When buying a home, you may be offered mortgage insurance, also known as mortgage default insurance or mortgage loan insurance. This type of insurance is mandatory if you want to buy a residential property with a down payment of less than 20% of the purchase price. It helps protect your lender in case you can't make your payments. The cost of mortgage insurance is typically calculated as a percentage of your total mortgage amount and is usually added to your regular mortgage payments. There are also optional types of mortgage insurance, such as mortgage life insurance, which can help your loved ones pay off the mortgage in the event of your death.

| Characteristics | Values |

|---|---|

| What is mortgage insurance? | Insurance that covers your lender in case you can't make your payments. |

| Who needs mortgage insurance? | Buyers who put a down payment of less than 20% of the purchase price. |

| How much does it cost? | Between 2.8% to 4.0% of the mortgage amount, depending on the financial situation and loan-to-value ratio. |

| Who pays for it? | The lender pays the insurance premium and usually passes this cost on to the borrower. |

| How is it paid? | The premium can be paid in a lump sum or added to the mortgage payments. |

| Is it mandatory? | Yes, if the down payment is less than 20%. Otherwise, it is optional. |

| What does it cover? | It covers the lender in case of borrower default and helps stabilize the housing market. |

| What are the benefits to the borrower? | It helps borrowers buy homes sooner, access better interest rates, and qualify for homes they otherwise wouldn't. |

| What are the drawbacks? | The cost of the premium is a significant con. |

| What are the alternatives? | Life insurance or personal life insurance can be used to cover mortgage payments in case of death. |

Explore related products

$15.95

What You'll Learn

![]()

Mortgage default insurance

In Canada, there are three mortgage default insurance providers: CMHC, Sagen (formerly Genworth Financial Canada), and Canada Guaranty. The most common provider is CMHC, a federal Crown Corporation, while Sagen and Canada Guaranty are private lenders. The lender arranges for mortgage default insurance on the borrower's behalf, and the borrower does not select their insurer. The insurance company evaluates the borrower's risk and the lender pays a premium on the loan, which covers the cost of legal proceedings and any shortfall if the property is sold due to borrower default.

Understanding House Mortgage Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Optional mortgage protection insurance

Mortgage protection insurance is an optional insurance product that can help you cover your mortgage payments during times of financial hardship due to unforeseen life events. It is different from mortgage loan insurance, which you are required to purchase if your down payment on your home is less than 20%.

Mortgage protection insurance acts as a safeguard if you can no longer afford your monthly mortgage repayments, helping you avoid defaulting on your mortgage and possibly losing your home. This type of insurance is particularly useful if you have dependents or a spouse who would like to stay in your home but may not be able to continue making the same mortgage payments.

There are several types of mortgage protection insurance:

- Mortgage life insurance: This insurance may pay off the remaining balance on your mortgage to the lender upon your death.

- Mortgage disability insurance: This insurance may make your mortgage payments to the lender if you become disabled and can't work due to a severe injury or illness.

- Critical illness insurance: This insurance may make your mortgage payments to the lender if you can't work due to a critical illness covered by the policy.

You can purchase mortgage protection insurance from your mortgage lender, a private insurance company, or a life insurance provider. It is important to note that your lender cannot insist that you buy mortgage insurance, and you must give express consent to obtain this product. Be sure to shop around and understand the terms and conditions of the insurance policy before purchasing it.

Mortgage Insurance: Death Benefit or Extra Cost?

You may want to see also

Explore related products

![]()

