Making health insurance affordable is a critical issue that affects millions of people worldwide. The rising costs of healthcare and insurance premiums have made it increasingly difficult for individuals and families to access the medical care they need. In this article, we will explore several strategies to help make health insurance more affordable, including understanding different types of insurance plans, maximizing tax credits and subsidies, and negotiating with healthcare providers. By following these tips, you can find a health insurance plan that fits your budget and provides the coverage you need to protect your health and well-being.

Explore related products

What You'll Learn

- Subsidies and Tax Credits: Explore government subsidies and tax credits to reduce premium costs for low-income individuals and families

- Preventive Care: Emphasize preventive care and wellness programs to lower overall healthcare costs and improve public health outcomes

- Market Competition: Encourage competition among insurance providers to drive down prices and offer more affordable plans to consumers

- Cost-Sharing Reductions: Implement cost-sharing reductions for deductibles, copayments, and coinsurance to make healthcare more accessible

- Administrative Cost Savings: Streamline administrative processes and reduce overhead costs to make insurance operations more efficient and cost-effective

![]()

Subsidies and Tax Credits: Explore government subsidies and tax credits to reduce premium costs for low-income individuals and families

One effective strategy to make health insurance more affordable is to leverage government subsidies and tax credits. These financial aids are designed to help low-income individuals and families reduce their premium costs, making health coverage more accessible. To start, it's essential to understand the types of subsidies available. For instance, the Affordable Care Act (ACA) offers premium tax credits to eligible individuals who purchase health insurance through the marketplace. These credits can significantly lower monthly premiums, and they are based on income and family size.

To qualify for these subsidies, individuals must meet specific criteria. Generally, they must have an income below a certain threshold, which varies by state and family size. Additionally, they must not be eligible for employer-sponsored health insurance or Medicaid. It's also important to note that these subsidies are only available for plans purchased through the health insurance marketplace, not for plans bought directly from an insurer.

Applying for subsidies involves filling out an application through the health insurance marketplace. This process typically requires providing proof of income and other documentation to verify eligibility. Once approved, the subsidy is applied directly to the monthly premium, reducing the amount the individual or family needs to pay out-of-pocket. It's crucial to reapply for subsidies each year, as eligibility can change based on income fluctuations and other factors.

Beyond premium tax credits, some states offer additional subsidies or assistance programs. These can include cost-sharing reductions, which help lower out-of-pocket costs like deductibles and copays, or state-specific programs that provide further financial aid. To explore these options, individuals should research their state's health insurance programs and contact local health departments or consumer assistance organizations for more information.

In conclusion, government subsidies and tax credits can play a vital role in making health insurance affordable for low-income individuals and families. By understanding the available options and the eligibility criteria, people can take advantage of these financial aids to reduce their premium costs and gain access to essential health coverage.

United Medical Resources: Insurance Coverage and Benefits Explained

You may want to see also

Explore related products

$14.99

![]()

Preventive Care: Emphasize preventive care and wellness programs to lower overall healthcare costs and improve public health outcomes

Preventive care and wellness programs are essential strategies in the quest to make health insurance more affordable. By focusing on early intervention and health maintenance, these programs can significantly reduce the financial burden on healthcare systems. For instance, regular health screenings and vaccinations can prevent the onset of chronic diseases, which are often costly to treat. Similarly, wellness initiatives that promote healthy lifestyles, such as smoking cessation programs and fitness challenges, can lead to a reduction in healthcare utilization and associated costs.

One effective approach to implementing preventive care is through employer-sponsored wellness programs. These programs can include biometric screenings, health risk assessments, and personalized health coaching. By identifying health risks early, individuals can take proactive steps to improve their health, thereby reducing the likelihood of developing costly medical conditions. Employers can also benefit from reduced absenteeism and increased productivity, making such programs a win-win for both parties.

Another key aspect of preventive care is the emphasis on chronic disease management. Conditions like diabetes, hypertension, and asthma can be effectively managed through regular monitoring, medication adherence, and lifestyle modifications. By providing resources and support for individuals with these conditions, healthcare systems can prevent costly hospitalizations and emergency room visits. For example, diabetes management programs that include regular blood sugar monitoring, dietary counseling, and medication management can significantly reduce the risk of complications and associated healthcare costs.

