The topic of making money in health insurance is a complex and multifaceted one, requiring a deep understanding of the industry, its regulations, and the various players involved. At its core, the health insurance industry is a business, and like any business, it operates on the principles of supply and demand, risk management, and profit maximization. To make money in health insurance, one must first understand the different ways in which revenue can be generated, such as through premiums, investments, and cost-sharing arrangements. Additionally, it is essential to grasp the regulatory framework that governs the industry, including laws related to healthcare reform, insurance licensing, and consumer protection. By combining this knowledge with strategic thinking and innovative approaches, individuals and organizations can identify opportunities to create value and generate profits within the health insurance market.

Explore related products

What You'll Learn

- Understanding Health Insurance Plans: Learn about different types of health insurance plans and their benefits

- Comparing Health Insurance Providers: Evaluate various health insurance companies based on coverage, cost, and customer reviews

- Maximizing Health Insurance Benefits: Discover ways to optimize your health insurance plan to save money on medical expenses

- Navigating Health Insurance Enrollment: Get guidance on how to enroll in a health insurance plan during open enrollment periods

- Health Insurance for Small Businesses: Explore health insurance options for small business owners and their employees

![]()

Understanding Health Insurance Plans: Learn about different types of health insurance plans and their benefits

Health insurance plans can be complex and overwhelming, but understanding the different types and their benefits is crucial for making informed decisions. There are several main categories of health insurance plans, each with its own unique features and advantages.

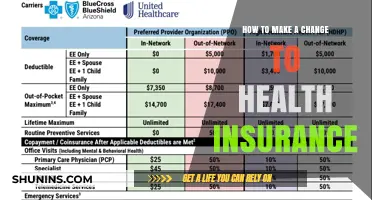

One of the most common types of health insurance plans is the Preferred Provider Organization (PPO) plan. PPO plans offer a network of preferred providers, and policyholders can choose to see any provider within the network without needing a referral. These plans typically have lower premiums and out-of-pocket costs compared to other types of plans. However, policyholders may face higher costs if they choose to see a provider outside of the network.

Another popular option is the Health Maintenance Organization (HMO) plan. HMO plans require policyholders to choose a primary care physician and obtain referrals for specialist care. These plans often have lower premiums and out-of-pocket costs than PPO plans, but they may also have more restrictions on provider choice and coverage.

For those who are self-employed or work for a small business, a Health Savings Account (HSA) plan may be a good option. HSA plans are tax-advantaged accounts that allow policyholders to save money for medical expenses. These plans typically have lower premiums than traditional health insurance plans, but they may also have higher deductibles.

When choosing a health insurance plan, it's important to consider factors such as premium cost, out-of-pocket costs, provider choice, and coverage. By understanding the different types of health insurance plans and their benefits, individuals can make informed decisions that meet their unique needs and budget.

Exploring Yale Specialty Health Insurance: Comprehensive Coverage Details

You may want to see also

Explore related products

![]()

Comparing Health Insurance Providers: Evaluate various health insurance companies based on coverage, cost, and customer reviews

Evaluating health insurance providers is a critical step in ensuring you receive the best possible coverage at a reasonable cost. When comparing different companies, it's essential to consider several key factors: coverage options, premium costs, and customer reviews. Coverage options vary widely among providers, with some offering comprehensive plans that include vision and dental care, while others may have more limited options. Premium costs are also a significant consideration, as they can vary greatly depending on the provider and the specific plan you choose. Customer reviews can provide valuable insights into the quality of service and the ease of claims processing.

To begin your evaluation, start by researching the top health insurance providers in your area. Look for companies that offer a range of coverage options to meet your specific needs. Once you have a list of potential providers, compare their premium costs for similar coverage levels. Be sure to consider any additional fees or out-of-pocket expenses that may be associated with each plan. Next, read customer reviews and ratings to get a sense of the overall satisfaction of policyholders. Pay attention to any recurring complaints or praises about the company's service.

Another important factor to consider is the provider's network of healthcare professionals. Ensure that the company has a robust network of doctors, hospitals, and specialists in your area. This can help you avoid out-of-network fees and ensure that you have access to quality care. Additionally, consider the company's financial stability and reputation. A provider with a strong financial rating and a long history of customer satisfaction is more likely to be a reliable choice.

When comparing health insurance providers, it's also essential to consider the specific benefits and features of each plan. Some plans may offer additional perks, such as wellness programs, telemedicine services, or prescription drug coverage. Evaluate these features based on your individual needs and preferences. Finally, don't hesitate to reach out to the providers directly to ask questions or clarify any uncertainties you may have about their plans.

In conclusion, evaluating health insurance providers requires careful consideration of several factors, including coverage options, premium costs, customer reviews, network strength, and additional benefits. By taking the time to research and compare different providers, you can find a plan that meets your specific needs and provides you with the best possible coverage at a reasonable cost.

Why Insurance Companies Offer Lower Advance Commissions: Key Factors Explained

You may want to see also

Explore related products

![]()

Maximizing Health Insurance Benefits: Discover ways to optimize your health insurance plan to save money on medical expenses

To maximize health insurance benefits and save on medical expenses, it's crucial to understand the specifics of your plan. Start by thoroughly reviewing your policy documents to grasp the coverage details, including deductibles, copays, and coinsurance. Familiarize yourself with the network of providers to ensure you're receiving care from in-network professionals, which can significantly reduce out-of-pocket costs.

