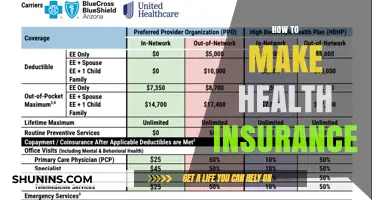

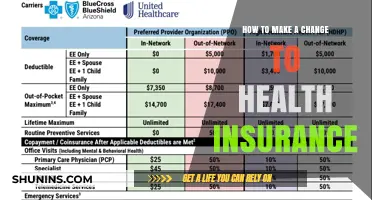

The high cost of health insurance in the USA is a pressing concern for many individuals and families. With premiums, deductibles, and out-of-pocket expenses continually rising, finding ways to make health insurance more affordable is crucial. This article will explore several strategies to reduce the cost of health insurance, including negotiating with providers, taking advantage of tax credits and subsidies, and considering alternative insurance options. By implementing these strategies, individuals can potentially save hundreds or even thousands of dollars on their annual health insurance costs.

Explore related products

What You'll Learn

- Increase competition among insurance providers to drive down prices and improve service quality

- Implement cost-sharing measures like higher deductibles and copays to reduce insurer payouts

- Expand Medicaid and subsidies to cover more low-income individuals and families

- Encourage preventive care and wellness programs to lower long-term healthcare costs

- Streamline administrative processes and reduce regulatory burdens to decrease operational expenses

![]()

Increase competition among insurance providers to drive down prices and improve service quality

One effective strategy to reduce health insurance costs in the USA is to increase competition among insurance providers. This can be achieved by implementing policies that encourage new entrants into the market and remove barriers to entry. For instance, states could eliminate licensing requirements that are overly burdensome or restrictive, allowing more companies to offer insurance plans. Additionally, the federal government could provide incentives for new insurance startups, such as tax breaks or grants, to help them establish a foothold in the market.

Another approach to fostering competition is to promote transparency in pricing and service quality. This could involve creating a centralized platform where consumers can easily compare insurance plans and their associated costs. By making it simpler for individuals to shop around for the best deal, insurance companies would be incentivized to lower their prices and improve their offerings to remain competitive. Furthermore, regulatory bodies could mandate that insurance providers disclose detailed information about their pricing structures and service metrics, enabling consumers to make more informed decisions.

Increasing competition could also involve expanding the role of health insurance exchanges established under the Affordable Care Act. These exchanges currently serve as marketplaces where individuals and small businesses can purchase insurance plans. By enhancing these exchanges and making them more accessible, more consumers could benefit from the competitive pricing and improved service quality that result from increased market competition.

Moreover, policymakers could explore the idea of introducing non-profit insurance cooperatives as an alternative to traditional for-profit insurance companies. These cooperatives would be owned and operated by their members, with any profits reinvested into improving services or reducing premiums. This model could potentially lead to lower costs and better service, as the focus would be on meeting the needs of members rather than maximizing profits for shareholders.

In conclusion, increasing competition among insurance providers is a promising approach to making health insurance more affordable in the USA. By implementing policies that encourage new market entrants, promote transparency, and support consumer choice, policymakers can drive down prices and improve service quality, ultimately benefiting consumers across the country.

Accident Insurance: Understanding Coverage and Its Benefits

You may want to see also

Explore related products

![]()

Implement cost-sharing measures like higher deductibles and copays to reduce insurer payouts

One approach to reducing health insurance costs in the USA is to implement cost-sharing measures such as higher deductibles and copays. This strategy shifts a greater portion of healthcare expenses from insurers to consumers, potentially leading to lower premiums. Here's a detailed exploration of this concept:

Analyzing the Impact of Higher Deductibles and Copays

Higher deductibles and copays can reduce insurer payouts by encouraging policyholders to be more mindful of their healthcare spending. When individuals are required to pay more out-of-pocket, they may be less likely to seek unnecessary medical treatments or choose more expensive options. This behavioral change can lead to significant cost savings for insurers, which could then be passed on to consumers in the form of lower premiums.

