Life insurance is a financial safety net for loved ones in the event of the policyholder's death. However, life insurance policies, particularly whole life insurance, can also be used as collateral for loans or be a source of loans themselves. Globe Life Insurance offers whole life insurance policies with a cash value component, allowing policyholders to borrow against their policy's cash value. This article will explore how to get a loan from your Globe Life Insurance policy, the advantages and disadvantages, and important considerations to keep in mind.

| Characteristics | Values |

|---|---|

| Application process | Short |

| Credit check | Not required if cash value built up |

| Credit report | Does not appear on report |

| Interest rates | Lower than other loans |

| Repayment schedule | Set by the borrower and provider |

| Repayment | Not required |

| Cash value | Must be built up over time |

| Death benefit | Reduced if loan not repaid |

| Policy | Risk of losing policy if interest and unpaid loan amount total more than remaining cash value |

Explore related products

What You'll Learn

![]()

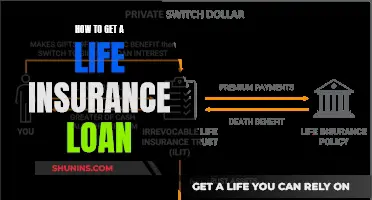

Using a life insurance policy as collateral

Advantages of Using a Life Insurance Policy as Collateral

There are several advantages to using a life insurance policy as collateral:

- No credit checks or qualification hoops: You can borrow money without having to prove your creditworthiness or jump through the usual qualification requirements.

- Competitive interest rates: Depending on the lender, you may be able to obtain a loan with a competitive interest rate, such as 4%.

- Potential for interest rate savings: If the interest rate on the loan is lower than the growth rate of your policy's cash value, the cost of borrowing can be offset by the gains on your policy.

- Access to funds: You can access the funds from the loan without having to wait until you reach a certain age or prove that the reason for borrowing is allowable.

- Flexibility in repayment: There is no set repayment schedule, and you can choose not to repay the loan, deducting the amount due from the beneficiary's benefit.

Disadvantages of Using a Life Insurance Policy as Collateral

There are also some disadvantages to consider:

- Risk to the policy: If you default on the loan, you may lose your life insurance policy, which could compromise the benefit for your beneficiaries.

- Interest charges: The insurance company will typically charge interest on the borrowed funds, which can reduce the overall value of your policy.

- Reduced death benefit: Borrowing against your life insurance policy will impact your coverage and may result in a reduced death benefit for your beneficiary if the loan is not repaid.

Requirements for Using a Life Insurance Policy as Collateral

To use your life insurance policy as collateral, several requirements must be met:

- The borrower must be the owner or an irrevocable beneficiary of the policy.

- The policy must remain in force for the life of the loan, with the policyholder making timely premium payments.

- The insurance company must allow collateral assignment.

- The lender becomes a beneficiary of the policy and must be notified of the collateral assignment.

- The policy must meet the lender's terms, including having sufficient death benefit coverage.

Alternatives to Using a Life Insurance Policy as Collateral

If you are considering using your life insurance policy as collateral, it is important to explore alternative options as well:

- Personal loans: You can apply for a personal loan from a bank, credit union, or private lender without putting your life insurance policy at risk.

- Surrendering your policy: If you no longer need the coverage, you can surrender your policy and use the cash value for your financial needs. However, your beneficiaries will no longer receive a death benefit.

- Other collateral options: You may have other assets that can be used as collateral for a loan, such as real estate, machinery, investments, or future payments from customers.

Who Qualifies as a Dependent for Life Insurance Coverage?

You may want to see also

Explore related products

![Loans on Life Insurance Policies, by John M. Taylor, President the Connecticut Mutual Life Insurance Company 1913 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Whole life policy loan

A whole life policy loan is when you borrow against the cash value of your permanent life insurance policy. This type of loan is available for whole life and universal life insurance policies, which accrue cash value over time. The cash value of a life insurance policy is funded by a portion of the premiums you pay.

To take out a whole life policy loan, you must have sufficient cash value built up in your policy. The minimum amount of cash value required varies by insurer. Once you have met this requirement, you can borrow up to the full amount of cash value you've accumulated. The insurance company will fund the loan, and your policy's cash value will be used as collateral.

There are several advantages to whole life policy loans. There is no approval process or credit check required, and the application process is short. Interest rates are typically lower than for personal loans and credit cards, and the money can be used for anything you want. Additionally, policy loans don't appear on your credit report, and you can choose your own repayment schedule or even choose not to repay the loan, instead deducting the amount due from the beneficiary's benefit.

However, there are also disadvantages and risks to consider. If the loan is not repaid, it will reduce the death benefit for your beneficiary. If the interest and unpaid loan amount total more than the remaining cash value, you could lose your policy. Additionally, you may owe taxes on the amount borrowed if the policy lapses.

Before taking out a whole life policy loan, it is important to consider the potential impact on your life insurance policy and beneficiaries, as well as any associated fees and costs. Consulting a financial advisor and a licensed insurance professional can help you make an informed decision.

