Permanent life insurance is a type of insurance policy that provides coverage for the entire lifespan of the policyholder. It is designed to offer long-term financial protection to the policyholder's loved ones. While permanent life insurance may be more expensive than term life insurance, it offers unique benefits such as lifelong coverage, guaranteed savings, and the opportunity to build cash value. This cash value component allows policyholders to withdraw or borrow funds during their lifetime, providing financial flexibility. However, the complexity of permanent life insurance and the potential for high premiums and limited returns raises the question of whether it is a worthwhile investment. This decision depends on individual circumstances, financial goals, and the need for long-term coverage.

| Characteristics | Values |

|---|---|

| Purpose | Financial protection of loved ones |

| Coverage | Permanent, lifelong |

| Premium | Remains level throughout the insured's lifetime |

| Cash value | Grows at a rate specified by the policy |

| Savings | Guaranteed |

| Complexity | More complex than term life insurance |

| Cost | More expensive than term life insurance |

| Renewal | Never needs to be renewed |

| Rate adjustment | Rates do not change with age |

| Death benefit | Tax-free |

| Investment | Not an investment vehicle |

| Dividends | Paid by some permanent life insurance options |

Explore related products

What You'll Learn

![]()

Permanent life insurance can be a good savings vehicle

The cash value component of permanent life insurance can be used to borrow money from the insurer, providing collateral for loans. Additionally, permanent life insurance policies may pay dividends, which can be taken as cash or used to purchase additional coverage. The premium amounts for permanent life insurance generally remain stable throughout the insured's lifetime, providing a sense of financial predictability.

Furthermore, permanent life insurance offers lifelong coverage, ensuring financial protection for loved ones regardless of when the policyholder passes away. This can be particularly important for individuals who want to provide long-term financial support for their dependents. The death benefit provided by permanent life insurance is typically tax-free, maximizing the benefit for beneficiaries.

While permanent life insurance may have higher premiums than term life insurance, it can be more efficient in the long run due to its permanent nature. Permanent life insurance never needs to be renewed, and rates do not increase with age. This stability can provide peace of mind and help individuals secure coverage early on, as premiums are usually lower when purchased at a younger age.

Overall, permanent life insurance can serve as a good savings vehicle, offering financial flexibility, lifelong coverage, and stable premiums. However, individuals should carefully consider their unique financial needs and circumstances before deciding on any insurance policy.

Police Reports: Redaction Rules for Insurance Claims

You may want to see also

Explore related products

![]()

Term life insurance is more affordable

Term life insurance is ideal for those who want substantial coverage at a low cost. It is a popular choice for individuals with specific financial obligations, such as raising children or paying off a mortgage. By contrast, permanent life insurance is a lifelong commitment with higher premiums. While permanent life insurance may be more efficient in the long run as it never needs to be renewed, term life insurance provides flexibility and affordability, especially during volatile economic times.

The affordability of term life insurance is particularly advantageous during periods of economic instability, such as a recession or pandemic. In such scenarios, individuals may face a higher risk of job loss and financial strain, making the lower premiums of term life insurance more manageable. Additionally, term life insurance can be tailored to meet specific needs, with options for level premium, yearly renewable term, and return of premium policies. Level premium policies maintain the same premium throughout the term, while yearly renewable term policies offer annual renewals at a higher cost. Return of premium policies refund a portion of the premiums if the policyholder survives the term.

Term life insurance also offers the advantage of simplicity. It is straightforward and easy to understand, without the complexity associated with permanent life insurance's cash value component. The absence of a cash value element in term life insurance contributes to its affordability. Permanent life insurance policies accumulate cash value over time, but this can be an expensive way to save for retirement due to the high premiums. On the other hand, term life insurance provides the option of ""living benefits," allowing policyholders to withdraw cash under certain circumstances.

While term life insurance is more affordable, it is important to consider individual circumstances when choosing between term and permanent life insurance. Permanent life insurance may be suitable for those seeking lifelong coverage, while term life insurance offers flexibility and cost-effectiveness for those with specific financial obligations or those who may outgrow their need for life insurance over time.

