Short-term health insurance is a type of health coverage that provides temporary protection for individuals who are in transition between jobs, waiting for employer-sponsored insurance to begin, or who need coverage for a brief period. To keep short-term health insurance, it's essential to understand the eligibility criteria, application process, and potential limitations of these plans. Typically, short-term health insurance can be purchased directly from an insurance company or through a broker, and the duration of coverage can vary from a few weeks to several months. It's important to note that short-term plans may not cover pre-existing conditions and often have limited benefits compared to long-term health insurance. To maintain short-term health insurance, policyholders must pay their premiums on time and adhere to the terms and conditions of their plan. Additionally, individuals should be aware of their rights and responsibilities under the Affordable Care Act (ACA) and how short-term health insurance may impact their eligibility for other health coverage options.

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements to qualify for short-term health insurance plans

- Coverage Duration: Learn about the typical length of coverage for short-term health insurance

- Policy Limitations: Be aware of any restrictions or exclusions in short-term health insurance policies

- Cost Factors: Discover the elements that influence the cost of short-term health insurance premiums

- Application Process: Get familiar with the steps to apply for and enroll in a short-term health insurance plan

![]()

Eligibility Criteria: Understand the requirements to qualify for short-term health insurance plans

To qualify for short-term health insurance plans, individuals must meet specific eligibility criteria set by insurance providers and regulatory bodies. These criteria typically include age, health status, and residency requirements. For instance, many short-term plans are available to individuals between the ages of 18 and 64 who are in good health and do not have pre-existing conditions. Some plans may also require applicants to undergo a medical exam or provide proof of income to ensure they can afford the premiums.

One unique aspect of short-term health insurance eligibility is the lack of a requirement for a qualifying life event, which is often necessary for enrolling in major medical plans outside of open enrollment periods. This makes short-term plans more accessible for individuals who experience a gap in coverage due to job loss, divorce, or other life changes. However, it's important to note that these plans are designed to provide temporary coverage and may not be suitable for everyone.

When applying for short-term health insurance, it's crucial to carefully review the eligibility criteria and application process to ensure you meet all the necessary requirements. This may involve gathering documentation, such as proof of identity, residency, and income, as well as completing a health questionnaire or undergoing a medical exam. By understanding the eligibility criteria and following the application process closely, you can increase your chances of qualifying for a short-term health insurance plan that meets your needs.

In conclusion, eligibility criteria for short-term health insurance plans are designed to ensure that applicants are in good health and can afford the coverage they are seeking. By meeting these criteria and following the application process carefully, individuals can secure temporary health insurance coverage to protect themselves during periods of transition or uncertainty.

Medigap and Medicaid: Understanding Their Complex Relationship

You may want to see also

Explore related products

![]()

Coverage Duration: Learn about the typical length of coverage for short-term health insurance

Short-term health insurance plans typically offer coverage for a limited duration, ranging from a few days to several months. These plans are designed to provide temporary protection for individuals who are between jobs, waiting for employer-sponsored coverage to begin, or who need immediate insurance while they apply for a longer-term policy. The exact length of coverage can vary significantly depending on the insurance provider and the specific plan chosen. Some short-term plans may offer renewable options, allowing policyholders to extend their coverage period, while others may have strict limits on the maximum duration of insurance.

When considering short-term health insurance, it's essential to carefully review the terms and conditions of the policy to understand the coverage duration and any limitations or exclusions that may apply. Policyholders should also be aware of the potential consequences of allowing their short-term coverage to lapse, as this could result in a gap in insurance protection and potentially higher premiums when applying for a new policy.

One unique aspect of short-term health insurance is that it often provides an opportunity for individuals to secure coverage quickly, sometimes within 24 hours of applying. This can be particularly beneficial for those who have experienced a sudden loss of employment or who need immediate insurance due to unforeseen circumstances. However, it's important to note that short-term plans may not offer the same level of comprehensive coverage as longer-term policies, and policyholders may need to carefully manage their healthcare needs during the coverage period.

In conclusion, understanding the coverage duration of short-term health insurance is crucial for individuals who are considering this type of policy. By carefully reviewing the terms and conditions and being aware of the potential limitations and consequences, policyholders can make informed decisions about their healthcare coverage and ensure that they have the protection they need during a transitional period.

Enrolling in Starbucks Medical Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Policy Limitations: Be aware of any restrictions or exclusions in short-term health insurance policies

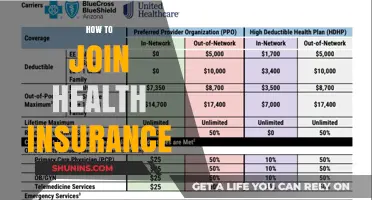

Short-term health insurance policies often come with limitations that can significantly impact their usefulness. One major restriction is the pre-existing conditions clause, which may exclude coverage for any health issues you had before purchasing the policy. This means that if you have a chronic condition like diabetes or asthma, your short-term insurance might not cover related medical expenses. It's crucial to carefully review the policy's terms and conditions to understand what is and isn't covered.

