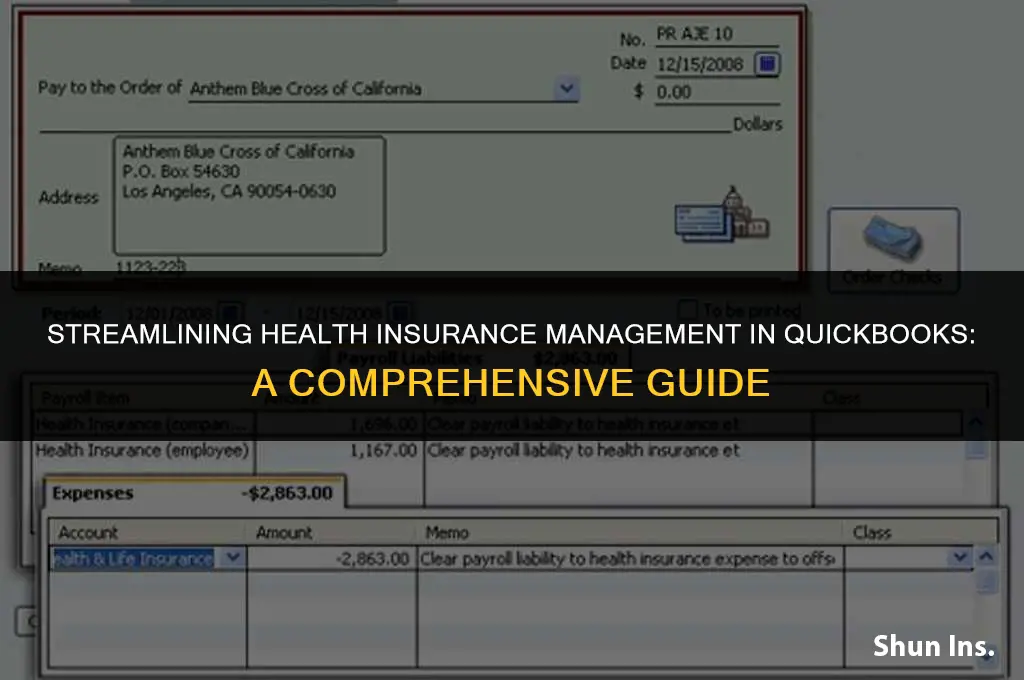

Listing health insurance in QuickBooks is an essential task for businesses that offer this benefit to their employees. To do this accurately, you'll need to set up a new payroll item specifically for health insurance. Begin by navigating to the 'Payroll' menu and selecting 'Payroll Items.' From there, choose 'New' to create a custom payroll item. Name the item 'Health Insurance' and ensure it's marked as a 'Deduction.' You'll then need to define the deduction amount, which can be a fixed dollar amount or a percentage of the employee's gross pay. Once the item is set up, you can assign it to the appropriate employees and track the deductions in their paychecks. This process helps streamline payroll management and ensures accurate record-keeping for both the employer and employees.

Explore related products

What You'll Learn

- Setting Up Health Insurance Accounts: Create separate accounts for premiums, claims, and payments to ensure accurate tracking

- Entering Health Insurance Premiums: Record monthly premiums as expenses to reflect ongoing costs and maintain financial accuracy

- Tracking Health Insurance Claims: Monitor claims submitted and received payments to manage cash flow and reconcile accounts

- Managing Health Insurance Payments: Ensure timely payment of premiums and claims to avoid penalties and maintain good standing

- Reporting Health Insurance Costs: Generate reports to analyze health insurance expenses and identify areas for cost savings

![]()

Setting Up Health Insurance Accounts: Create separate accounts for premiums, claims, and payments to ensure accurate tracking

To effectively manage health insurance in QuickBooks, it's crucial to set up separate accounts for premiums, claims, and payments. This ensures accurate tracking and simplifies the reconciliation process. Begin by creating a new account for health insurance premiums. This account should be categorized under 'Expenses' and will be used to record the monthly or annual premiums paid to the insurance provider.

Next, create an account for health insurance claims. This account should be categorized under 'Assets' as it represents money owed to you by the insurance company for covered medical expenses. When you submit a claim, you'll record the amount in this account. Once the claim is approved and the insurance company pays you, you'll transfer the funds from the claims account to your checking account.

