Lowering health insurance costs can be achieved through various strategies. One approach is to shop around and compare policies from different providers to find the most affordable option. Additionally, increasing your deductible or opting for a high-deductible health plan can lead to lower monthly premiums. Another cost-saving measure is to take advantage of preventive care services, which are often covered at no cost to you. Furthermore, maintaining a healthy lifestyle by exercising regularly, eating a balanced diet, and avoiding tobacco can also contribute to lower health insurance costs in the long run.

Explore related products

What You'll Learn

- Shop Around for Plans: Compare different health insurance providers and plans to find the most affordable option

- Increase Your Deductible: Opt for a higher deductible to reduce your monthly premium payments

- Take Advantage of Discounts: Look for discounts based on factors like age, occupation, or membership in certain organizations

- Maintain a Healthy Lifestyle: Engage in regular exercise and maintain a balanced diet to potentially qualify for lower premiums

- Consider a Health Savings Account (HSA): Utilize an HSA to save money on taxes and pay for qualified medical expenses

![]()

Shop Around for Plans: Compare different health insurance providers and plans to find the most affordable option

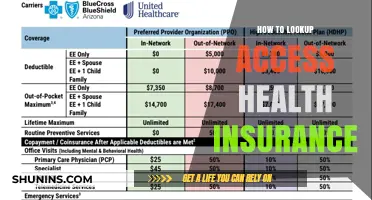

To effectively shop around for health insurance plans, it's crucial to understand your unique needs and preferences. Start by assessing your current health status, anticipated medical expenses, and any specific requirements you may have, such as prescription drug coverage or mental health services. Once you have a clear picture of your needs, you can begin comparing different providers and plans. Utilize online comparison tools or consult with a licensed insurance agent to explore a variety of options. Pay close attention to factors like premiums, deductibles, copays, and out-of-pocket maximums to determine the overall affordability of each plan.

When comparing health insurance plans, consider the network of healthcare providers associated with each option. Some plans may offer more comprehensive coverage within a specific network, while others may provide more flexibility to visit out-of-network providers. Evaluate the quality of care and customer satisfaction associated with each provider by researching reviews and ratings. Additionally, take note of any additional benefits or perks offered by certain plans, such as wellness programs, telemedicine services, or discounts on gym memberships.

It's essential to carefully review the terms and conditions of each plan, as well as the exclusions and limitations. Some plans may have hidden costs or restrictions that could impact your overall healthcare experience. Reach out to the insurance provider directly if you have any questions or concerns about the plan details. By thoroughly comparing different health insurance providers and plans, you can make an informed decision that aligns with your budget and healthcare needs.

Remember that the most affordable option may not always be the best choice for your specific situation. Consider the long-term implications of each plan, including the potential for rate increases or changes in coverage. It may be beneficial to consult with a financial advisor or healthcare professional to discuss the pros and cons of each option. Ultimately, the goal is to find a health insurance plan that provides adequate coverage at a reasonable cost, while also meeting your individual preferences and requirements.

Mastering Health Insurance Allocation in Mutual Fund Schemes: A Guide

You may want to see also

Explore related products

![]()

Increase Your Deductible: Opt for a higher deductible to reduce your monthly premium payments

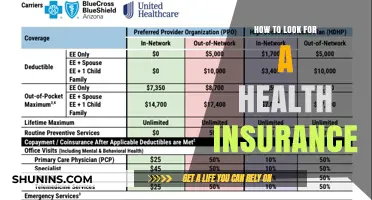

Choosing a higher deductible is a strategic way to lower your monthly health insurance premiums. This approach is particularly beneficial for individuals who are generally healthy and do not anticipate frequent medical expenses. By opting for a higher deductible, you are essentially agreeing to pay more out-of-pocket for healthcare costs before your insurance coverage kicks in. This increased financial responsibility typically results in lower monthly premiums, as the insurance company is taking on less risk.

For example, if you currently have a deductible of $500 and you increase it to $1,000, you could potentially save anywhere from 10% to 30% on your monthly premiums, depending on your insurance provider and policy details. This savings can add up significantly over the course of a year, making it a viable option for those looking to reduce their healthcare costs.

