit your insurance rate, while a bad one could mean you pay more each month. If your auto insurance score is lower than you would like, there are several things you can do to improve it:

- Get a credit report: You can pull your credit report for free once a year from the three main reporting bureaus: Equifax, Experian, and TransUnion. Reviewing your credit report will give you a good basis for understanding your current credit score and where you can improve.

- Pay bills on time: This is an easy way to improve your credit score and, in turn, your auto insurance score. Set reminders or use sticky notes to ensure you never miss a bill payment.

- Avoid opening too many credit accounts at once: Opening multiple credit accounts in a short time frame can make you look like a risky borrower and hurt your insurance score.

- Keep accounts open: Credit accounts that have been open for a long time demonstrate stability and financial responsibility. Keep your oldest credit accounts open to show a long-established track record.

- Keep outstanding balances low: Using some credit is good for your auto insurance score. Aim to use 20-30% of your available credit. This sweet spot shows you are using credit wisely.

- Improve your driving score: Your driving behaviour can also impact your auto insurance rates. You can improve your driving score by focusing on speed management, safe driving hours, vehicle handling, and focused driving.

Canceling Geico Auto Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How auto insurance scores affect your insurance rate

Auto insurance scores are numerical scores used to predict the likelihood of a driver having an accident or filing a claim. They are calculated from information on a driver's credit reports and are used by car insurers to determine how much the driver will pay for car insurance.

The better your insurance scores are, the lower your auto insurance rate will typically be. Conversely, if your insurance scores are poor, your auto insurance rate will likely be higher. It's worth noting that insurance companies can vary in their use of "low score" and "high score" to refer to positive scoring.

In addition to insurance scores, insurance companies consider factors like the age, make and model of your vehicle, miles driven per year, age or driving experience, and accident or claims history.

While auto insurance scores can affect your insurance rate, it's important to note that they are not the only factor. Other factors, such as driving behaviour, can also impact your insurance rate. For example, Credit Karma's Drive Score feature monitors your driving behaviour and provides personalized discounts based on safe driving practices such as speed management, safe driving hours, vehicle handling, and focused driving.

Additionally, certain states have banned the use of credit when calculating insurance rates, including California, Hawaii, Massachusetts, and Michigan. In these states, insurance companies base rates on factors such as driving record, location, and other characteristics.

Lyft Auto Insurance: Claims and Denials

You may want to see also

Explore related products

![]()

How to access your auto insurance score

Auto insurance scores are numerical scores used to predict the likelihood of a driver having an accident or making a claim. They are calculated using information from credit reports and can influence the premium rate.

As a Credit Karma member, you can access your auto insurance score for free. This score is provided by TransUnion and typically ranges from 200 to 997. It's worth noting that Credit Karma also provides free VantageScore 3.0 credit scores from TransUnion and Equifax, as well as free credit reports from these bureaus.

To access your auto insurance score on Credit Karma, follow these steps:

- Sign up for a Credit Karma account if you haven't already.

- Log in to your Credit Karma account.

- Navigate to the "Auto Insurance Score" section. This may be found under a specific tab or menu dedicated to scores and reports.

- Review your auto insurance score provided by TransUnion.

It's important to note that Credit Karma may not be the only source for your auto insurance score. The specific scoring model and formula used can vary across different companies and insurers. For example, FICO offers its own auto insurance scoring model, which weighs factors such as payment history, outstanding debt, and length of credit history. If you're particularly interested in your FICO auto score, you may need to purchase access through FICO directly.

Additionally, keep in mind that auto insurance scores are just one factor in determining insurance rates. Other factors, such as age, vehicle details, driving experience, and claims history, also play a significant role in calculating insurance premiums.

Commercial Auto Insurance: A Multi-Billion Dollar Industry

You may want to see also

Explore related products

![]()

How auto insurance scores differ from credit scores

Auto insurance scores and credit scores are calculated differently and used for different purposes. While both are numerical scores, they are calculated using different methodologies and weightings.

Auto insurance scores are used to predict the likelihood that you will have an accident or make a claim. They are calculated from information on your credit reports, but they are not directly tied to your credit scores. While your credit information can impact your auto insurance rates, your auto insurance scores are based on the interpretation of your credit information by each auto insurance company.

Credit scores, on the other hand, are a measure of creditworthiness and are used to determine your eligibility for loans, credit cards, and other financial products. Credit scores are calculated based on factors such as payment history, credit history length, credit mix, and pursuit of new credit.

Factors Affecting Auto Insurance Scores

Auto insurance scores are calculated using information from your credit reports, including payment history, outstanding debt, length of credit history, pursuit of new credit, and mix of credit experience. These factors are weighted differently by different companies, resulting in varying auto insurance scores. For example, FICO weighs payment history at roughly 40% and outstanding debt at roughly 30%.

Impact of Auto Insurance Scores on Rates

Auto insurance scores can affect your insurance rates, with higher scores potentially resulting in lower rates. This is because insurers assume that individuals with higher auto insurance scores are less likely to file a claim. However, the impact of auto insurance scores on rates varies between states, and some states have banned the use of credit information in calculating insurance rates.

Improving Your Auto Insurance Score

To improve your auto insurance score, you can make all your debt payments on time, keep your credit utilization low, and maintain numerous accounts in good standing. Keeping old lines of credit open and managing your credit inquiries can also positively impact your score.

Understanding Commercial Auto Insurance: Is Your Short Bus Covered?

You may want to see also

Frequently asked questions

Auto insurance scores are numerical scores used to predict the likelihood that you’ll have an accident or file a claim. They are calculated from information on your credit reports.

As a Credit Karma member, you can access your auto insurance score from TransUnion. You can download the free Credit Karma app to monitor your driving and let you know if you qualify for a personalized discount.

A good score is usually around 770 or higher, according to TransUnion.

If your scores are lower than you’d like, there are a few things you can do, or avoid doing, to help improve them. Making all of your debt payments on time, keeping your credit utilization down, and having numerous accounts in good standing can help your auto insurance scores.