Potential Benefits and Drawbacks

The benefits of higher deductibles and copays include reduced insurer costs, potentially leading to lower premiums for policyholders. Additionally, this cost-sharing approach can promote more responsible healthcare consumption, as individuals are more likely to consider the cost-effectiveness of treatments. However, there are also drawbacks to consider. Higher out-of-pocket costs can be a significant financial burden for low-income individuals or those with chronic health conditions, potentially leading to delayed or foregone care. This could result in poorer health outcomes and higher long-term costs for the healthcare system.

Implementing Cost-Sharing Measures Effectively

To implement cost-sharing measures effectively, insurers and policymakers must strike a balance between cost reduction and ensuring access to necessary care. This could involve setting deductibles and copays at levels that are high enough to encourage cost-conscious behavior but not so high as to deter individuals from seeking essential medical attention. Additionally, cost-sharing measures could be paired with other strategies, such as health savings accounts or subsidies for low-income individuals, to mitigate the financial impact on vulnerable populations.

In conclusion, implementing cost-sharing measures like higher deductibles and copays can be an effective way to reduce health insurance costs in the USA. However, it is crucial to carefully consider the potential benefits and drawbacks and to implement these measures in a way that promotes responsible healthcare consumption while ensuring access to necessary care for all individuals. By doing so, policymakers and insurers can work towards creating a more sustainable and affordable healthcare system.

Does Health Insurance Cover Outpatient Drug Rehab? What You Need to Know

You may want to see also

Explore related products

![]()

Expand Medicaid and subsidies to cover more low-income individuals and families

One effective strategy to make health insurance more affordable in the USA is to expand Medicaid and subsidies to cover a broader range of low-income individuals and families. This approach directly addresses the financial barriers that prevent many Americans from accessing necessary healthcare services. By increasing the eligibility criteria for Medicaid, more people can benefit from this government-funded program, which provides comprehensive health coverage at little to no cost for those who qualify.

In addition to expanding Medicaid, enhancing subsidies for health insurance premiums can significantly reduce the financial burden on low-income families. Subsidies can be provided through various mechanisms, such as tax credits or direct payments to insurance companies, which then lower the premium costs for eligible individuals. This not only makes health insurance more accessible but also encourages more people to enroll in health plans, thereby increasing the overall health of the population and reducing the long-term costs associated with untreated medical conditions.

Implementing these measures requires careful consideration of the administrative and fiscal implications. States and the federal government must work together to streamline the application and enrollment processes, ensuring that eligible individuals can easily access Medicaid and subsidies. Furthermore, it is essential to allocate sufficient funding to support the expansion of these programs without compromising the quality of care provided.

Critics may argue that expanding Medicaid and subsidies could lead to increased government spending and potential abuse of the system. However, numerous studies have shown that Medicaid expansion can lead to significant cost savings in the long run by reducing the number of uninsured individuals and the associated costs of emergency care and untreated chronic conditions. Moreover, robust oversight and monitoring mechanisms can be put in place to prevent fraud and ensure that only those who truly need assistance receive it.

In conclusion, expanding Medicaid and subsidies is a crucial step in making health insurance more affordable and accessible in the USA. By targeting low-income individuals and families, this approach can help bridge the healthcare gap and improve the overall well-being of the nation. It is essential to address the practical challenges and potential criticisms associated with this strategy to ensure its successful implementation and long-term sustainability.

Kaiser Insurance Mental Health Coverage: What’s Included and Excluded?

You may want to see also

Explore related products

![]()

Encourage preventive care and wellness programs to lower long-term healthcare costs

Preventive care and wellness programs are essential strategies for reducing long-term healthcare costs in the USA. By focusing on early intervention and health maintenance, these programs can significantly decrease the incidence of chronic diseases, which are major drivers of healthcare expenses. For instance, regular screenings for conditions like diabetes, hypertension, and certain cancers can lead to early detection and treatment, thereby preventing more costly complications down the line.

One effective approach is to incentivize participation in preventive care programs through health insurance benefits. Insurers can offer reduced premiums or copays for individuals who engage in regular check-ups, exercise programs, smoking cessation classes, and other health-promoting activities. Additionally, employers can play a crucial role by providing wellness programs as part of their employee benefits packages, which can include on-site fitness classes, nutritional counseling, and stress management workshops.