However, it's important to consider the potential downsides of increasing your deductible. If you do end up needing medical care, you will be responsible for covering a larger portion of the costs upfront. This could lead to financial strain if you are not prepared. Additionally, increasing your deductible may not be the best option if you have chronic health conditions or require frequent medical attention, as the increased out-of-pocket costs could outweigh the savings on premiums.

To determine if increasing your deductible is the right choice for you, it's essential to evaluate your current health status, anticipated medical needs, and financial situation. If you are generally healthy and have the financial means to cover a higher deductible, this option could be a practical way to lower your health insurance costs. However, if you have significant health concerns or limited financial resources, it may be more beneficial to maintain a lower deductible and higher premiums to ensure you have adequate coverage when you need it.

In conclusion, increasing your deductible can be an effective strategy for reducing your monthly health insurance premiums, but it's crucial to weigh the potential benefits against the risks and consider your individual circumstances before making a decision.

President's Budget Cuts: Impact on Children's Health Insurance Program

You may want to see also

Explore related products

$9.95 $9.95

![]()

Take Advantage of Discounts: Look for discounts based on factors like age, occupation, or membership in certain organizations

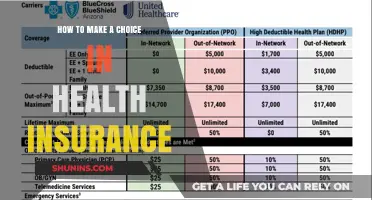

Did you know that your age, occupation, or membership in certain organizations could qualify you for discounts on your health insurance premiums? Many insurers offer special rates to individuals who fall into specific categories, so it's worth exploring these options to see if you can save money on your coverage.

For example, if you're a senior citizen, you may be eligible for discounts through organizations like AARP or the National Association of Retired Persons (NAR). These groups often partner with insurance companies to offer exclusive rates to their members. Similarly, if you're a member of a professional organization, such as a medical association or a teachers' union, you may be able to access discounted health insurance through your membership.

To take advantage of these discounts, you'll need to do some research and legwork. Start by contacting your current insurer to see if they offer any discounts based on your age, occupation, or memberships. If they don't, shop around for other insurers that do. You can also reach out to organizations you're a part of to see if they have any partnerships with health insurance providers.

Keep in mind that the availability and amount of discounts can vary widely depending on the insurer and the specific criteria they use. Some discounts may be small, while others can be significant, so it's important to compare rates and options carefully. Additionally, be aware that you may need to provide proof of your age, occupation, or membership to qualify for these discounts, so have that documentation ready when you're applying for coverage.

By taking the time to explore these discount options, you could potentially save hundreds of dollars a year on your health insurance premiums. And who wouldn't want to take advantage of that?

Medical Malpractice: Insurance Limits and You

You may want to see also

Explore related products

![]()

Maintain a Healthy Lifestyle: Engage in regular exercise and maintain a balanced diet to potentially qualify for lower premiums

Regular exercise and a balanced diet are not only crucial for overall health but can also play a significant role in reducing health insurance premiums. Many insurance providers offer discounts to policyholders who demonstrate a commitment to maintaining a healthy lifestyle. This can include participating in wellness programs, achieving certain fitness milestones, or even using wearable devices to track physical activity.

To potentially qualify for lower premiums, individuals should aim to engage in moderate-intensity aerobic exercise for at least 150 minutes per week, as recommended by the World Health Organization. This can include activities such as brisk walking, cycling, or swimming. Additionally, incorporating strength training exercises at least twice a week can help build and maintain muscle mass, which is important for overall health and injury prevention.

A balanced diet is equally important for maintaining good health and potentially reducing insurance costs. Consuming a variety of fruits, vegetables, whole grains, lean proteins, and healthy fats can help prevent chronic diseases such as heart disease, diabetes, and obesity, which are often associated with higher healthcare costs. Limiting processed foods, sugary drinks, and excessive alcohol consumption can also contribute to a healthier lifestyle and potentially lower insurance premiums.

