Whole life insurance is a financial tool that can provide added protection for your loved ones. If you pass away, your loved ones can help replace some of your income or save for the future using your policy’s death benefit payout. Whole life insurance also has a cash value growth component that can offer a wealth-building opportunity. However, if you no longer need or want whole life insurance, you can cancel your policy.

If you have recently purchased a policy, you are likely within the free look period, which typically lasts 10 to 30 days, depending on your state. This period allows you to cancel your policy without any financial penalty and receive a full refund of any premiums you’ve paid. After the free look period, if you have a term life insurance policy, you can simply stop paying premiums and walk away. If you have a permanent life insurance policy, you can surrender the policy for its cash value, or you may be able to exchange it for another policy or an annuity tax-free. You might also have the option to sell your policy in a life settlement, especially if you’re 75 or older.

| Characteristics | Values |

|---|---|

| Reasons for cancellation | Buyer's remorse, no longer wanting/needing the policy, switching policies, unaffordable premiums, etc. |

| Timing | During the "free look" period (typically 10-30 days), after the "free look" period, in the early years of the policy, after holding the policy for a long time, etc. |

| Policy type | Term life insurance, whole life insurance, universal life insurance, etc. |

| Cancellation process | Stop paying premiums, contact the insurance company, fill out forms, etc. |

| Money back | Depends on the type of policy, timing of cancellation, surrender charges, outstanding loans, withdrawals, etc. |

Explore related products

$15.95

What You'll Learn

![]()

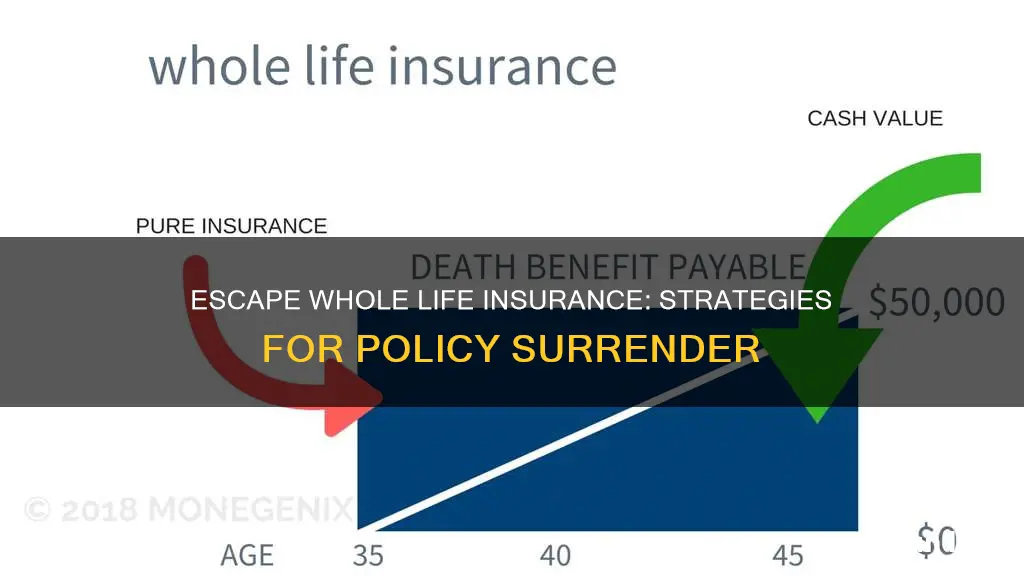

Surrender your policy

Surrendering your whole life insurance policy means cancelling your coverage in exchange for a lump sum value. The surrender value of a policy is based on the portion of premiums that went into the cash value account, plus the interest rate paid or investment gains. From that, outstanding loans are subtracted, along with any surrender fee.

If you surrender your whole life insurance policy, you will receive the cash value minus any surrender fees. If you go this route, the coverage ends, and your beneficiaries will not receive a death benefit when you die.

