Looking for health insurance can be a daunting task, but it's an essential part of maintaining your health and financial well-being. With so many options available, it's important to understand the basics of health insurance and how to find a plan that meets your needs. In this guide, we'll walk you through the process of selecting health insurance, from understanding the different types of plans to comparing costs and benefits. We'll also provide tips on how to navigate the complex world of health insurance terminology and make informed decisions about your coverage. Whether you're new to health insurance or looking to switch plans, this guide will help you find the right coverage for you and your family.

Explore related products

What You'll Learn

- Assess Your Needs: Determine your health care requirements and those of your dependents. Consider age, health status, and any pre-existing conditions

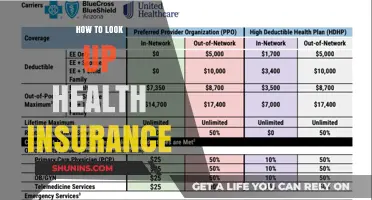

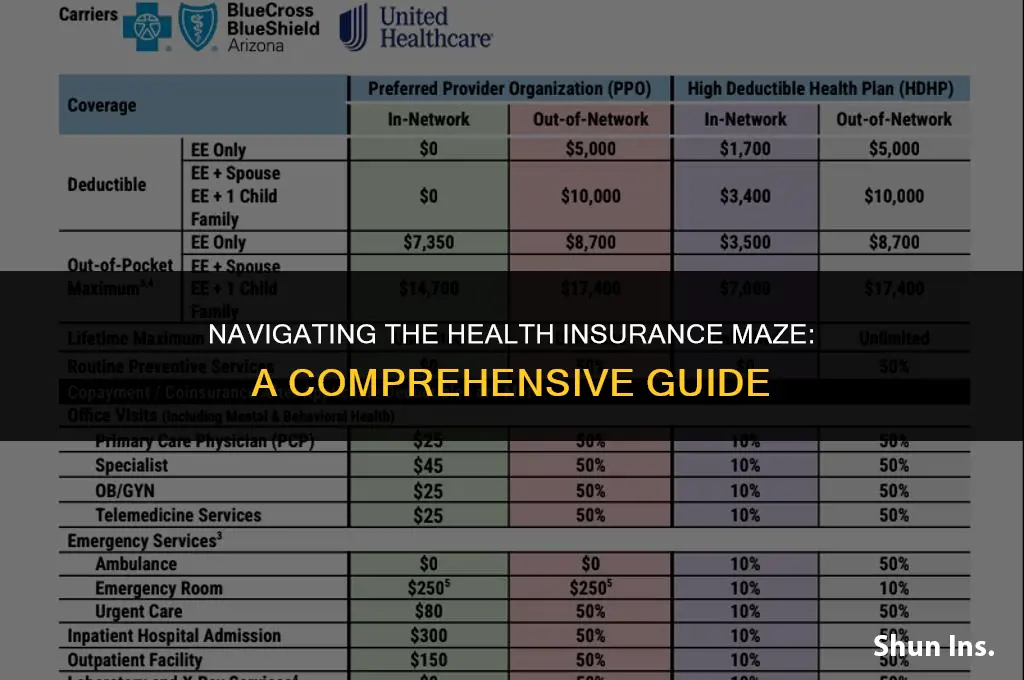

- Understand Insurance Types: Familiarize yourself with different types of health insurance plans, such as HMO, PPO, EPO, and POS. Each has its own benefits and limitations

- Compare Costs: Evaluate the premiums, deductibles, copays, and coinsurance associated with each plan. Consider both immediate and long-term costs

- Check Provider Networks: Ensure your preferred doctors, hospitals, and specialists are included in the plan's network. Out-of-network care can be significantly more expensive

- Read Reviews and Ratings: Research the insurance company's reputation, customer service quality, and claims processing efficiency. Look for reviews from current and former policyholders

![]()

Assess Your Needs: Determine your health care requirements and those of your dependents. Consider age, health status, and any pre-existing conditions

To effectively assess your health care needs and those of your dependents, begin by gathering comprehensive information about each individual's health status. This includes documenting any pre-existing conditions, current medications, and recent medical treatments or hospitalizations. For children, consider their developmental stage and any specific health concerns related to their age group. Older adults may require additional considerations such as mobility issues, chronic conditions, and potential long-term care needs.

Next, evaluate the frequency and type of medical services each person typically requires. This could range from routine check-ups and preventive care to more specialized treatments for chronic conditions. Consider the potential costs associated with these services, including out-of-pocket expenses, copays, and deductibles. This information will help you determine the level of coverage needed and the most cost-effective insurance options.

