Health insurance is a critical component of financial planning, providing a safety net against unexpected medical expenses. Creating a comprehensive health insurance policy involves understanding the needs of the insured, assessing risks, and crafting a plan that balances coverage with affordability. This process requires careful consideration of various factors, including the types of medical services covered, the extent of coverage, and the premium costs. Additionally, it's essential to navigate the complex regulatory landscape governing health insurance to ensure compliance with legal requirements. By following a systematic approach, individuals and organizations can design health insurance plans that offer robust protection and peace of mind.

Explore related products

What You'll Learn

- Understanding Health Insurance Basics: Learn about different types of plans, coverage options, and key terminology

- Assessing Your Health Needs: Evaluate your medical history, current health status, and future needs to choose appropriate coverage

- Comparing Insurance Providers: Research and compare various insurance companies based on reputation, cost, and customer service

- Navigating Enrollment Periods: Understand open enrollment periods, special enrollment rights, and how to apply for coverage

- Managing Costs and Benefits: Learn how to estimate healthcare costs, understand deductibles and copays, and maximize your benefits

![]()

Understanding Health Insurance Basics: Learn about different types of plans, coverage options, and key terminology

Health insurance is a critical component of financial planning, yet many individuals find it challenging to navigate the complex landscape of options available. Understanding the basics of health insurance is essential for making informed decisions about coverage. There are several types of health insurance plans, each with its own set of benefits and drawbacks.

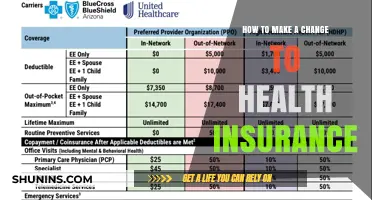

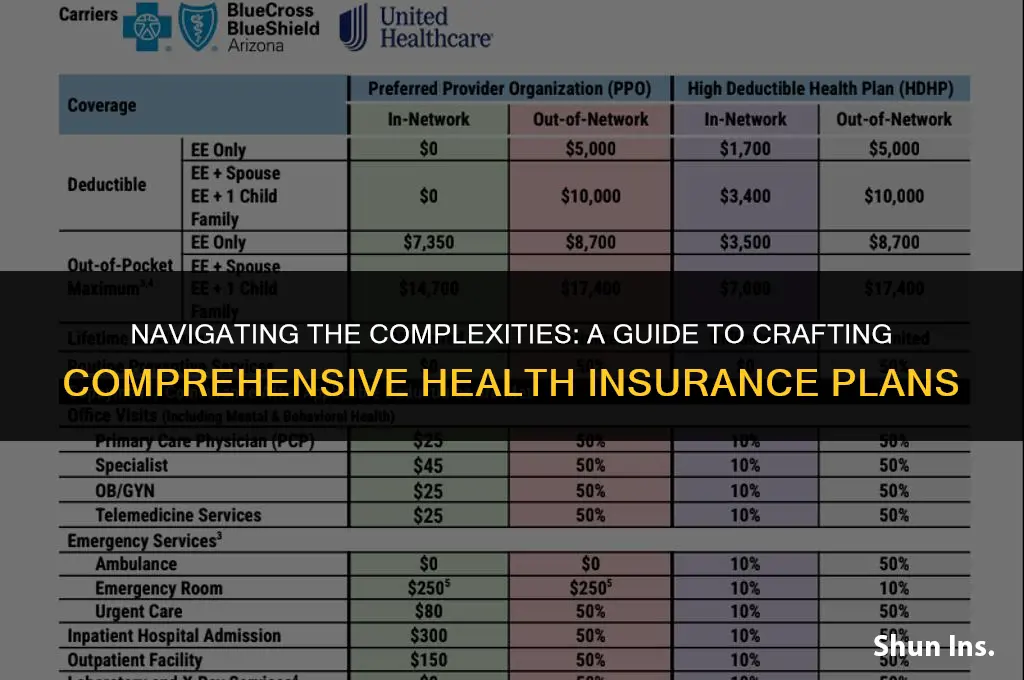

One common type of health insurance plan is the Preferred Provider Organization (PPO). PPOs offer a network of preferred providers, and policyholders can choose to see doctors within or outside this network. However, seeing providers outside the network typically results in higher out-of-pocket costs. Another option is the Health Maintenance Organization (HMO), which requires policyholders to see providers within a specific network and often necessitates a referral from a primary care physician to see a specialist. HMOs tend to have lower premiums but more restrictive coverage compared to PPOs.

