When determining your total mortgage payment, it's important to consider all the costs involved, including insurance and taxes. The monthly mortgage payment typically constitutes the bulk of the financial costs associated with owning a house, but there are other significant expenses to keep in mind. These costs can be divided into two categories: recurring and non-recurring. Recurring costs, such as property taxes, home insurance, HOA fees, and other expenses, tend to increase over time due to inflation. Non-recurring costs, while not as frequent, can be substantial and include upfront expenses like closing costs, attorney fees, property transfer taxes, and more. Additionally, your monthly mortgage payment depends on various factors, including the purchase price, down payment, interest rate, loan term, and property taxes and insurance. Understanding these components and utilising online mortgage calculators can help you make informed decisions about your mortgage payments and overall financial planning.

| Characteristics | Values |

|---|---|

| Down payment | The portion of the home's price that is not financed with a mortgage. |

| Loan amount | The amount borrowed from a lender or bank, i.e., the purchase price minus the down payment. |

| Interest | What the lender charges to borrow the principal or loan amount, expressed as an annual percentage. |

| Property taxes | The tax on a home levied by the city, county, or municipality, paid for as long as the owner owns the property. |

| Homeowners insurance | An insurance policy that covers damage and financial losses to the property and possessions. |

| Mortgage insurance | Required if the down payment is less than 20% of the home's purchase price, added to monthly payments. |

| HOA fees | Monthly dues paid to a homeowners association, which manages planned neighbourhoods or condo communities. |

| Amortization | The ability to input extra payments to decide whether to prepay the mortgage and by how much. |

| Debt-to-income ratio | The ratio of monthly debt payments to monthly pre-tax income, helping lenders understand the borrower's financial capacity. |

Explore related products

What You'll Learn

![]()

Property taxes

The assessed value may not always represent the full market value, as some jurisdictions apply an assessment ratio, which is a percentage of the property's fair market value. This helps determine the taxable value, which is then used to calculate the property tax due. The taxable value is influenced by factors such as depreciation, improvements, renovations, and access to public services.

The property tax rate, often called the mill levy or mill rate, is determined by local authorities and reflects the amount of tax owed per $1,000 of assessed property value. This mill rate combines all local rates from the county, city, and school district. Different taxing entities, such as school districts, fire departments, and local governments, may have different mill rates.

To calculate your property tax, multiply your assessed home value by the local tax rate or mill rate. For example, if the taxable value is $300,000 and the mill rate is 10, the property tax would be:

Property tax = (taxable value / 1,000) x mill rate

Property tax = ($300,000 / 1,000) x 10 = $3,000

Keep in mind that property taxes are usually paid monthly along with your mortgage payment. You can use online mortgage calculators to estimate your monthly mortgage payments, including property taxes. These calculators allow you to input your annual property tax, home insurance, and other factors to determine your total monthly payment.

Independent Adjusters: Worth the Cost?

You may want to see also

Explore related products

![]()

Home insurance

When calculating your insurance premium, insurance companies take into account several factors, including:

- Your state

- Credit tier (in most states)

- Dwelling coverage limit

- Construction year

- Deductible

- Claims history

- ZIP code

The dwelling coverage limit is the cost to completely rebuild your home and is one of the most important parts of your policy. The coverage you have for other structures on your property and for your personal belongings is set based on a percentage of your dwelling limit. Typically, you need enough dwelling coverage to pay the cost of completely rebuilding your home. An insurance agent can help you estimate this amount.

Your deductible is the amount of damage you agree to cover out of pocket in the event of a claim. Higher deductibles usually result in lower premiums, while lower deductibles yield higher premiums.

You can use online home insurance calculators to get an estimate of your costs. It is recommended to get at least three quotes to find the most competitive one. Make sure each quote has similar deductibles and coverage limits.

If you have a mortgage, you can choose to have your lender pay your homeowners insurance bill through your escrow account. Otherwise, you will need to pay the bill yourself, either in full or in installments.

Enhanced Title Insurance: Is the Extra Cost Worthwhile?

You may want to see also

Explore related products

$16.53 $22.99

![]()

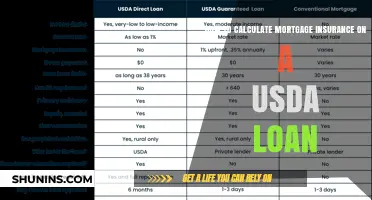

Mortgage insurance

There are different types of loans that require mortgage insurance, including conventional loans, Federal Housing Administration (FHA) loans, and U.S. Department of Agriculture (USDA) loans. For FHA loans, you pay mortgage insurance premiums to the FHA, and it's required regardless of your credit score. USDA loans are similar but tend to be cheaper. For conventional loans, your lender may arrange mortgage insurance with a private company, and the rates depend on factors like your down payment amount and credit score.