Mortgage life insurance

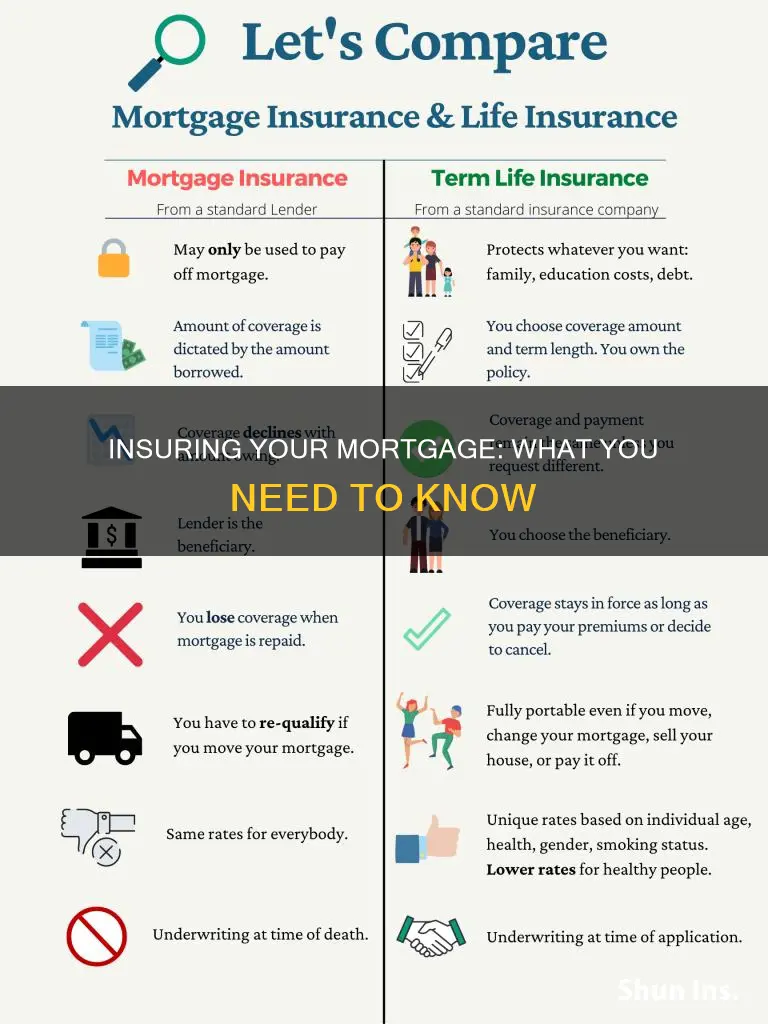

While mortgage life insurance provides peace of mind and helps your loved ones stay in their home, it has some limitations. The policy only covers the repayment of the mortgage, and the death benefit decreases as you pay down your mortgage while the premiums remain the same. This means that you will be paying the same premiums for a decreasing level of coverage. Furthermore, your beneficiaries do not receive the proceeds, so they cannot use the money to help with other expenses or debts. For these reasons, term life insurance may be a more flexible and cost-effective option for some individuals.

Strategies to Remove Private Mortgage Insurance

You may want to see also

Explore related products

$8

![]()

Mortgage disability insurance

When purchasing mortgage disability insurance, it is essential to understand the terms and conditions of the policy. Most insurance plans have specific inclusions and exclusions, such as a list of covered illnesses or injuries. Pre-existing medical conditions are usually not covered, and answering health-related questions is often a requirement during the application process. The cost of mortgage disability insurance is influenced by factors such as your age, health status, and the amount of your regular mortgage payment.

Before acquiring mortgage disability insurance, it is recommended to compare it with regular disability insurance. Regular disability insurance provides more comprehensive coverage, allowing you to use the benefits for various expenses, including your mortgage. Additionally, with regular disability insurance, you receive the payments directly, providing more flexibility in managing your finances. However, mortgage disability insurance may be suitable if you are in poor health or have a high-risk job and cannot qualify for regular disability insurance.

In summary, while mortgage disability insurance can provide financial protection for your mortgage payments in the event of disability, it is important to weigh the advantages against the limitations and explore alternative options to make an informed decision.

Home Insurance: Is Your Phone Covered?

You may want to see also

Explore related products

![]()

Critical illness insurance

When taking out critical illness insurance, it is important to consider whether you already have some form of illness insurance, such as through your employer or combined with another insurance policy. Income protection insurance, for example, may cover a broader range of illnesses and conditions and may be more suitable for your needs. It is also important to understand the terms and conditions of the insurance, including any exclusions and the specific illnesses or injuries that are covered. Pre-existing medical conditions are usually not covered by critical illness insurance.

The cost of critical illness insurance varies depending on your age and the amount of coverage you require. The older you are and the more coverage you need, the higher the premium you will pay. Critical illness insurance can be purchased through your mortgage lender, or from a bank, credit union, or another financial institution. In Canada, several banks and credit unions offer Mortgage Critical Illness Insurance, with employees trained to provide knowledge about the products.

Before purchasing critical illness insurance, it is advisable to seek independent financial advice to ensure you choose the policy that best suits your needs. An independent financial adviser can assess your situation and recommend the most suitable policy. While you may have to pay for this advice, it can help you make an informed decision about the right type and level of insurance coverage.

Overall, critical illness insurance can provide financial peace of mind and security in the event of a serious illness or injury. By understanding the different options available, seeking financial advice, and carefully considering your needs and budget, you can make an informed decision about whether to include critical illness insurance as part of your overall financial plan.

Understanding Insurance: Clove Report Basics

You may want to see also

Frequently asked questions

Mortgage insurance is a type of credit and loan insurance that you're usually offered when you take out or renew a mortgage. It helps protect the lender in case you can't make your payments.

If your down payment is less than 20% of a home’s purchase price, you need mortgage loan insurance, also known as mortgage default insurance. Mortgage insurance is optional if your down payment is more than 20% of the purchase price.

Mortgage insurance helps you buy a home sooner. It also adds stability to slow economic times and ensures mortgage funds are available to home buyers. It lowers the risk of lending and helps borrowers buy homes they wouldn’t otherwise qualify for.

There are two main types of mortgage insurance: mortgage default insurance and optional mortgage protection insurance. Mortgage default insurance is mandatory for down payments of less than 20%. Optional mortgage protection insurance can help protect the outstanding balance on your mortgage or cover your payments during financial hardship.