Coverage options vary widely among health insurance plans. Some plans offer comprehensive coverage, including preventive care, prescription drugs, and mental health services, while others may have more limited benefits. It's important to carefully review the coverage details of each plan to ensure it meets your specific needs. Key terminology to understand includes premiums (the monthly cost of the plan), deductibles (the amount you must pay out-of-pocket before the plan begins to cover costs), copays (a fixed amount you pay for each service), and coinsurance (a percentage of the cost you pay after meeting the deductible).

When selecting a health insurance plan, it's crucial to consider your individual circumstances, such as your age, health status, and financial situation. For example, younger, healthier individuals may opt for a high-deductible plan with lower premiums, while older individuals or those with chronic health conditions may prefer a plan with more comprehensive coverage and higher premiums. Additionally, it's important to be aware of any subsidies or tax credits you may be eligible for, which can help offset the cost of premiums.

In conclusion, understanding the basics of health insurance is key to making informed decisions about coverage. By familiarizing yourself with different types of plans, coverage options, and key terminology, you can better navigate the complex world of health insurance and select a plan that meets your unique needs and budget.

The Legal Ramifications of Falsifying Health Insurance Status

You may want to see also

Explore related products

![Life and Health Insurance License Study Cards: Life Health Insurance Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Assessing Your Health Needs: Evaluate your medical history, current health status, and future needs to choose appropriate coverage

To effectively assess your health needs for appropriate insurance coverage, begin by gathering comprehensive information about your medical history. This includes documenting any chronic conditions, past surgeries, medications, and hospitalizations. Understanding your medical background is crucial as it directly impacts the type and extent of coverage you may require. For instance, individuals with pre-existing conditions may need policies that offer more extensive benefits or have specific clauses addressing their health needs.

Next, evaluate your current health status. This involves considering your age, lifestyle, and any recent health changes or concerns. Are you experiencing any symptoms that might indicate an underlying condition? Have you recently undergone any medical tests or check-ups? The answers to these questions can help you determine if you need immediate coverage for potential health issues or if you can opt for a more basic plan.

Looking ahead, anticipate your future health needs. This might involve considering family medical history, potential risks associated with your lifestyle or occupation, and common health issues that arise with aging. For example, if heart disease runs in your family, you may want to ensure your insurance covers cardiac care. Similarly, if you work in a physically demanding job, you might prioritize coverage for musculoskeletal disorders.

When choosing appropriate coverage, it's essential to balance cost with the level of protection you need. Analyze different insurance plans, comparing their premiums, deductibles, co-pays, and coverage limits. Consider using online comparison tools or consulting with an insurance agent to find a policy that aligns with your health needs and budget.

Finally, don't overlook the importance of preventive care. Many insurance plans now cover preventive services such as annual check-ups, vaccinations, and screenings at no additional cost. By prioritizing preventive care, you can potentially avoid more significant health issues down the road, reducing your overall healthcare expenses and improving your quality of life.

Understanding Deductible Waivers in Medical Insurance Plans

You may want to see also

Explore related products

$75.4 $257.95

![]()

Comparing Insurance Providers: Research and compare various insurance companies based on reputation, cost, and customer service

To effectively compare insurance providers, begin by gathering information from reputable sources such as consumer reports, industry ratings, and customer reviews. Websites like the Better Business Bureau, Consumer Affairs, and Trustpilot can offer valuable insights into the reputation and customer service quality of various insurance companies. Additionally, consider consulting with insurance comparison websites that aggregate data on cost and coverage options from multiple providers.

When evaluating insurance companies, it's crucial to consider both the cost and the value of the coverage offered. While lower premiums may be attractive, it's important to ensure that the policy provides adequate coverage for your specific needs. Compare the deductibles, co-pays, and out-of-pocket maximums associated with each plan to get a comprehensive understanding of the potential costs you may incur.

Customer service is another key factor to consider when comparing insurance providers. Look for companies that have a reputation for responsive and helpful customer support. This can include factors such as the availability of 24/7 customer service, the ease of filing claims, and the overall satisfaction of policyholders with the claims process.

In addition to these factors, consider the financial stability and longevity of the insurance companies you are comparing. A company with a strong financial rating is more likely to be able to meet its obligations and provide reliable coverage. You can check the financial ratings of insurance companies through organizations like A.M. Best, Moody's, and Standard & Poor's.

Finally, take the time to read and understand the terms and conditions of each policy you are considering. Pay close attention to any exclusions, limitations, or special provisions that may affect your coverage. By carefully comparing insurance providers based on reputation, cost, and customer service, you can make an informed decision that meets your specific insurance needs.