One effective strategy is to take advantage of preventive care services, which are often fully covered by insurance plans. Regular check-ups, vaccinations, and screenings can help detect potential health issues early, preventing more costly treatments down the line. Additionally, consider utilizing telemedicine services for non-urgent medical consultations, as these can be more affordable and convenient than in-person visits.

When it comes to prescription medications, explore options for cost savings. Many insurance plans offer prescription drug coverage, but it's essential to understand the formulary and any associated costs. Consider opting for generic medications, which are typically less expensive than brand-name drugs. You may also benefit from using mail-order pharmacies or prescription discount cards to further reduce medication costs.

Another way to optimize your health insurance plan is to be mindful of your health savings account (HSA) or flexible spending account (FSA). These accounts allow you to set aside pre-tax dollars for qualified medical expenses, providing a tax-advantaged way to save for healthcare costs. Be sure to contribute the maximum amount allowed by your plan and use the funds wisely to cover deductibles, copays, and other eligible expenses.

Lastly, stay informed about changes to your insurance plan and the broader healthcare landscape. Insurance providers may update their policies, networks, or coverage options, so it's essential to stay up-to-date to ensure you're making the most of your benefits. By being proactive and informed, you can effectively maximize your health insurance benefits and minimize your medical expenses.

Postal Retirees: Understanding Medicare and Your Insurance Options

You may want to see also

Explore related products

![]()

Navigating Health Insurance Enrollment: Get guidance on how to enroll in a health insurance plan during open enrollment periods

During open enrollment periods, individuals have the opportunity to enroll in a health insurance plan or make changes to their existing coverage. This is a critical time for those looking to secure affordable and comprehensive health insurance. To navigate this process successfully, it's essential to understand the key steps and considerations involved.

First, it's important to research and compare different health insurance plans available in your area. This can be done through online marketplaces, insurance company websites, or by consulting with a licensed insurance agent. When comparing plans, consider factors such as premiums, deductibles, copays, and coverage limits. Additionally, check to see if your preferred healthcare providers are included in the plan's network.

Once you've selected a plan, you'll need to gather the necessary documentation to enroll. This typically includes proof of identity, income, and citizenship or immigration status. You may also need to provide information about your health history, including any pre-existing conditions.

After submitting your application and required documents, you'll receive a confirmation of your enrollment. Be sure to review the details of your plan carefully, including the effective date of your coverage and any associated costs. It's also important to keep track of your enrollment period, as missing the deadline could result in a gap in coverage.

To make the most of your health insurance, it's crucial to understand your benefits and how to access them. This includes knowing your deductible, copay, and coinsurance amounts, as well as any limitations or exclusions on your coverage. By familiarizing yourself with your plan details, you can make informed decisions about your healthcare and avoid unexpected costs.

In conclusion, navigating health insurance enrollment requires careful research, documentation, and attention to detail. By following these steps and staying informed about your coverage options, you can secure the health insurance that best meets your needs and budget.

Your Guide to Applying for Health Insurance in Virginia

You may want to see also

Explore related products

![]()

Health Insurance for Small Businesses: Explore health insurance options for small business owners and their employees

Small business owners often find themselves in a unique position when it comes to health insurance. They must balance the need to provide competitive benefits to attract and retain employees with the financial constraints of running a small business. One option that has gained popularity in recent years is the use of Health Savings Accounts (HSAs). HSAs allow employees to save money on a tax-free basis for qualified medical expenses, and they can be a cost-effective alternative to traditional health insurance plans.

Another option for small businesses is to consider a Flexible Spending Account (FSA). FSAs are similar to HSAs in that they allow employees to save money on a tax-free basis for medical expenses. However, FSAs are typically only available to employees who are enrolled in a health insurance plan, and the funds must be used within a specific timeframe. Small business owners may also want to explore the possibility of offering a Health Reimbursement Arrangement (HRA). HRAs allow employers to reimburse employees for qualified medical expenses, and they can be a flexible and cost-effective way to provide health benefits.

When considering health insurance options for small businesses, it's important to keep in mind the specific needs of the business and its employees. For example, a business with a large number of employees may benefit from a group health insurance plan, while a business with a small number of employees may find it more cost-effective to offer individual plans. Additionally, small business owners should consider the age and health status of their employees when selecting a health insurance plan.

One of the key factors that small business owners should consider when choosing a health insurance plan is the cost. Health insurance premiums can be a significant expense for small businesses, and it's important to find a plan that is affordable while still providing adequate coverage. Small business owners may also want to consider the administrative costs associated with managing a health insurance plan, as these can add up quickly.

Finally, small business owners should be aware of the changing landscape of health insurance regulations. The Affordable Care Act (ACA) has had a significant impact on the health insurance industry, and small business owners need to stay up-to-date on the latest changes in order to make informed decisions about their health insurance options. By carefully considering the unique needs of their business and employees, small business owners can find a health insurance plan that is both cost-effective and provides the necessary coverage.

Simplifying BCBS Health Insurance Payments: A Step-by-Step Guide

You may want to see also

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61eAQwSUEcL._AC_UY218_.jpg)