Mortgage insurance is a type of insurance that lenders use to offset the risk of lending to borrowers who have made a down payment of less than 20% of the purchase price of the home. It is also typically required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. There are several types of mortgage insurance, including borrower-paid, single-premium, lender-paid, split-premium, and federal home loan premium. The cost of mortgage insurance varies depending on the type of loan and the borrower's credit score. It is important to note that mortgage insurance protects the lender and increases the cost of the loan for the borrower.

| Characteristics | Values |

|---|---|

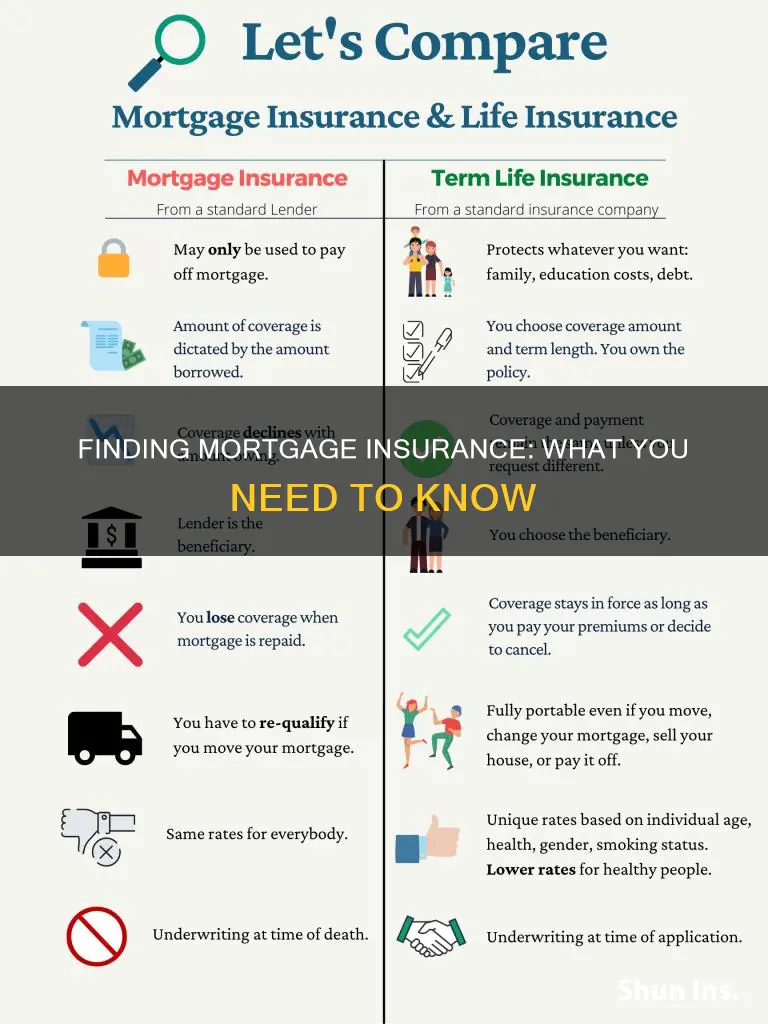

| Who does mortgage insurance protect? | The lender, not the borrower. |

| Who needs mortgage insurance? | Those who borrow with a down payment of less than 20%. |

| Who provides mortgage insurance? | Private companies, FHA, USDA. |

| How is mortgage insurance paid? | Monthly, upfront, or a hybrid of both. |

| Can mortgage insurance be canceled? | Yes, when the mortgage balance reaches 80% of the home's value. |

| How much does mortgage insurance cost? | $30 to $70 per month for each $100,000 borrowed; 0.46% to 1.5% of the loan amount. |

Explore related products

$10.81 $17.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI is arranged by the lender and provided by private insurance companies. It protects the lender and covers their losses if the borrower fails to make loan payments. It does not protect the borrower, and foreclosure may still occur if payments are missed.