There are generally no restrictions on when you can surrender a life insurance policy, as long as you have made it through the surrender period. This period varies by policy and could be a couple of years to over 15 years. After the surrender period, the exact timing for surrendering your life insurance policy depends on your personal preference or financial situation. However, most policies require you to pay surrender fees when surrendering a policy. A surrender fee is a fee the life insurance company charges for you to cancel your insurance contract early. Surrender charges often decrease over the policy's life, with some disappearing entirely after a specific time. That means the longer you wait to surrender the policy, the less you'll likely pay in surrender fees.

Most life insurance companies make it reasonably straightforward to surrender your policy. While you'll want to check your policy for details, most policies require you to contact your insurance company or your insurance agent. You may have to sign paperwork confirming your surrender. Once the process is in motion, you likely won't have to do much but wait for the surrender value check. The insurance company handles the details of calculating your final payout. Generally, this amount is your cash value balance minus any surrender fees or outstanding loans on your policy.

In addition to surrender fees, you may have to pay taxes on your life insurance surrender value as taxable income. In general, you'll only pay income tax on interest or earnings over the amount you paid into the policy. The tax-free portion typically includes any money you paid in premiums over the life of the policy. For example, if you paid $50,000 into your policy's cash value via premiums and the surrender value is $60,000, you'll generally have to pay taxes on the $10,000 over what you paid into the policy.

Life Insurance Revolutionized: Algorithm-Led Innovations Save Lives

You may want to see also

Explore related products

![]()

Take out a policy loan

Taking out a policy loan is one way to get out of a whole life insurance policy. Whole life insurance lets you borrow at low rates with no credit check and no fixed repayment date. In some cases, you may not owe taxes on borrowed amounts, and your death benefit doesn't decrease. This offers a flexible way to access extra cash for various purposes.

However, interest accumulates on your outstanding balance. If the balance exceeds the cash value, your policy could lapse. This may result in a taxable event since you don't have to repay a loan on a canceled policy. Therefore, careful management of the loan is critical.

The process of taking out a life insurance loan is straightforward. You'll just need to fill out a form from the insurer, and the money will be deposited into your account, often within a few days. You may need to confirm your identity, sign a confirmation document, or provide a notarized confirmation before receiving your loan if:

- You provided new account information to the insurer in the past month

- The policy changed ownership recently

- The loan exceeds a specific size, such as $50,000

Unlike a bank loan or credit card, policy loans do not affect your credit, and there is no approval process or credit check since you are essentially borrowing from yourself. When borrowing on your policy, no explanation is required about how you plan to use the money, so it can be used for anything from bills to vacation expenses to a financial emergency.

The loan is also not recognized by the IRS as income, therefore it remains free from tax as long as the policy stays active (provided it's not a modified endowment contract). It's still expected that a policy loan will be paid back with interest (though the interest rates are typically much lower than on a bank loan or credit card) and there is no mandatory monthly payment.

A policy loan reduces your available cash value and death benefit. If you pass away while owing money on a life insurance loan, it will reduce the amount your beneficiaries receive.

Contacting American Amicable Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Consider a life settlement

A life settlement is a way to get cash for a life insurance policy you no longer need or can no longer afford. It is a sale of a life insurance policy by the policy owner to a third party. The seller typically gets more than the cash surrender value of the policy but less than the amount of the death benefit. The third party continues to pay the policy's premiums and then collects the death benefit when the insured dies.

A life settlement can make sense if your need for cash is greater than your need for providing a life insurance payout to your current beneficiaries. Your children might be grown and no longer count on your support. You might have high medical costs associated with a terminal illness or need long-term care but don't have another way to pay for it.

There are several steps to selling your life insurance policy:

- Fill out applications to one or more life settlement companies. Applications require the policyholder to submit life insurance information and medical records, or authorize the company to obtain that information on your behalf.

- Once the life settlement company has the necessary documentation, they will begin the underwriting process. During this stage, the company will check that all submitted information is accurate, and they will determine if you meet the requirements to qualify for a life settlement.

- After analyzing the value of your life insurance policy and determining it to be a good investment, a life settlement company will make an offer. You can choose to accept the offer and finalize the deal, or decline the offer and negotiate the sale value.

- If you decline the offer, you may be able to negotiate with the life settlement company to see if they will raise the amount they are willing to give you. These negotiations can go back and forth until you eventually agree on a value or decide to work with another life settlement company.

