Navigating the complexities of health insurance can be a daunting task, but with the right knowledge and strategies, you can maximize your benefits and minimize your out-of-pocket expenses. This guide will walk you through the essential steps to make the most out of your health insurance plan. From understanding your coverage and network to effectively managing your claims and appeals, we'll provide you with the tools and insights you need to become a savvy healthcare consumer. Whether you're new to health insurance or looking to optimize your existing plan, this comprehensive resource will empower you to take control of your healthcare costs and ensure you're getting the best possible care.

Explore related products

What You'll Learn

- Understanding Your Coverage: Know what's included and excluded in your plan to avoid unexpected costs

- Maximizing Preventive Care: Utilize free preventive services like check-ups and screenings to catch issues early

- Choosing In-Network Providers: Stay within your network to minimize out-of-pocket expenses and ensure coverage

- Managing Chronic Conditions: Learn how to manage ongoing health issues effectively to reduce long-term costs

- Appealing Denied Claims: Understand the process to appeal if your insurance claim is denied, potentially reversing the decision

![]()

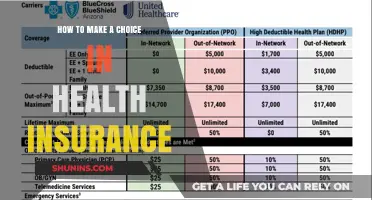

Understanding Your Coverage: Know what's included and excluded in your plan to avoid unexpected costs

Understanding your health insurance coverage is crucial to avoid unexpected costs and make the most out of your plan. Start by thoroughly reviewing your policy documents to familiarize yourself with what is included and excluded. Pay close attention to the fine print, as it often contains important details about coverage limitations and requirements.

One key aspect to understand is the difference between in-network and out-of-network providers. In-network providers have agreed to charge lower rates to plan members, while out-of-network providers may charge higher rates or not be covered at all. Make sure to choose in-network providers whenever possible to minimize your out-of-pocket expenses.

Another important consideration is the coverage for prescription medications. Check your plan's formulary to see which medications are covered and at what cost. Some plans may have tiered coverage, where generic medications are covered at a lower cost than brand-name medications. Understanding your medication coverage can help you make informed decisions about your healthcare and avoid unexpected costs.

Additionally, be aware of any pre-authorization requirements for certain procedures or treatments. Many insurance plans require pre-authorization for expensive or elective procedures to ensure that they are medically necessary. Failing to obtain pre-authorization can result in denied coverage and significant out-of-pocket expenses.

Finally, take advantage of preventive care benefits offered by your plan. Many insurance plans cover preventive services, such as annual check-ups, vaccinations, and screenings, at no cost to you. Utilizing these benefits can help you maintain your health and potentially avoid more costly medical issues down the line.

By understanding your coverage, choosing in-network providers, reviewing medication coverage, obtaining pre-authorization when necessary, and utilizing preventive care benefits, you can make the most out of your health insurance plan and avoid unexpected costs.

Understanding the Health Insurance Industry: Sector, Role, and Impact

You may want to see also

Explore related products

![]()

Maximizing Preventive Care: Utilize free preventive services like check-ups and screenings to catch issues early

Preventive care is a cornerstone of maintaining good health and making the most out of your health insurance. By utilizing free preventive services such as regular check-ups and screenings, you can catch potential health issues early, when they are often easier and less expensive to treat. This proactive approach not only helps in avoiding more serious health complications down the line but also ensures that you are getting the most value from your insurance coverage.

One of the key benefits of preventive care is that it can help identify risk factors and early signs of diseases that might otherwise go unnoticed. For example, regular blood pressure screenings can detect hypertension early, allowing for lifestyle changes or medication to be introduced before it leads to more severe conditions like heart disease or stroke. Similarly, routine dental check-ups can prevent cavities and gum disease, which, if left untreated, could result in costly procedures and long-term oral health issues.

To maximize the benefits of preventive care, it's important to stay informed about the specific services covered by your health insurance plan. Many plans cover annual physical exams, certain vaccinations, and screenings for conditions like diabetes, cholesterol, and cancer at no cost to you. By understanding what is covered, you can take advantage of these services and work with your healthcare provider to develop a personalized preventive care plan.

In addition to the direct health benefits, preventive care can also have a positive impact on your finances. By catching and treating health issues early, you can avoid the high costs associated with emergency room visits, hospital stays, and extensive treatments that are often required for more advanced conditions. This not only helps in reducing your out-of-pocket expenses but also contributes to keeping your insurance premiums lower by reducing the overall cost of healthcare for everyone.

To make the most out of preventive care, it's crucial to be proactive and consistent. Schedule regular appointments with your healthcare provider, follow through with recommended screenings and vaccinations, and take an active role in your health by maintaining a healthy lifestyle, including proper diet, exercise, and stress management. By doing so, you can ensure that you are getting the most out of your health insurance and setting yourself up for a lifetime of good health.

Proving Medicare Insurance for Taxes: A Guide

You may want to see also

Explore related products

![]()

Choosing In-Network Providers: Stay within your network to minimize out-of-pocket expenses and ensure coverage

Choosing in-network providers is a crucial strategy for maximizing the benefits of your health insurance plan. By staying within your network, you can significantly reduce your out-of-pocket expenses and ensure that your coverage is fully utilized. This approach is particularly important for individuals who have high-deductible plans or those who are looking to minimize their overall healthcare costs.

One of the key advantages of using in-network providers is that they have negotiated rates with your insurance company, which are typically lower than the rates charged by out-of-network providers. This means that when you visit an in-network doctor or hospital, your insurance company will pay a larger portion of the bill, leaving you with a smaller copay or coinsurance amount. Additionally, in-network providers are more likely to be familiar with your insurance plan's coverage and limitations, which can help to prevent unexpected charges or denials of coverage.