Insurance Loss: House Claims

You may want to see also

Explore related products

![]()

Permanent life insurance is complex

The cash value of permanent life insurance policies grows tax-deferred, meaning that no income taxes are paid on the growth, allowing it to accumulate faster. This cash value can be withdrawn or borrowed against during the lifetime of the policyholder, providing financial stability if needed. However, accessing the cash value will reduce the available cash surrender value and death benefit. Permanent life insurance policies may also pay dividends, which can be taken as cash, used to pay premiums, or reinvested to buy more insurance.

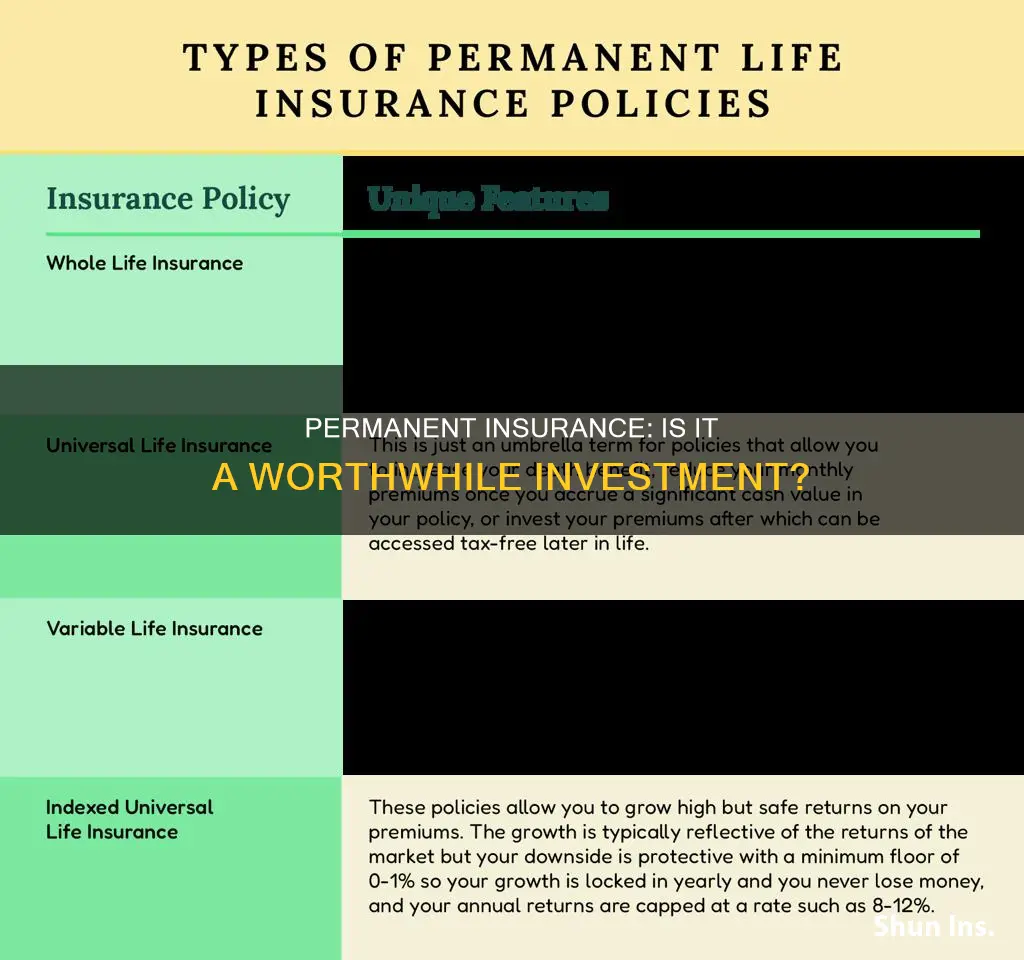

The complexity of permanent life insurance policies is further increased by the various types of policies available, such as whole life and universal life insurance. Whole life insurance policies are meant to last for the policyholder's entire life, building cash value in a secure account, and have regularly scheduled premiums. Universal life insurance, on the other hand, offers more flexibility as premium payments can be adjusted over time, but this can negatively impact the cash value and cause premiums to increase over time.