In addition to these two accounts, you should also set up an account for health insurance payments. This account should be categorized under 'Liabilities' and will be used to track payments made to healthcare providers for out-of-pocket expenses or co-pays. When you make a payment, you'll record the amount in this account. At the end of each month, you can reconcile this account with your checking account to ensure all payments have been accounted for.

By setting up these separate accounts, you'll be able to easily track your health insurance expenses and ensure that you're accurately recording and reconciling all transactions related to your health insurance. This will not only save you time and effort but also provide you with a clear picture of your health insurance costs and benefits.

Understanding the Medical Insurance Claim Process

You may want to see also

Explore related products

![]()

Entering Health Insurance Premiums: Record monthly premiums as expenses to reflect ongoing costs and maintain financial accuracy

To accurately reflect ongoing costs and maintain financial accuracy in QuickBooks, it's essential to record monthly health insurance premiums as expenses. This practice ensures that your financial statements provide a true picture of your business's financial health. Here's a step-by-step guide on how to enter health insurance premiums in QuickBooks:

- Open QuickBooks and Navigate to the Expenses Section: Log in to your QuickBooks account and click on the "Expenses" tab located on the left-hand side of the screen. This will take you to the expenses recording section.

- Create a New Expense: Click on the "New Expense" button to start recording a new expense. In the expense form, select the appropriate account for your health insurance premiums, such as "Health Insurance" or "Employee Benefits."

- Enter the Premium Amount: In the "Amount" field, enter the monthly premium amount. Ensure that you enter the correct amount to avoid any discrepancies in your financial records.

- Specify the Payment Method: Choose the payment method used for paying the health insurance premium. This could be a check, credit card, or bank transfer. QuickBooks allows you to track different payment methods, which helps in reconciling your accounts later.

- Set the Expense Date: Enter the date on which the premium was paid or is due. This date will determine in which accounting period the expense is recorded, affecting your financial statements accordingly.

- Save the Expense: Once you have filled in all the necessary details, click on the "Save" button to record the expense. QuickBooks will automatically update your financial records to reflect the new expense.

By following these steps, you can ensure that your health insurance premiums are accurately recorded as expenses in QuickBooks. This not only helps in maintaining financial accuracy but also aids in budgeting and forecasting future expenses. Regularly recording these premiums can provide valuable insights into your business's financial commitments and help you make informed decisions regarding employee benefits and cost management.

Health Insurance Coverage for Road Trips: Alaska Edition

You may want to see also

Explore related products

![]()

Tracking Health Insurance Claims: Monitor claims submitted and received payments to manage cash flow and reconcile accounts

To effectively track health insurance claims in QuickBooks, it's essential to monitor both the claims submitted and the payments received. This dual approach ensures that you can manage your cash flow efficiently and reconcile your accounts accurately. Start by setting up a system to record each claim as it's submitted, including the date, claim number, patient information, and the amount billed. You can use QuickBooks' invoicing feature to create and track these claims.

Once a claim is submitted, it's crucial to follow up with the insurance provider to confirm receipt and processing. QuickBooks allows you to set reminders and track the status of each claim, helping you stay on top of pending payments. When a payment is received, record it in QuickBooks by matching it to the corresponding claim. This will help you maintain an accurate record of your accounts receivable and ensure that your financial statements reflect the correct amounts.

In addition to tracking individual claims, it's important to analyze your claims data as a whole. QuickBooks provides reporting tools that can help you identify trends, such as which insurance providers are paying claims more quickly or which types of claims are being denied more frequently. This information can be invaluable in making decisions about your practice's financial management and in negotiating with insurance providers.

To streamline the claims tracking process, consider using QuickBooks' automation features. You can set up automatic reminders for follow-ups, create custom workflows for claim processing, and even use QuickBooks' mobile app to stay updated on the go. By leveraging these tools, you can reduce the administrative burden of claims tracking and focus more on providing quality care to your patients.

Finally, it's important to regularly review and reconcile your accounts to ensure that all claims have been processed and payments have been received. QuickBooks makes this process straightforward with its reconciliation tools, which allow you to match transactions and identify any discrepancies. By maintaining accurate and up-to-date financial records, you can ensure the financial health of your practice and make informed decisions about your business.