To make the most of this strategy, it's important to carefully review your insurance plan's provider directory and familiarize yourself with the in-network options available to you. This may involve researching the credentials and experience of different providers, as well as considering factors such as location, office hours, and patient reviews. By taking the time to select a provider who is both in-network and well-suited to your individual needs, you can ensure that you receive high-quality care while also minimizing your financial burden.

Another benefit of choosing in-network providers is that it can help to streamline the claims process. When you receive care from an in-network provider, they will typically handle the billing and claims submission process for you, which can save you time and hassle. Additionally, in-network providers are more likely to be subject to your insurance company's utilization review and quality assurance processes, which can help to ensure that you receive appropriate and effective care.

In conclusion, choosing in-network providers is a smart and effective way to make the most of your health insurance plan. By staying within your network, you can reduce your out-of-pocket expenses, ensure that your coverage is fully utilized, and enjoy a more streamlined claims process. To maximize the benefits of this strategy, be sure to carefully review your provider directory, research your options, and select a provider who is both in-network and well-suited to your individual needs.

Medical Insurance Enrollment: Anytime Access and Flexibility

You may want to see also

Explore related products

![]()

Managing Chronic Conditions: Learn how to manage ongoing health issues effectively to reduce long-term costs

Chronic conditions such as diabetes, hypertension, and asthma can significantly impact one's quality of life and financial well-being. Effective management of these conditions is crucial not only for maintaining good health but also for reducing long-term healthcare costs. Here are some strategies to help you manage chronic conditions more effectively:

Firstly, it's essential to have a comprehensive understanding of your condition. This includes knowing the symptoms, triggers, and appropriate treatment options. Educate yourself by consulting with healthcare professionals, reading reputable sources, and attending patient education programs. The more informed you are, the better equipped you'll be to make informed decisions about your health.

Secondly, adherence to treatment plans is vital. This may include taking medications as prescribed, monitoring your condition regularly, and making necessary lifestyle changes. For example, if you have diabetes, maintaining a healthy diet, exercising regularly, and monitoring your blood sugar levels can help prevent complications and reduce the need for costly interventions.

Thirdly, regular check-ups with your healthcare provider can help detect potential issues early on, allowing for timely intervention and preventing more severe complications. This can lead to significant cost savings in the long run. Additionally, many health insurance plans cover preventive care services, such as annual physicals and screenings, at little or no cost to you.

Lastly, consider utilizing technology to help manage your condition. There are numerous mobile apps and devices available that can assist with tracking symptoms, medication adherence, and overall health monitoring. These tools can provide valuable insights and help you stay on top of your health, potentially reducing the need for frequent doctor visits and associated costs.

By implementing these strategies, you can take control of your chronic condition and work towards reducing the financial burden associated with long-term healthcare. Remember, effective management is key to maintaining good health and making the most out of your health insurance.

Medical Expense Insurance: 3 Basic Coverages for Peace of Mind

You may want to see also

Explore related products

$14.52 $30

![]()

Appealing Denied Claims: Understand the process to appeal if your insurance claim is denied, potentially reversing the decision

If your health insurance claim has been denied, it's crucial to understand that you have the right to appeal the decision. The appeals process can be complex, but with the right approach, you may be able to reverse the denial and receive the coverage you need. Here's a step-by-step guide to help you navigate the appeals process effectively.

First, carefully review the denial letter from your insurance provider. This letter should outline the specific reasons why your claim was denied, as well as the steps you need to take to appeal the decision. Pay close attention to any deadlines mentioned, as you typically have a limited amount of time to file an appeal.

Next, gather all relevant documentation to support your appeal. This may include medical records, receipts for out-of-pocket expenses, and any correspondence between you and your healthcare provider. Organize these documents in a clear and concise manner, making it easy for the appeals committee to review your case.

When filing your appeal, be sure to clearly state the reasons why you believe the denial was incorrect. Use specific examples from your medical records or other documentation to support your argument. It's also important to remain calm and professional throughout the appeals process, as emotions can run high when dealing with healthcare coverage.

If your initial appeal is denied, don't give up. You may have the option to file a second appeal or even request a review by an independent medical professional. Keep in mind that the appeals process can be time-consuming, so it's essential to stay organized and persistent.

Finally, consider seeking assistance from a healthcare advocate or a legal professional who specializes in insurance appeals. These experts can provide valuable guidance and support throughout the appeals process, increasing your chances of a successful outcome. Remember, appealing a denied claim is your right, and with the proper approach, you may be able to secure the healthcare coverage you deserve.

Supporting Veterans' Families: Understanding Health Insurance Options and Benefits

You may want to see also

Frequently asked questions

When selecting a health insurance plan, consider factors such as your budget, health needs, and preferred healthcare providers. Compare different plans based on their premiums, deductibles, copays, and coverage limits. Also, check if the plan includes prescription drug coverage and mental health services. It's essential to choose a plan that aligns with your healthcare needs and financial situation.

To make the most out of your health insurance, understand your plan's details, including what services are covered and what your out-of-pocket costs will be. Use in-network healthcare providers to minimize expenses, and take advantage of preventive care services that are often fully covered. Additionally, review your plan's formulary to ensure your medications are covered, and consider using generic drugs when possible to save money.

If you have a dispute with your health insurance provider, start by reviewing your plan documents to understand your rights and the appeals process. Contact your provider's customer service department to discuss the issue and seek a resolution. If you're not satisfied with the response, you can file a formal appeal or complaint with your state's insurance department. Keep detailed records of all communications and documentation related to your dispute for future reference.