- When you accept an offer, the buyer will send you a closing package with documents to sign. Upon completion, the life insurance carrier receives written notice that the buyer is now the owner and beneficiary of the policy. At this point, you will also receive a one-time cash payment for the agreed-upon sale value.

There are several things to keep in mind when considering a life settlement:

- Age and health: Typically, you need to be old enough or sick enough for investors to be willing to take on the risk of buying your policy.

- Policy value: The face value of your life insurance policy must be at least $100,000 or more to qualify for a life settlement.

- Policy type: Not all types of life insurance policies are eligible for a life settlement. To qualify, you must hold a whole, universal, variable, or convertible term policy.

- Policy age: You must own a life insurance policy for anywhere from 2-5 years before selling it. The amount of time you need to wait depends on the state you live in, as each state has its own waiting period.

- Taxes: Proceeds from life settlements are taxed, meaning you will have to pay income tax on any value you get that exceeds the money you have paid toward premiums.

- Alternatives: A life settlement may not be the ideal option for everyone. There might be better alternatives, such as letting your policy lapse by no longer paying premiums, surrendering your policy for its cash value, or borrowing from the cash value of the policy.

Diabetes and Life Insurance: Impact and Implications

You may want to see also

Explore related products

![]()

Exchange your policy

If you have a permanent life insurance policy, you can exchange it for another insurance product, such as an annuity, long-term care insurance, or another life insurance policy, without paying taxes. This is called a 1035 exchange.

A 1035 exchange can be a good option if you no longer need the coverage provided by your current policy but want to continue investing in a similar product. It's important to work with a qualified life insurance advisor to ensure the exchange is done correctly and explore other options before making a final decision.

You can also exchange your policy for a very low-cost variable annuity (VA). This will allow you to grow your cash value tax-free until it equals the basis, and then surrender the VA with no tax cost. However, finding a low-cost VA can be difficult.

Another option is to exchange your whole life policy into a modified endowment contract. This will eliminate the need to make additional payments into the policy, but you won't be able to use the cash value for other purposes or borrow against the policy later in life.

U.S.A.A. Life Insurance: Physical Exam Requirements Explained

You may want to see also

![]()

Get term life insurance in place first

Before you cancel your whole life insurance policy, it is important to get term life insurance in place. This process usually takes a couple of weeks, but it is vital to ensure that you are not left exposed, even for a short period of time. Additionally, you may be surprised by something that is found during underwriting, so it is better to be safe than sorry.

Life Insurance: Cremation Coverage and Your Options

You may want to see also

Frequently asked questions

The best way to cancel your life insurance policy depends on the type of policy you have and how long you've had it. Term life insurance policies are generally easier to cancel than permanent life insurance policies. If you've had your policy for less than a month, you can cancel during the "free look" period and get a full refund. Otherwise, you can simply stop paying premiums and walk away. For permanent life insurance policies, you can surrender the policy for its cash value, but you may be subject to surrender fees. You may also be able to exchange your policy for another policy or an annuity tax-free.

Whether you can get money back when cancelling a life insurance policy depends on the type of policy and when you cancel it. Term life insurance policies do not accumulate cash value, so you will not receive a payout if you cancel. Permanent life insurance policies, on the other hand, do accumulate cash value, and you may receive a payout if you cancel, but this will likely be reduced by surrender fees, especially if you cancel in the early years of the policy.

If you're thinking of cancelling your life insurance policy because you can no longer afford the premiums, there are a few alternatives you can consider. You may be able to use the cash value of your policy to pay the premiums, although this will reduce the death benefit. You could also explore options like converting your term policy to a permanent policy, or reducing your death benefit to lower your premium payments.

There are several situations in which it may make sense to cancel your life insurance policy. If you no longer need coverage, for example, if your family is grown and financially independent, you may want to cancel. You may also want to cancel if you are changing your investment strategy or if you are switching policies or insurance companies.

Yes, your insurance company can cancel your life insurance policy, but only under specific circumstances, such as non-payment of premiums, policy misrepresentation, cash value depletion, or the policy reaching maturity.