Choosing the right health insurance plan can be a daunting task, but it's essential for ensuring you have the coverage you need. With so many options available, it's important to understand the key factors to consider when making your decision. In this guide, we'll walk you through the process of selecting a health insurance plan that meets your needs and budget. We'll cover everything from understanding your coverage options to comparing plans and enrolling in the one that's right for you. By the end of this guide, you'll have the confidence and knowledge to make an informed choice about your health insurance.

Explore related products

What You'll Learn

- Assess Your Needs: Consider your health status, age, and any pre-existing conditions that may affect your coverage options

- Understand Plan Types: Familiarize yourself with different plan types such as HMO, PPO, EPO, and POS to choose the best fit

- Compare Costs: Evaluate premiums, deductibles, copays, and coinsurance to determine the most cost-effective plan for your budget

- Check Provider Networks: Ensure your preferred doctors and hospitals are included in the plan's network to avoid unexpected out-of-pocket expenses

- Read Reviews and Ratings: Research customer satisfaction and ratings of insurance providers to gauge the quality of service and support

![]()

Assess Your Needs: Consider your health status, age, and any pre-existing conditions that may affect your coverage options

To make an informed decision about health insurance, it's crucial to begin by assessing your individual needs. This involves taking a close look at your current health status, age, and any pre-existing conditions that could impact your coverage options. Start by making a list of your regular healthcare needs, such as prescription medications, ongoing treatments, or chronic conditions that require regular monitoring. This will help you identify which types of coverage are essential for you.

Next, consider your age and how it might affect your insurance premiums and coverage. Younger individuals may opt for more affordable plans with higher deductibles, while older adults may prefer plans with more comprehensive coverage, even if they come with higher premiums. Additionally, think about any pre-existing conditions you have, as these can significantly influence your insurance options. Some plans may exclude coverage for pre-existing conditions, while others may offer limited coverage or require higher premiums.

It's also important to consider your lifestyle and habits when assessing your health insurance needs. For example, if you're an avid traveler, you may want to look for plans that offer international coverage. Similarly, if you're planning to start a family, you'll want to ensure that your insurance covers maternity and newborn care. By taking the time to evaluate your unique needs and circumstances, you can narrow down your options and find a health insurance plan that provides the right level of coverage for you.

When assessing your needs, it's helpful to consult with a healthcare professional or an insurance advisor who can provide personalized guidance based on your specific situation. They can help you understand the intricacies of different insurance plans and how they might impact your healthcare costs. Additionally, consider using online tools and resources to compare different plans and get a sense of their coverage and costs. By doing your research and seeking expert advice, you can make a more informed decision about your health insurance.

Remember, your health insurance needs may change over time, so it's important to reassess your coverage periodically. Life events such as marriage, divorce, or a change in employment status can all impact your insurance needs. By staying informed and proactive, you can ensure that you have the right level of coverage to protect your health and financial well-being.

Last-Minute Insurance: What to Do If You Missed the Deadline

You may want to see also

Explore related products

![]()

Understand Plan Types: Familiarize yourself with different plan types such as HMO, PPO, EPO, and POS to choose the best fit

Understanding the different types of health insurance plans is crucial for making an informed decision about your coverage. Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), and Point of Service (POS) plans each have unique characteristics that cater to different needs and preferences.

HMOs typically require you to choose a primary care physician (PCP) and use a network of approved providers. They often have lower premiums and out-of-pocket costs but may limit your flexibility in choosing healthcare providers outside the network. PPOs, on the other hand, offer more flexibility by allowing you to visit any healthcare provider, but you may pay higher premiums and out-of-pocket costs for out-of-network care.

EPOs are similar to HMOs in that they require you to use a network of approved providers, but they do not usually require you to choose a PCP. They often have lower premiums than PPOs but may have higher out-of-pocket costs for out-of-network care. POS plans combine elements of HMOs and PPOs, allowing you to choose a PCP and use a network of approved providers, but also giving you the option to seek care outside the network at a higher cost.

When choosing a plan, consider factors such as your budget, your healthcare needs, and your preference for provider flexibility. It's also important to review the plan's coverage details, including deductibles, copayments, and coinsurance, to ensure that it meets your specific requirements. By understanding the differences between these plan types, you can make a more informed decision about which one is the best fit for you.

Is Not Changing Your Address Health Insurance Fraud?