In addition to these strategies, preventive care also involves addressing social determinants of health, such as access to healthy food, safe housing, and clean water. By investing in community-based initiatives that address these factors, healthcare systems can improve overall public health outcomes and reduce disparities in healthcare access and affordability. For instance, programs that provide fresh produce to underserved communities or initiatives that improve housing conditions can have a profound impact on health outcomes and healthcare costs.

In conclusion, preventive care and wellness programs offer a promising solution to the challenge of making health insurance more affordable. By focusing on early intervention, chronic disease management, employer-sponsored initiatives, and addressing social determinants of health, these programs can lead to significant cost savings and improved public health outcomes. As such, they should be a central component of any comprehensive strategy to reform healthcare and make it more accessible and affordable for all.

Does Health Insurance Cover Chemotherapy? Understanding Your Coverage Options

You may want to see also

Explore related products

![]()

Market Competition: Encourage competition among insurance providers to drive down prices and offer more affordable plans to consumers

Insurance companies operate in a competitive market, and this competition can be leveraged to make health insurance more affordable for consumers. By encouraging more providers to enter the market and compete for customers, prices can be driven down, and more affordable plans can be offered. This can be achieved through a combination of regulatory changes, market reforms, and consumer education.

One way to encourage competition is to reduce barriers to entry for new insurance providers. This could include streamlining the licensing process, reducing capital requirements, and providing incentives for new companies to enter the market. Additionally, policymakers could consider implementing measures to increase transparency and accountability in the insurance industry, such as requiring companies to disclose their pricing and underwriting practices.

Another approach is to promote market reforms that encourage competition. This could include allowing insurance companies to sell plans across state lines, which would increase the number of providers available to consumers and create a more competitive market. Additionally, policymakers could consider implementing measures to reduce the administrative costs associated with insurance, such as simplifying billing and claims processes.

Consumer education is also an important component of encouraging competition in the insurance market. By educating consumers about their options and encouraging them to shop around for the best plan, they can put pressure on insurance companies to offer more affordable and competitive plans. This could include providing resources and tools to help consumers compare plans and prices, as well as educating them about the benefits and drawbacks of different types of insurance.

In conclusion, encouraging competition among insurance providers is a key strategy for making health insurance more affordable for consumers. By reducing barriers to entry, promoting market reforms, and educating consumers, policymakers can create a more competitive market that drives down prices and offers more affordable plans. This approach not only benefits consumers but also encourages innovation and improvement in the insurance industry as a whole.

Who is Assurance Insurance Company? A Comprehensive Overview and Guide

You may want to see also

Explore related products

![]()

Cost-Sharing Reductions: Implement cost-sharing reductions for deductibles, copayments, and coinsurance to make healthcare more accessible

Implementing cost-sharing reductions is a strategic approach to making healthcare more accessible and affordable. This involves lowering the out-of-pocket expenses that individuals must pay when receiving medical services, which can include deductibles, copayments, and coinsurance. By reducing these costs, more people can afford necessary treatments and preventive care, leading to better overall health outcomes and reduced financial strain on households.

One effective method to achieve cost-sharing reductions is through policy changes at the state or federal level. Legislators can pass laws that mandate lower cost-sharing requirements for insurance plans, or they can provide subsidies to help individuals afford their out-of-pocket expenses. For example, the Affordable Care Act (ACA) includes provisions for cost-sharing reductions for low-income individuals, which have been shown to improve access to care and reduce financial hardship.

Another approach is for employers to offer health insurance plans with lower cost-sharing requirements as part of their employee benefits packages. This can be an attractive option for workers and can help to improve employee satisfaction and retention. Additionally, some healthcare providers offer sliding scale fees or financial assistance programs to help patients afford their care, which can also contribute to cost-sharing reductions.

It is important to note that while cost-sharing reductions can make healthcare more accessible, they must be balanced with the need to maintain the financial sustainability of the healthcare system. If cost-sharing reductions are too drastic, they can lead to increased premiums or reduced coverage options, which can have negative consequences for the overall affordability of health insurance.