Empowering Communities: Effective Strategies to Promote Health Insurance Awareness

You may want to see also

Explore related products

![]()

Navigating Enrollment Periods: Understand open enrollment periods, special enrollment rights, and how to apply for coverage

Open enrollment periods are a critical time for individuals and families to select or change their health insurance coverage. These periods typically occur once a year and are set by the health insurance marketplace or employer-sponsored plan. During open enrollment, you have the opportunity to review your current plan, compare it with other available options, and make changes if necessary. It's essential to mark your calendar and set reminders to ensure you don't miss this window, as late enrollment may result in penalties or delays in coverage.

Special enrollment rights (SERs) allow individuals to enroll in or change health insurance plans outside of the regular open enrollment period under certain circumstances. These circumstances may include losing job-based coverage, experiencing a significant life change such as marriage or the birth of a child, or moving to a new state. To qualify for an SER, you must provide documentation supporting the qualifying event. This can include a letter from your employer, a marriage certificate, or a birth certificate. It's crucial to understand the specific requirements and deadlines for SERs, as they can vary depending on the type of plan and the state you live in.

Applying for health insurance coverage during open enrollment or an SER involves several steps. First, you'll need to gather necessary information, such as your income, household size, and current health insurance details. Next, you'll need to research available plans and compare their benefits, premiums, and out-of-pocket costs. You can use online tools or consult with a licensed insurance agent to help with this process. Once you've selected a plan, you'll need to complete the application, which may require providing additional documentation or undergoing a medical underwriting process. Finally, you'll need to pay the first month's premium to activate your coverage.

Navigating enrollment periods can be complex, but there are resources available to help. The health insurance marketplace website, employer-sponsored plan materials, and licensed insurance agents can provide guidance and support throughout the process. It's essential to take the time to understand your options and make informed decisions about your health insurance coverage. By doing so, you can ensure that you and your family have the protection and peace of mind that comes with having adequate health insurance.

Verify Insurance: Medical Assistant's Step-by-Step Guide

You may want to see also

Explore related products

$77.92 $232.95

![]()

Managing Costs and Benefits: Learn how to estimate healthcare costs, understand deductibles and copays, and maximize your benefits

Understanding healthcare costs is crucial for effective financial planning. Start by reviewing your insurance policy's Summary of Benefits and Coverage (SBC), which provides an estimate of costs for various services. Additionally, many insurers offer online tools or mobile apps that allow you to compare costs for different treatments and providers. When evaluating costs, consider not only the immediate expenses but also potential long-term costs, such as follow-up care or medication.

Deductibles and copays are key components of your health insurance plan that directly impact your out-of-pocket expenses. A deductible is the amount you must pay before your insurance coverage kicks in, while a copay is a fixed amount you pay for each service or prescription. To manage these costs, consider choosing a plan with a lower deductible if you anticipate frequent medical visits, or opt for a higher deductible plan if you're generally healthy and want lower monthly premiums.

Maximizing your benefits involves understanding the specifics of your coverage and taking advantage of available resources. For instance, many plans cover preventive care services, such as annual check-ups and vaccinations, at no cost to you. Additionally, some insurers offer wellness programs or discounts for healthy behaviors, such as gym memberships or smoking cessation programs. To get the most out of your benefits, review your policy regularly and stay informed about any changes or updates.

When navigating healthcare costs, it's essential to be proactive and advocate for yourself. Don't hesitate to ask your provider about the cost of a service or treatment, and explore options for reducing expenses, such as generic medications or alternative therapies. Furthermore, consider using a Health Savings Account (HSA) or Flexible Spending Account (FSA) to set aside pre-tax dollars for medical expenses, which can help you save money over time.

In conclusion, managing healthcare costs and benefits requires a combination of understanding your coverage, being proactive in your healthcare decisions, and taking advantage of available resources. By following these strategies, you can effectively navigate the complexities of health insurance and make informed choices that benefit both your health and your wallet.

Health Insurance Mandate: What Small Businesses Need to Know

You may want to see also

Frequently asked questions

To create a health insurance plan, you need to: 1) Define the scope and objectives of the plan, 2) Identify the target population, 3) Determine the benefits and coverage, 4) Set premiums and cost-sharing mechanisms, 5) Establish a network of healthcare providers, and 6) Develop a system for claims processing and payment.

Determining benefits and coverage involves assessing the healthcare needs of the target population, considering the cost of medical services, and deciding on the level of financial protection you want to offer. This may include coverage for hospital stays, doctor visits, prescription drugs, and preventive care.

When setting premiums, consider the cost of healthcare services in your area, the demographics of your target population, the level of coverage you're offering, and the financial stability of your insurance company. Premiums should be set high enough to cover expected claims and administrative costs but remain affordable for policyholders.

To ensure compliance, familiarize yourself with federal and state laws governing health insurance, such as the Affordable Care Act (ACA) and state insurance codes. Consult with legal experts, develop policies and procedures that meet regulatory standards, and regularly review and update your plan to reflect changes in the law.