PMI can be paid in different ways. It can be paid upfront at closing, with monthly payments, or a combination of both. It is generally paid monthly, with little to no initial payment at closing. You can request to cancel PMI when your mortgage balance reaches 80% of your home's value. Federal law dictates that your lender must automatically end PMI when the loan-to-value (LTV) ratio drops to 78%, or when you are one month past the midpoint of your loan term.

PMI can help you qualify for a loan that you may not otherwise be eligible for. However, it increases the overall cost of your loan. Before agreeing to a mortgage, ask lenders about their PMI choices and calculate the total costs to determine the best option.

Stay Vigilant: Report Health Insurance Fraud

You may want to see also

Explore related products

![]()

When PMI is required

Private mortgage insurance (PMI) is a type of insurance that is usually required when homebuyers make a down payment of less than 20% of the home's value. PMI is designed to protect the lender in the event that the buyer defaults on their loan. This protection is important because it is riskier for a lender to provide a mortgage with a low down payment. PMI is typically required for conventional loans, but it is important to note that other types of loans, such as Federal Housing Administration (FHA) loans, might have their own mortgage insurance requirements.

When taking out a conventional loan, if you are able to make a down payment of 20% or more, you can avoid the need for PMI. This is because a larger down payment reduces the risk for the lender, and the additional protection of PMI is not necessary. However, it is important to note that even with a 20% down payment, some lenders may still require PMI, especially if you are refinancing a conventional loan and your equity is less than 20% of the value of your home.

The requirement for PMI is based on the loan-to-value (LTV) ratio, which is calculated by dividing the loan amount by the appraised value of the property. If the LTV ratio is greater than 80% (meaning the down payment is less than 20%), PMI is typically required. This threshold may vary depending on the lender and other factors, but 20% is generally considered the standard cutoff.

PMI can be paid in different ways, including monthly premiums, a one-time upfront payment at closing, or a combination of both. The cost of PMI varies and is typically calculated as a percentage of the mortgage loan amount. It is important to consider the additional cost of PMI when budgeting for a home purchase, as it increases the overall cost of the loan.

While PMI is an additional expense, it can be beneficial for homebuyers who do not have a 20% down payment. By paying for PMI, homebuyers can still qualify for a loan and purchase a home, even if they have not saved up the full 20%. This provides an opportunity for homebuyers to enter the market sooner, rather than waiting years to accumulate a large down payment.

Indiana Farmers Insurance: Understanding the Reach and Service Network

You may want to see also

Explore related products

![]()

How much PMI costs

The cost of private mortgage insurance (PMI) varies depending on several factors, including the down payment amount, the homebuyer's credit score, debt-to-income ratio, and loan-to-value ratio. Generally, PMI is required if you put down less than 20% on a conventional home loan, and it ranges from 0.2% to 2% of your loan amount per year.

For example, if you have a 15% down payment and an excellent credit score, your PMI costs will likely be lower than someone with a 5% down payment and an average credit score. PMI fees typically range from 0.46% to 1.5% of the original loan amount per year, or between $115 and $375 per month on a $300,000 mortgage.

Borrowers with lower credit scores, high debt-to-income ratios, and smaller down payments will typically pay higher PMI rates. Building your credit score, reducing debt, and increasing your down payment can help lower your PMI costs.

Additionally, the type of mortgage you have can impact your PMI rate. Adjustable-rate mortgages may have higher PMI rates than conventional loans due to the added risk.

It's important to note that PMI is a temporary cost, and it can be canceled once you've built up enough equity in your home.

VSP Eye Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Cancelling PMI

Private mortgage insurance (PMI) is an additional monthly cost that is added to your conventional loan if you bought a home with less than 20% down. It is not to be confused with homeowners insurance, which provides financial protection from damages to your home. PMI protects the lender if the buyer stops making loan payments.