Another key aspect is the integration of preventive care into primary care settings. Primary care physicians can act as gatekeepers, ensuring that patients receive appropriate preventive services based on their individual risk profiles. This can be facilitated through the use of electronic health records (EHRs) that prompt providers to recommend preventive measures during routine visits. Furthermore, telehealth services can expand access to preventive care, especially for individuals in underserved areas or those with mobility issues.

Education and awareness campaigns are also vital components of preventive care initiatives. Public health campaigns can inform the population about the importance of preventive measures and the resources available to them. This can include community outreach programs, social media campaigns, and partnerships with local organizations to disseminate information about healthy lifestyles and disease prevention.

In conclusion, encouraging preventive care and wellness programs is a multifaceted approach that involves collaboration between insurers, employers, healthcare providers, and public health entities. By investing in these programs, the USA can potentially see a significant reduction in long-term healthcare costs while also improving the overall health and well-being of its population.

Insurance Companies: Over-the-Counter vs. Prescribed Medication Rejection

You may want to see also

Explore related products

![]()

Streamline administrative processes and reduce regulatory burdens to decrease operational expenses

One effective strategy to reduce the cost of health insurance in the USA is to streamline administrative processes and alleviate regulatory burdens, which can significantly lower operational expenses for insurance providers. This approach involves simplifying the complex paperwork and bureaucratic procedures that currently dominate the healthcare system. By implementing more efficient administrative protocols, insurance companies can reduce the time and resources spent on processing claims, verifying eligibility, and complying with regulations. This, in turn, can lead to cost savings that can be passed on to policyholders in the form of lower premiums.

To achieve this goal, insurance providers can leverage technology to automate routine tasks, such as claims processing and data entry. This not only speeds up the process but also minimizes the risk of human error, which can lead to costly mistakes. Additionally, insurers can work with healthcare providers to standardize billing and coding practices, reducing the administrative burden on both parties. By simplifying the regulatory environment, insurers can also reduce the need for extensive compliance departments, further lowering operational costs.

Another key aspect of streamlining administrative processes is to improve communication and collaboration between different stakeholders in the healthcare system. This includes insurers, healthcare providers, and patients. By sharing information more effectively and working together to resolve issues, these stakeholders can reduce the need for duplicate testing, unnecessary procedures, and other costly inefficiencies. This collaborative approach can also help to identify and address areas where the system is failing, leading to more targeted and effective reforms.

In conclusion, streamlining administrative processes and reducing regulatory burdens is a critical step in making health insurance more affordable in the USA. By implementing more efficient protocols, leveraging technology, and fostering better communication and collaboration, insurance providers can significantly lower their operational expenses. These cost savings can then be passed on to policyholders, helping to make healthcare more accessible and affordable for all Americans.

Does Your Health Insurance Roll Over? Understanding Policy Renewal Basics

You may want to see also

Frequently asked questions

There are several strategies to lower health insurance costs, including:

- Increasing your deductible to reduce monthly premiums.

- Improving your credit score, as insurers often use it to help determine rates.

- Taking advantage of employer-sponsored health plans, which can be more affordable.

- Comparing plans and providers to find the most cost-effective option.

A high deductible health plan (HDHP) typically has lower monthly premiums compared to plans with lower deductibles. This is because you're agreeing to pay more out-of-pocket for healthcare services before your insurance coverage kicks in. HDHPs are often paired with health savings accounts (HSAs) to help manage the higher deductible costs.

Preventive care, such as regular check-ups, vaccinations, and screenings, can help reduce health insurance costs by:

- Detecting and treating health issues early, before they become more serious and expensive to treat.

- Reducing the likelihood of developing chronic conditions, which can lead to higher healthcare costs.

- Encouraging healthier lifestyle choices, which can lower overall healthcare expenses.

Yes, negotiating with healthcare providers can potentially help lower insurance costs. Here's how:

- You can discuss payment plans or discounts for upfront payments.

- You can ask about any available financial assistance programs.

- You can compare prices for procedures and services among different providers to find the most affordable option.

Remember, it's important to be proactive and communicate with your healthcare providers about your financial concerns.