In some cases, you can avoid paying mortgage insurance by reaching 20% equity in your home, which is when you can request to remove PMI. Additionally, if you obtain a Department of Veterans' Affairs (VA)-backed loan, there is no monthly mortgage insurance premium, although you pay an upfront "funding fee" that can be rolled into your mortgage.

When considering mortgage insurance, it's important to review your options carefully and decide based on your financial situation and needs. It is a valuable tool to ensure your family is not burdened with debt in the event of unforeseen circumstances.

Understanding Mortgage Clauses in Insurance Policies

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

HOA fees

HOA, or Homeowners Association, fees are monthly payments made to the homeowners association. HOA fees are used to cover the costs of maintaining common-use amenities in a community. The amount of the fees is determined by the HOA board of directors, which is made up of homeowners. HOA fees are typically billed directly and are not added to the monthly mortgage payment.

The fees cover a range of items, including basic maintenance, shared utilities, and insurance. For example, in communities with single-family homes, HOA fees may pay for landscaping, road maintenance, and snow removal. In condominium buildings, HOA fees may be used for maintaining lobbies, elevators, swimming pools, and parking spaces.

In addition to these, HOA fees may also include contingency funds for emergencies, natural disasters, or unexpected costs. They may also cover the cost of engaging professionals to manage the community optimally.

The national average monthly HOA fee in the United States is $191, according to the 2021 American Housing Survey. However, most Americans paid between $200 and $300 per month. It's worth noting that these fees can fluctuate from year to year and are determined by the association's budget for the year.

Jewelry Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Down payment

A down payment is a lump sum of cash paid upfront when purchasing a home. It is separate from closing costs and is typically expressed as a percentage of the total cost of the home, with the remainder covered by a mortgage. The down payment amount varies depending on the buyer's finances, the type of loan, and the location, typically ranging from 3% to 20% or more. Some mortgage programs, such as those for first-time homebuyers, do not require any down payment at all.

The down payment directly impacts the interest rate and monthly payments on the mortgage loan. A larger down payment reduces the loan amount, resulting in lower monthly payments and less interest paid over the life of the loan. For example, consider a $100,000 loan at a 5% interest rate, which incurs $5,000 in interest in the first year. With a $20,000 down payment, the loan amount decreases to $80,000, reducing the first-year interest to $4,000. Additionally, a higher down payment can eliminate the need for private mortgage insurance (PMI), further reducing the monthly payments.

While a 20% down payment is not mandatory, it is considered a substantial upfront payment that can lead to better interest rates and smaller monthly payments. For instance, a 20% down payment on a $400,000 home with a 30-year loan at a fixed 6% interest rate can result in monthly savings of around $400 compared to a 3% down payment. However, it is important to consider the potential drawbacks of a larger down payment, such as stretching savings too thin or missing out on opportunities to invest the money elsewhere.

To determine the ideal down payment amount, homebuyers can utilise online down payment calculators. These tools allow users to input various factors, such as the purchase price, interest rate, loan term, and property taxes, to estimate the impact of different down payment scenarios on their monthly payments. It is advisable to be conservative and cautious when deciding on a down payment amount to avoid financial strain. Additionally, exploring loan programs and down payment assistance options based on individual circumstances and requirements is essential.

Permanent Insurance: Is It a Worthwhile Investment?

You may want to see also

Frequently asked questions

A mortgage payment is comprised of the principal and interest. The principal is the loan amount borrowed, and the interest is the additional money that accrues over time, charged as a percentage of the initial loan.

There are other upfront and recurring costs to consider when getting a mortgage. Upfront costs include attorney fees, title service costs, recording fees, survey fees, property transfer tax, brokerage commission, and mortgage application fees. Recurring costs include property taxes, home insurance, and HOA (Homeowners Association) fees.

Your monthly mortgage payment will depend on several factors, including the purchase price, down payment, interest rate, loan term, property taxes, and insurance. You can use a mortgage calculator to estimate your monthly payments.

It is recommended that your mortgage payment should not exceed 28% of your monthly pre-tax income, and your total debt should not be more than 36% of your monthly income. This is known as the 28/36 rule or the DTI (Debt-to-Income) ratio.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)