Do You Have Whole Life Insurance? Here's How to Tell

You may want to see also

Explore related products

$16.53 $22.99

![]()

Borrowing from the cash value

Understanding Cash Value

The "cash value" of a life insurance policy refers to the ability to borrow from the policy if you have paid a certain amount in premiums. This is a feature of permanent life insurance policies, which include whole life and universal life insurance. On the other hand, term life insurance does not build cash value and only offers a death benefit.

The cash value of a life insurance policy is funded by a portion of the premiums you pay. When you pay your premium, a portion goes toward the cost of insuring you, another portion goes toward the cash value, and the remaining portion covers expense charges.

Borrowing from Cash Value

Once you have accrued enough cash value, you may be able to borrow from your life insurance policy. Most insurers have a minimum cash value requirement that must be met before you can take out a loan. After meeting this requirement, you can typically borrow up to the full amount you have accumulated.

There are several advantages to borrowing from the cash value of your life insurance policy:

- No lengthy application process: There is usually no credit check required, and policy loans do not appear on your credit report.

- Lower interest rates: Policy loans typically have lower interest rates compared to other types of loans.

- Flexible repayment terms: You can often set your own repayment schedule, and you may even choose to not repay the loan, with the amount due being deducted from the beneficiary's benefit.

However, there are also some drawbacks and risks to consider:

- Time to build cash value: It may take years from the policy start date to accumulate enough cash value to borrow against.

- Reduced death benefit: If the loan is not repaid, the death benefit for your beneficiary will be reduced.

- Risk of losing the policy: If the interest and unpaid loan amount total more than the remaining cash value, you could lose your policy.

- Over-loan risk: If the balance of the loan becomes larger than the cash value, you must repay enough to reduce the loan balance below the cash value to avoid the policy lapsing.

- Tax consequences: There may be potential tax implications if the policy lapses before the loan is repaid.

Considerations

Before deciding to borrow from the cash value of your life insurance policy, it is important to carefully consider the potential impact on your coverage, benefits, and premium schedule. It is recommended to treat this type of loan with the same level of diligence as any other loan. While it can provide a temporary financial solution, the primary purpose of a life insurance policy is to protect your beneficiaries in the event of your death. Therefore, it is crucial to ensure that borrowing from the cash value does not compromise this goal.

Life Insurance Rejection: What Are the Legal Risks?

You may want to see also

Explore related products

$8.34 $17.99

![]()

Cash value withdrawals

If you need quick access to cash but don't want to forfeit your coverage or ownership, you may want to consider withdrawing the cash value of your whole or universal life insurance policy. This option is typically best for those who need money fast but want to keep their policy. The amount you can withdraw depends on your specific policy and provider, but it's usually less than a policy loan.

Withdrawing the cash value of your life insurance policy is a big decision that can have a significant financial impact. It's important to understand the benefits and drawbacks before making any decisions.

One benefit of withdrawing the cash value is that you're essentially taking money that you've accumulated in your policy. This can be a quick way to access cash in an emergency without having to go through a lengthy loan application process. Additionally, since you're not borrowing money from a lender, there are no monthly payments or interest rates to worry about.

However, there are also several drawbacks to consider. Withdrawing the cash value of your policy will reduce or deplete the available cash value and will likely result in a reduced death benefit for your beneficiaries. There may also be potential tax implications, and you could find yourself in a situation where you've withdrawn all the cash value and still need to borrow money, which could put your policy at risk.

Before making any decisions, it's important to carefully consider your coverage, benefits, and premium schedule. It's also a good idea to consult a financial advisor or accountant to determine the best course of action for your specific situation.

Vaping and Life Insurance: Does It Show Up in Tests?

You may want to see also

Explore related products

![]()

Surrendering your policy

While this option can be beneficial, there are some things to watch out for. Firstly, you will be giving up your benefit, so your beneficiaries will no longer receive a payout upon your death. Additionally, there may be tax implications associated with surrendering your policy, so be sure to consult a financial advisor or accountant before making any decisions.

It's important to carefully consider your coverage, benefits, and premium schedule before making any changes to your life insurance policy. Borrowing from your life insurance policy will ultimately impact your coverage, so it's crucial to understand the financial implications and risks involved.

Before surrendering your policy, be sure to weigh the pros and cons and consider all your options. You may also want to speak with a financial advisor or a licensed insurance agent to fully understand the implications of surrendering your Globe Life Insurance policy.

When it comes to life insurance, it's always better to be informed and make decisions that align with your long-term financial goals and needs.

Whole Life Insurance: Does It Expire With Age?

You may want to see also

Frequently asked questions

The face value of life insurance is the amount paid to the beneficiaries when the insured person passes away. The cash value is the amount funded by a portion of the premiums paid by the insured person. When cashing out a policy, the insured person will receive the full cash value of the policy, not the full premium contributions.

Taking out a loan from your Globe Life Insurance policy can be done without a credit check and the interest rates are typically lower. Additionally, repayment terms are usually more flexible.

Yes, if you are unable to pay back the full amount, you may risk losing your policy if the interest and unpaid loan amount total more than the remaining cash value. Additionally, your beneficiary's benefit may be at risk.

You must first build up the cash value of your policy by paying your premium. Once you have accrued enough cash value, you may take out a loan, depending on eligibility requirements.