In conclusion, cost-sharing reductions are a valuable tool for making healthcare more affordable and accessible. By implementing these reductions through policy changes, employer-sponsored insurance plans, and healthcare provider initiatives, we can help to ensure that more people have access to the care they need without facing financial hardship.

NV Energy Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Administrative Cost Savings: Streamline administrative processes and reduce overhead costs to make insurance operations more efficient and cost-effective

One effective strategy to reduce administrative costs in health insurance operations is to implement automation technologies. By leveraging software solutions for tasks such as claims processing, billing, and customer service, insurers can significantly decrease the need for manual labor, thereby reducing overhead expenses. For instance, automated claims processing systems can quickly analyze and approve claims, minimizing the time and resources required for manual review.

Another approach to streamlining administrative processes is to adopt a paperless environment. Transitioning to digital documentation not only cuts down on physical storage costs but also enhances data accessibility and security. Insurers can utilize cloud-based storage solutions to securely store and manage policyholder information, claims data, and other critical documents. This shift to digital records also facilitates easier communication and collaboration among staff members, further improving operational efficiency.

Furthermore, insurers can explore outsourcing certain administrative functions to specialized service providers. By partnering with experts in areas such as claims management or IT support, insurers can tap into cost-effective solutions without compromising on quality. This strategic outsourcing allows insurers to focus on their core competencies while benefiting from the economies of scale and expertise offered by external providers.

In addition to these measures, insurers can optimize their organizational structure to eliminate redundancies and improve workflow. Conducting regular process audits can help identify inefficiencies and areas for improvement. By restructuring departments and redefining roles, insurers can create a more agile and responsive operational framework, better equipped to handle the demands of a dynamic healthcare market.

Lastly, investing in staff training and development can yield significant long-term benefits in terms of administrative cost savings. Equipping employees with the necessary skills and knowledge to perform their roles effectively can lead to increased productivity and reduced errors. Insurers can offer training programs focused on process optimization, technology adoption, and customer service excellence to enhance their workforce's capabilities and contribute to overall operational efficiency.

Nonprofit Employee Medical Insurance: What's the Deal?

You may want to see also

Frequently asked questions

There are several strategies to consider. First, shop around and compare rates from different providers. You might also look into increasing your deductible or switching to a Health Savings Account (HSA) plan. Additionally, maintaining a healthy lifestyle and taking advantage of employer-sponsored wellness programs can sometimes lead to discounts.

As a self-employed individual, you may want to explore options like joining a professional association that offers group health insurance rates. You could also consider a Health Reimbursement Arrangement (HRA) or a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) to help cover medical expenses.

Yes, there are government programs available to assist with health insurance costs. Medicaid and the Children's Health Insurance Program (CHIP) provide coverage for eligible low-income individuals and families. Additionally, you may qualify for subsidies through the Affordable Care Act (ACA) marketplace.

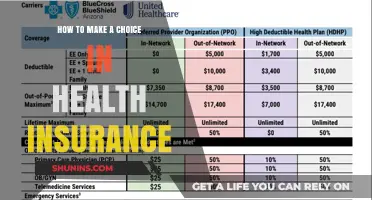

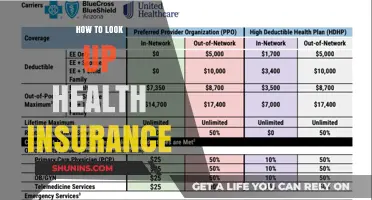

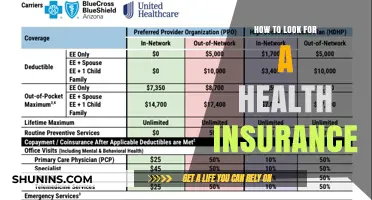

When selecting a health insurance plan, consider factors such as the premium cost, deductible amount, copayments, and coinsurance rates. It's also important to evaluate the plan's network of providers and prescription drug coverage. Choosing a plan with a lower premium might mean higher out-of-pocket costs, so balance your needs and budget carefully.

To reduce out-of-pocket expenses, consider using generic medications instead of brand-name drugs. You can also look into telemedicine options for non-emergency care, which may have lower copays. Additionally, make sure to use in-network providers whenever possible and review your plan's benefits to understand what services are covered and what your responsibilities are.