You may want to see also

Explore related products

$9.95 $9.95

![]()

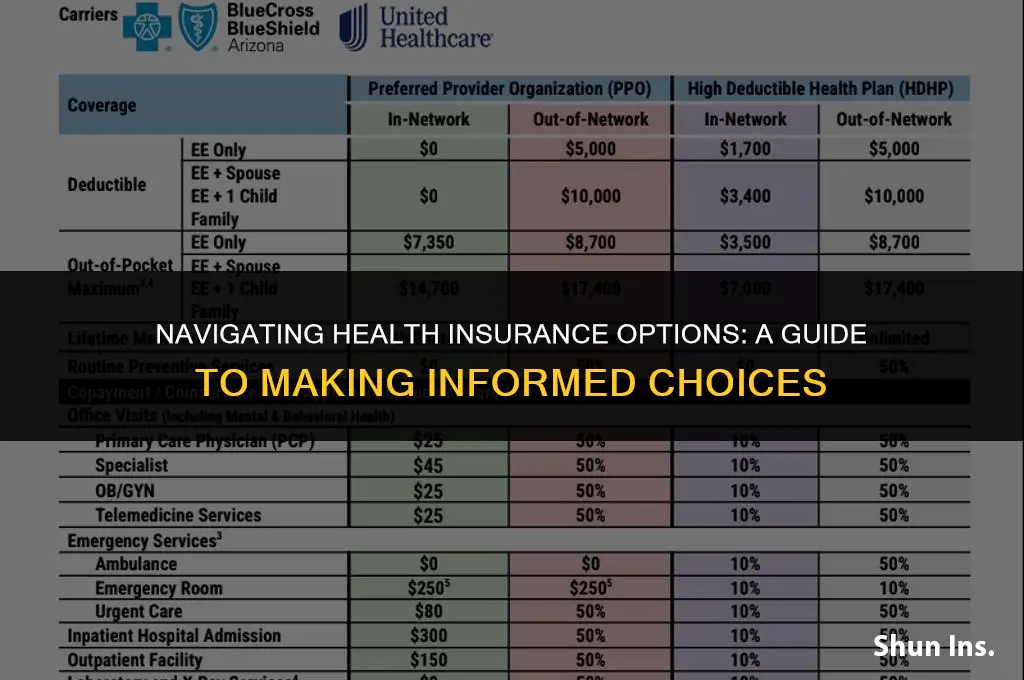

Compare Costs: Evaluate premiums, deductibles, copays, and coinsurance to determine the most cost-effective plan for your budget

To effectively compare the costs of different health insurance plans, it's crucial to go beyond just looking at the monthly premiums. While premiums are a significant factor, they don't tell the whole story. You also need to consider the deductible, which is the amount you'll have to pay out of pocket before your insurance coverage kicks in. Plans with lower premiums often have higher deductibles, which can lead to higher overall costs if you require frequent medical care.

Another important aspect to consider is the copay, which is a fixed amount you'll pay for each doctor's visit or prescription. Some plans may have lower copays for in-network providers but higher copays for out-of-network care. Additionally, coinsurance, which is the percentage of medical costs you'll pay after meeting your deductible, can vary significantly between plans. A plan with a lower premium might have a higher coinsurance rate, which could result in higher out-of-pocket expenses.

When evaluating the cost-effectiveness of a plan, it's essential to consider your individual health needs and budget. If you're generally healthy and don't anticipate needing a lot of medical care, a plan with a lower premium and higher deductible might be more cost-effective. However, if you have chronic health conditions or expect to need frequent medical attention, a plan with a higher premium but lower deductible and copays might be a better choice.

To make an informed decision, it's helpful to create a spreadsheet or use an online calculator to compare the costs of different plans based on your expected healthcare needs. This will allow you to see which plan is the most cost-effective for your specific situation. Additionally, it's important to consider the plan's network of providers and whether your preferred doctors and hospitals are included. While a plan might be more cost-effective, it may not be worth it if it doesn't provide access to the care you need.

In conclusion, comparing the costs of health insurance plans requires a careful analysis of premiums, deductibles, copays, and coinsurance. By considering your individual health needs and budget, and using tools to compare the costs of different plans, you can make an informed decision that will help you save money and get the care you need.

Applying Third-Party Insurance to Your Flight Bookings

You may want to see also

Explore related products

![]()

Check Provider Networks: Ensure your preferred doctors and hospitals are included in the plan's network to avoid unexpected out-of-pocket expenses

Before selecting a health insurance plan, it's crucial to verify that your preferred healthcare providers are part of the plan's network. This due diligence can prevent unexpected out-of-pocket expenses that may arise from visiting out-of-network doctors or hospitals. To begin, make a list of your primary care physician, specialists, and any hospitals you frequently visit or would prefer to use in case of emergencies.

Next, obtain a list of in-network providers from the insurance company you're considering. This list is typically available on the insurer's website or can be requested directly. Compare your list of preferred providers with the insurer's network list to ensure there's a match. If your preferred providers are not included, you may need to consider alternative plans or be prepared to pay additional costs for out-of-network care.