The decision to choose permanent life insurance should be made after careful consideration of one's unique needs and financial situation. While it offers lifelong coverage and a savings component, it is more complex and expensive than term life insurance. It may be more suitable for those who lack the discipline to save through other means, as it provides a forced savings mechanism through the premiums.

Farmers Insurance: Navigating the Claims Process and Settlement Offers

You may want to see also

Explore related products

![]()

Permanent life insurance provides lifelong coverage

Permanent life insurance policies often have a cash value component, which is similar to an investment account. This cash value grows tax-deferred, meaning you don't pay income taxes on it, allowing faster growth. The cash value can be withdrawn or borrowed against once it's large enough, and it can also be used to pay premiums. This feature can be especially helpful later in life, providing financial stability if your spouse or children depend on your income.

Another benefit of permanent life insurance is that it offers guaranteed-savings, which is useful for those who may not be disciplined about saving money on their own. Additionally, some permanent life insurance options pay the owner dividends, which can be taken as cash, applied to premiums, or used to buy more insurance.

However, permanent life insurance is often more complex than term life insurance due to its cash value component. The premiums for permanent life insurance can be expensive, and many people may outgrow the need for life insurance as they pay off debts and finish raising their kids. Therefore, it is essential to consider your unique financial needs and circumstances when deciding between term and permanent life insurance.

Insuring Your New Home: When to Start

You may want to see also

Explore related products

![]()

Permanent life insurance has a cash value component

Permanent life insurance is often more complex than term life insurance due to its cash value component. This feature can be especially helpful later in life since the cash value you accumulate can be accessed to help pay for unexpected emergencies or milestone events like college and retirement. The cash value component of a whole life policy grows tax-deferred, meaning that while the cash value grows, you do not pay income taxes on it, allowing it to grow even faster. On average, cash value will grow by around 4-5% IRR from most major mutually held insurance carriers.

The cash value of permanent life insurance does offer some financial protection. If you ever decide to give up your coverage, you would get the cash value back. However, during the first several years of coverage, there are surrender charges, so you wouldn't get the entire accumulated cash value. You'd still be able to recoup a portion of the money you will have paid. It's important to note that the cash value is separate from the death benefit of a permanent life insurance policy. When you pass away, your beneficiaries typically will not receive any of the cash value.

Some permanent life insurance options pay the owner dividends, which can be taken as cash, applied to your premium, saved to gather interest, or used to buy more insurance. Mutual life insurance companies are owned by their policyholders, so if the insurer brings in more money than is spent, the profits are distributed as dividends. These can be taken as cash, used to pay premiums, or used to pay for additional coverage. Each time you pay a premium, a portion of the money goes into a cash value account. This account grows at a rate specified by the policy. Once the cash value has reached a certain amount, you can borrow money from the insurer and use it as collateral.

While permanent life insurance may be more expensive than term life insurance, it may be more efficient in the long run. That's because permanent life insurance never needs to be renewed, and your rates will not be adjusted as you get older. Permanent life insurance is a way to build savings through premiums for those who aren't motivated to save through other means.

DirectPay Pet Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Permanent life insurance is a type of insurance that provides coverage for the entirety of the policyholder's life. It has a savings component that builds a cash value over time, which can be used as collateral to take out loans.

Term life insurance provides coverage for a specific period, typically 10-30 years. It is generally more affordable than permanent life insurance, with some policies priced at less than $20 per month for $500,000 of coverage for healthy people in their twenties.

Permanent life insurance offers lifelong coverage, guaranteed savings, and a cash value component that can be used to borrow money or pay premiums. It also provides financial stability for dependents if the policyholder passes away.

Permanent life insurance is often more complex and expensive than term life insurance. The cash value component may take a long time to grow, and the policy may need to be held for an extended period to be beneficial.

The worth of permanent life insurance depends on individual circumstances. It can be beneficial for those who want lifelong coverage, have a need for the savings component, and can afford the premiums. However, term life insurance may be a more affordable and flexible option for those who only require coverage for a specific period.