Another limitation to consider is the duration of coverage. Short-term health insurance policies typically last between 30 days and 3 months, which may not be sufficient if you're dealing with a prolonged health issue or waiting for a new job with employer-sponsored insurance to start. Additionally, these policies often have a maximum payout limit, which can be as low as $5,000 or $10,000. This cap can quickly be reached with a single hospital visit or surgery, leaving you responsible for any additional costs.

Short-term health insurance policies also tend to have higher out-of-pocket costs, including deductibles and copays, compared to long-term plans. This can make them less affordable in the long run, especially if you require frequent medical care. Furthermore, these policies may not cover preventive care, such as routine check-ups or vaccinations, which can lead to unexpected expenses if you need these services.

To navigate these limitations, it's essential to have a clear understanding of your healthcare needs and budget. If you're considering a short-term health insurance policy, make sure to read the fine print and ask questions about any unclear terms. It may also be beneficial to consult with a healthcare professional or insurance advisor to determine if a short-term policy is the right choice for your situation. Remember, while short-term health insurance can provide temporary coverage, it's not a substitute for comprehensive, long-term health insurance.

Electronic Health Records: Do They Include Insurance Data?

You may want to see also

Explore related products

![]()

Cost Factors: Discover the elements that influence the cost of short-term health insurance premiums

Several factors can influence the cost of short-term health insurance premiums. Understanding these factors can help you make informed decisions when selecting a policy. Here are some key elements that can impact the cost of your short-term health insurance:

- Age: Younger individuals typically pay lower premiums compared to older adults. This is because younger people are generally considered to be at lower risk for health issues that require extensive medical care.

- Health Status: Your overall health condition plays a significant role in determining your premium cost. Individuals with pre-existing conditions or a history of serious health issues may face higher premiums due to the increased risk they pose to insurers.

- Coverage Duration: The length of time you need coverage can also affect the cost. Short-term health insurance is designed to provide temporary coverage, usually up to 12 months. The longer you need coverage, the more you may pay in premiums.

- Deductible and Coinsurance: Policies with higher deductibles and coinsurance rates typically have lower premiums. This is because you are agreeing to pay more out-of-pocket for your healthcare expenses, which reduces the financial risk for the insurer.

- Location: Where you live can also impact the cost of your premiums. Healthcare costs vary by region, and insurers may adjust their rates accordingly. Urban areas may have higher premiums due to the higher cost of living and healthcare services.

- Provider Network: Some short-term health insurance plans may have a limited network of healthcare providers. Plans with a more extensive network may have higher premiums due to the increased access to healthcare services.

By considering these factors, you can better understand why your short-term health insurance premiums may vary and make more informed decisions when choosing a plan that fits your needs and budget.

Top Health Insurance Providers Serving Texas Residents: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Application Process: Get familiar with the steps to apply for and enroll in a short-term health insurance plan

Navigating the application process for short-term health insurance requires a clear understanding of the steps involved. Begin by researching and selecting a reputable insurance provider that offers short-term plans. Once you've identified a suitable provider, visit their website or contact their customer service to initiate the application process. Be prepared to provide personal information such as your name, address, date of birth, and social security number.

During the application process, you may be asked to answer health-related questions to determine your eligibility and premium rates. It's essential to answer these questions accurately to avoid any issues with your coverage later on. If you have any pre-existing conditions, be sure to disclose them as they may impact your ability to obtain coverage or affect your premium costs.

After submitting your application, you may need to undergo a medical exam or provide additional documentation to support your health status. This step is crucial for the insurance provider to assess your risk level and determine the appropriate coverage options for you. Be proactive in gathering any necessary documents and scheduling any required exams to expedite the process.

Once your application is approved, carefully review the terms and conditions of your short-term health insurance plan. Pay close attention to the coverage limits, deductibles, and any exclusions or restrictions that may apply. It's also important to understand your premium payment schedule and any grace periods for making payments to avoid lapses in coverage.

Finally, keep track of your enrollment dates and any renewal options available to you. Short-term health insurance plans typically have a limited duration, so it's essential to monitor your coverage period and plan accordingly. If you anticipate needing continued coverage beyond the initial term, explore your options for renewing or transitioning to a longer-term plan.

Understanding Coinsurance Fees in Health Insurance: A Comprehensive Guide

You may want to see also

Frequently asked questions

Short-term health insurance is a temporary health plan that provides coverage for a limited period, typically ranging from a few days to several months. It is suitable for individuals who need immediate coverage and are in between jobs, waiting for employer-sponsored insurance to begin, or have recently graduated from college.

Qualification for short-term health insurance usually involves meeting certain eligibility criteria, such as being under a certain age, not having pre-existing conditions, and not being eligible for Medicaid or Medicare. The specific requirements may vary depending on the insurance provider and the state you reside in.

Short-term health insurance plans generally cover unexpected medical expenses, such as doctor visits, hospital stays, and emergency room visits. However, they may not cover preventive care, prescription drugs, or pre-existing conditions. It's important to review the plan details carefully to understand what is and isn't covered.

You can find short-term health insurance plans through various sources, including insurance companies, online marketplaces, and insurance brokers. To apply, you will typically need to provide personal information, such as your name, address, and date of birth, as well as answer questions about your health history. Once approved, you can enroll in the plan and make the required premium payments to activate your coverage.