It's also important to understand the different types of provider networks. Exclusive Provider Organizations (EPOs) and Health Maintenance Organizations (HMOs) generally require you to use in-network providers, except in emergencies. Preferred Provider Organizations (PPOs) offer more flexibility, allowing you to use out-of-network providers at a higher cost. Knowing the type of network can help you make an informed decision based on your healthcare needs and preferences.

Additionally, consider the potential for changes in the provider network. Insurance companies periodically update their networks, which could result in your preferred provider being dropped. To mitigate this risk, choose a plan with a stable network history or one that offers a broader range of in-network providers.

Finally, don't overlook the importance of checking the network's geographic coverage. If you travel frequently or live in a border state, ensure that the plan's network includes providers in the areas you visit most often. This can provide peace of mind and ensure continuity of care, even when you're away from home.

Travel Insurance: Medical Records and Their Importance

You may want to see also

Explore related products

![]()

Read Reviews and Ratings: Research customer satisfaction and ratings of insurance providers to gauge the quality of service and support

Researching customer satisfaction and ratings of insurance providers is a crucial step in making an informed choice about health insurance. This process allows you to gauge the quality of service and support you can expect from a provider, which is just as important as the coverage options and costs. Start by visiting reputable review websites and consumer advocacy groups that specialize in health insurance. Look for recent reviews and pay attention to trends in customer feedback. Are there consistent complaints about billing issues, denied claims, or poor customer service? Or do you see a pattern of positive experiences and high satisfaction rates?

Next, check the ratings assigned by independent rating agencies such as A.M. Best, Moody’s, and Standard & Poor’s. These agencies evaluate insurance companies based on their financial stability, ability to pay claims, and overall performance. A high rating from these agencies can give you confidence in a provider’s reliability and long-term viability. Additionally, consider reaching out to friends, family, and colleagues for their personal recommendations and experiences with different insurance providers.

When evaluating reviews and ratings, it’s important to consider the context and specifics of each situation. For example, a single negative review about a denied claim may not necessarily indicate a systemic problem with the provider, especially if the reviewer failed to meet the policy’s requirements. Similarly, a high overall rating may not guarantee that you will have a perfect experience, as individual circumstances can vary greatly. Look for patterns and consistency in the feedback, and pay attention to how the provider responds to both positive and negative reviews.

In addition to customer satisfaction and ratings, it’s also important to research the provider’s history of regulatory compliance and any major legal issues they may have faced. This information can give you insight into the company’s ethical practices and commitment to upholding industry standards. You can find this information through online searches, state insurance department websites, and consumer advocacy groups.

Finally, as you gather information from reviews and ratings, keep in mind that your own needs and preferences are unique. What may be a deal-breaker for one person may not be as important to you. Consider the factors that matter most to you in a health insurance provider, such as the quality of customer service, the ease of navigating the claims process, or the availability of specific coverage options. By weighing these factors against the reviews and ratings you’ve researched, you can make a more informed and confident decision about which health insurance provider is right for you.

Are Retiree Health Insurance Benefits Taxable? What You Need to Know

You may want to see also

Frequently asked questions

When selecting a health insurance plan, consider factors such as your budget, the level of coverage you need, the type of healthcare providers you prefer, and any specific health conditions you may have. Additionally, think about the plan's deductible, copayments, coinsurance, and out-of-pocket maximums to ensure it aligns with your financial situation and healthcare needs.

A PPO (Preferred Provider Organization) plan allows you to visit any healthcare provider within the network without needing a referral from a primary care physician. However, you may pay more for out-of-network care. On the other hand, an HMO (Health Maintenance Organization) plan typically requires you to choose a primary care physician and get referrals for specialist care. HMOs often have lower premiums and out-of-pocket costs but may limit your provider choices.

A high deductible health plan (HDHP) requires you to pay a higher deductible before your insurance coverage kicks in. The advantage of an HDHP is that it usually comes with lower monthly premiums, making it more affordable for individuals who don't anticipate frequent medical expenses. However, the disadvantage is that you'll need to cover a larger portion of your healthcare costs out-of-pocket before your insurance benefits apply, which can be challenging if you face unexpected medical bills.

The open enrollment period is a specific timeframe during which you can enroll in, switch, or update your health insurance plan. This period is crucial because it's the only time you can make changes to your coverage without experiencing a qualifying life event, such as marriage, divorce, or job loss. Missing the open enrollment period may result in being locked into your current plan for the remainder of the year, so it's essential to stay informed about the dates and make any necessary adjustments during this time.