There are several ways to cancel PMI:

Automatic Termination

According to the Homeowners Protection Act of 1998, lenders or servicers must automatically cancel PMI when the mortgage's loan-to-value (LTV) ratio reaches 78% of the home's purchase price, or the month after the midpoint of your loan's term, whichever comes first. The midpoint of your loan's amortization schedule is halfway through the original full term of your loan. For example, for 30-year loans, the midpoint is after 15 years.

Request PMI Cancellation

You can request to cancel PMI when your loan-to-value (LTV) ratio falls below 80% of the property's original value. You may have to submit a formal request to your loan provider, along with documentation such as proof of home value and a solid payment history.

Refinance

With rising home values, you may have the equity required to refinance and avoid paying PMI. You may also want to refinance from an FHA to a conventional loan, eliminating your MIP.

Pay Down Your Mortgage Earlier

If you are in a comfortable financial position, consider making additional mortgage payments to accelerate the reduction of your mortgage balance. This will help you reach the 80% LTV ratio required for PMI cancellation sooner.

Reappraise Your Home

You can request a professional appraisal of your home to determine its current market value. If you have owned the home for at least five years and your loan balance is no more than 80% of the new valuation, you can ask for PMI cancellation. If you've owned the home for at least two years, your remaining mortgage balance must be no greater than 75%.

It's important to note that the specific rules and regulations regarding PMI cancellation may vary depending on your lender and the type of mortgage you have. Always consult with your lender or a financial professional for advice specific to your situation.

Reporting Insurance Fraud: What You Need to Know

You may want to see also

Explore related products

![]()

Types of PMI

Private mortgage insurance (PMI) is a type of insurance that lenders use to offset risk. It is typically required when a buyer makes a down payment of less than 20% of the home's value. It is important to note that PMI protects the lender, not the borrower, in case the buyer stops making loan payments.

- Borrower-paid mortgage insurance (BPMI): This is the most common type of PMI. The cost of PMI is added to the borrower's monthly mortgage payment. This type of PMI is typically paid until the borrower achieves 20% equity in their home.

- Single-premium mortgage insurance: This type of PMI requires borrowers to make a one-time payment at the time of closing, rather than making monthly payments.

- Lender-paid mortgage insurance (LPMI): With LPMI, the lender initially covers the cost of the PMI, but the borrower's mortgage rate is slightly higher to compensate for this. LPMI can result in lower down payments and monthly payments. However, it cannot be removed from the loan, regardless of the equity in the home.

- Split-premium mortgage insurance: This type blends elements of BPMI and single-premium mortgage insurance. The borrower makes an upfront payment at closing and then continues to make monthly payments. Split-premium mortgage insurance offers flexibility and can help reduce the cash needed at closing.

- Federal home loan mortgage insurance premium (MIP): This type of PMI is associated with loans backed by the Federal Housing Authority (FHA). FHA-backed loans typically have lower down payments, closing costs, and credit score requirements, making home ownership more accessible. However, the lower requirements can also mean higher risk for lenders.

**A Safety Net for Farmers: Exploring Crop Fire Insurance**

You may want to see also

Frequently asked questions

Mortgage insurance, also known as private mortgage insurance (PMI), lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be eligible for.

Mortgage insurance is typically required when you put down less than 20% on a conventional loan. It is also required for Federal Housing Administration (FHA) loans and U.S. Department of Agriculture (USDA) loans.

The cost of mortgage insurance varies depending on the type of loan and your credit score. It typically costs $30 to $70 per month for every $100,000 borrowed.

There are several ways to pay for mortgage insurance, including borrower-paid, single-premium, lender-paid, and split-premium. With borrower-paid mortgage insurance, the cost of PMI is added to your monthly mortgage payment. Single-premium mortgage insurance requires a one-time upfront payment, while lender-paid mortgage insurance results in a higher interest rate on the loan. Split-premium mortgage insurance involves paying a larger upfront fee and the remainder with your monthly payment.

Yes, you can request to cancel your mortgage insurance when your mortgage balance reaches 80% of your home's value. Lenders are required to cancel it when your mortgage balance drops to 78% of your home's original value or once you are halfway through your loan term, whichever comes first.