It's important to note that while maintaining a healthy lifestyle can potentially lead to lower premiums, it is not a guarantee. Insurance providers may have specific criteria and requirements that must be met in order to qualify for discounts. Additionally, individuals should always consult with their healthcare provider before starting any new exercise or diet regimen to ensure it is safe and appropriate for their personal health needs.

In conclusion, by prioritizing regular exercise and a balanced diet, individuals can not only improve their overall health but also potentially reduce their health insurance costs. Taking advantage of wellness programs and discounts offered by insurance providers can be a proactive step towards managing healthcare expenses and promoting a healthier lifestyle.

Does Private Health Insurance Cover Overseas Medical Expenses?

You may want to see also

Explore related products

![]()

Consider a Health Savings Account (HSA): Utilize an HSA to save money on taxes and pay for qualified medical expenses

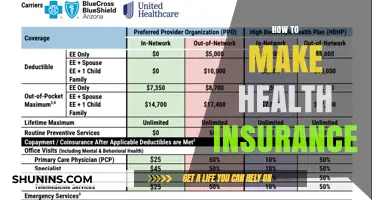

A Health Savings Account (HSA) is a powerful tool for managing healthcare costs and reducing your tax burden. If you're looking to lower your health insurance expenses, an HSA could be a valuable addition to your financial strategy. Here's how it works: an HSA allows you to set aside pre-tax dollars to pay for qualified medical expenses, which can include everything from doctor's visits and prescription medications to dental care and vision services. By using an HSA, you can save money on taxes and pay for these expenses tax-free, as long as you use the funds for eligible healthcare costs.

One of the key benefits of an HSA is its flexibility. Unlike other types of health savings accounts, such as Flexible Spending Accounts (FSAs), HSAs do not require you to spend the money within a specific timeframe. This means you can save the funds for future medical expenses or even use them to pay for long-term care costs. Additionally, HSAs are portable, which means you can take the account with you if you change jobs or retire.

To maximize the benefits of an HSA, it's important to understand the contribution limits and eligibility requirements. As of 2023, individuals can contribute up to $3,650 per year to an HSA, while families can contribute up to $7,300. To be eligible for an HSA, you must have a high-deductible health plan (HDHP) and not be enrolled in Medicare. It's also important to note that you cannot contribute to an HSA if you are covered by a spouse's health insurance plan, unless that plan also meets the HDHP requirements.

When it comes to using your HSA funds, it's essential to keep track of your qualified medical expenses. You can use the funds to pay for a wide range of healthcare costs, including deductibles, copays, and coinsurance. However, you cannot use HSA funds to pay for health insurance premiums, except in certain circumstances, such as when you are receiving unemployment benefits. To avoid any potential tax penalties, it's important to only use your HSA funds for eligible expenses and to keep accurate records of your healthcare costs.

In conclusion, a Health Savings Account can be a valuable tool for lowering your health insurance costs and managing your healthcare expenses. By understanding the contribution limits, eligibility requirements, and qualified medical expenses, you can make the most of this tax-advantaged savings account and take control of your healthcare finances.

Understanding Co-Insurance: A Key Component of Health Insurance Policies

You may want to see also

Frequently asked questions

There are several strategies to lower your health insurance costs. These include choosing a plan with a higher deductible, opting for a Health Savings Account (HSA) or Flexible Spending Account (FSA), and ensuring you're taking advantage of any employer-sponsored wellness programs. Additionally, maintaining a healthy lifestyle, quitting smoking, and comparing plans during open enrollment can also lead to savings.

Increasing your deductible typically results in lower monthly premiums. This is because you're agreeing to pay more out-of-pocket for healthcare services before your insurance coverage kicks in. However, it's important to consider your overall health needs and financial situation to ensure that a higher deductible plan is the right choice for you.

Yes, switching to a different health insurance provider can potentially save you money. It's important to compare plans and prices from multiple providers during open enrollment. Look for plans that offer the coverage you need at a price that fits your budget. Keep in mind that switching providers may also involve changes to your network of doctors and hospitals, so be sure to consider that in your decision-making process.