Injury Insurance vs. Health Insurance: Understanding Coverage Differences

You may want to see also

Explore related products

![]()

Managing Health Insurance Payments: Ensure timely payment of premiums and claims to avoid penalties and maintain good standing

To manage health insurance payments effectively, it's crucial to set up a system that ensures timely payment of premiums and claims. This can be achieved by leveraging QuickBooks' automated features. Begin by creating a separate account for health insurance premiums and another for claims. This will help you track payments and receipts more efficiently. Next, set up recurring payments for premiums to avoid missing deadlines. QuickBooks allows you to schedule these payments in advance, ensuring that funds are deducted automatically on the due date.

For claims, establish a routine to submit them as soon as possible after receiving the necessary documentation. QuickBooks can streamline this process by allowing you to attach supporting documents directly to the claim. This reduces the risk of delays due to misplaced paperwork. Additionally, regularly review your health insurance statements to verify that all payments have been processed correctly. QuickBooks' reporting features can generate detailed statements that make it easy to identify any discrepancies or errors.

It's also important to stay informed about any changes in your health insurance policy that could affect your payments. This includes updates to premium rates, changes in coverage, or new requirements for claims submission. QuickBooks can help you manage these changes by allowing you to update your accounts and payment schedules as needed. By staying proactive and organized, you can avoid penalties and maintain good standing with your health insurance provider.

Do Social Workers Explain Health Insurance? Understanding Their Role in Healthcare

You may want to see also

Explore related products

![]()

Reporting Health Insurance Costs: Generate reports to analyze health insurance expenses and identify areas for cost savings

To effectively manage health insurance costs, it's crucial to have a clear understanding of where your expenses are going. QuickBooks provides a robust reporting feature that allows you to generate detailed reports on your health insurance expenses. These reports can help you identify areas where you can cut costs and make more informed decisions about your health insurance coverage.

The first step in generating these reports is to ensure that your health insurance expenses are properly categorized in QuickBooks. This means setting up specific accounts for health insurance premiums, copays, deductibles, and any other related expenses. Once your expenses are categorized correctly, you can use QuickBooks' reporting tools to create custom reports that focus on your health insurance costs.

One of the most useful reports for analyzing health insurance expenses is the 'Health Insurance Expense Report'. This report provides a breakdown of your total health insurance costs by category, allowing you to see exactly where your money is going. You can also use this report to compare your current health insurance costs to previous periods, helping you to identify trends and potential areas for cost savings.

Another valuable report is the 'Health Insurance Cost per Employee Report'. This report calculates the average health insurance cost per employee, which can be helpful in identifying employees who may be incurring higher than average costs. This information can then be used to target cost-saving measures, such as negotiating better rates with providers or implementing wellness programs to reduce health insurance claims.

In addition to these standard reports, QuickBooks also allows you to create custom reports that can be tailored to your specific needs. For example, you could create a report that tracks the percentage of health insurance costs that are covered by your company versus the percentage that is paid by employees. This type of report can be useful in evaluating the effectiveness of your health insurance plan and in making decisions about future coverage options.

By regularly generating and analyzing these reports, you can gain a deeper understanding of your health insurance costs and identify opportunities to reduce expenses without compromising on coverage. This not only helps to improve your company's bottom line but also ensures that you are providing the best possible health insurance options for your employees.

Strategies for Selling Medical Insurance: Tips and Tricks

You may want to see also

Frequently asked questions

To set up health insurance tracking in QuickBooks, navigate to the "Lists" menu and select "Charts of Accounts." Create a new account under "Expenses" for health insurance premiums. Additionally, set up a separate account for health insurance reimbursements under "Other Income." This will allow you to accurately track and report health insurance-related transactions.

Yes, you can automate health insurance premium payments in QuickBooks by setting up a recurring payment. Go to the "Pay Bills" section, select the health insurance premium bill, and choose the "Recurring" option. Enter the payment frequency, start date, and end date to automate the process.

To report health insurance expenses on your tax return using QuickBooks, generate a Profit and Loss report. Ensure that the health insurance premium expenses are categorized correctly under the appropriate expense account. The report will provide a summary of your business's income and expenses, including health insurance costs, which can be used for tax reporting purposes.