It's also important to think about future health care needs. For example, if you or a dependent has a condition that is likely to worsen over time, you may need to consider insurance plans that offer more extensive coverage for ongoing treatments. Additionally, if you plan to have more children, factor in the costs associated with pregnancy, childbirth, and pediatric care.

When assessing your needs, don't overlook the importance of mental health care. Many insurance plans now include coverage for mental health services, and it's crucial to consider these needs alongside physical health requirements. This could include therapy sessions, psychiatric evaluations, and medication management for conditions such as depression, anxiety, or ADHD.

Finally, consider the overall health and wellness goals of your family. If you prioritize preventive care and wellness programs, look for insurance plans that offer incentives or coverage for activities such as gym memberships, nutrition counseling, or smoking cessation programs. By taking a holistic approach to assessing your health care needs, you can identify the most suitable insurance options that will provide comprehensive coverage and support for your family's well-being.

Evaluating Gap Health Insurance: Is It Worth the Investment?

You may want to see also

Explore related products

![]()

Understand Insurance Types: Familiarize yourself with different types of health insurance plans, such as HMO, PPO, EPO, and POS. Each has its own benefits and limitations

Understanding the different types of health insurance plans is crucial when looking for coverage that suits your needs. Health Maintenance Organizations (HMOs) are one of the most common types of plans. They typically require you to choose a primary care physician and use a network of approved providers. HMOs often have lower premiums and out-of-pocket costs but may limit your flexibility in choosing healthcare providers outside the network.

Preferred Provider Organizations (PPOs) offer more flexibility than HMOs. They allow you to visit any healthcare provider within their network without needing a referral from a primary care physician. PPOs also cover some out-of-network care, although at a higher cost. This type of plan is ideal for those who want more control over their healthcare choices and are willing to pay a bit more for that freedom.

Exclusive Provider Organizations (EPOs) are similar to HMOs in that they require you to use a network of approved providers. However, they do not require you to choose a primary care physician or obtain referrals for specialist care. EPOs often have lower premiums than PPOs but may have higher out-of-pocket costs if you need to see a provider outside the network.

Point of Service (POS) plans are a hybrid between HMOs and PPOs. They require you to choose a primary care physician and obtain referrals for specialist care, similar to an HMO. However, they also allow you to visit providers outside the network, like a PPO, although at a higher cost. POS plans can be a good option for those who want the lower costs of an HMO but also need some flexibility in their healthcare choices.

When choosing a health insurance plan, it's important to consider your healthcare needs, budget, and preferences. Each type of plan has its own benefits and limitations, so it's essential to compare them carefully to find the one that best fits your situation.

The Risks and Consequences of Living Without Health Insurance

You may want to see also

Explore related products

![]()

Compare Costs: Evaluate the premiums, deductibles, copays, and coinsurance associated with each plan. Consider both immediate and long-term costs

To effectively compare the costs of different health insurance plans, it's crucial to look beyond just the monthly premiums. While premiums are a significant factor, they don't tell the whole story. Deductibles, copays, and coinsurance are also essential components that can greatly impact your overall expenses. A plan with a lower premium might have higher out-of-pocket costs, making it less cost-effective in the long run. Conversely, a plan with a higher premium might offer more comprehensive coverage, potentially saving you money on healthcare costs over time.

When evaluating deductibles, consider how much you're willing and able to pay out of pocket before your insurance coverage kicks in. If you anticipate needing frequent medical care or have a chronic condition, a plan with a lower deductible might be more suitable. On the other hand, if you're generally healthy and don't expect to need much medical attention, a plan with a higher deductible could be a more affordable option.

Copays and coinsurance are also important to consider. Copays are fixed amounts you pay for certain services, such as doctor visits or prescription medications, while coinsurance is a percentage of the cost you're responsible for after meeting your deductible. Plans with lower copays and coinsurance can be more beneficial if you require regular medical care or have high healthcare costs.

In addition to immediate costs, it's essential to consider long-term expenses. Some plans may have lower premiums but higher maximum out-of-pocket costs, which could lead to financial strain in the event of a major medical emergency. Other plans may have higher premiums but offer more comprehensive coverage, potentially saving you money in the long run.

To make an informed decision, use online tools or consult with an insurance agent to compare the costs of different plans side by side. Take into account your expected healthcare needs, budget, and risk tolerance when evaluating the various cost components. By carefully considering both immediate and long-term costs, you can choose a health insurance plan that provides the best value for your money.

Top Health Insurance Providers in Kenya: A Comprehensive Comparison Guide

You may want to see also

Explore related products

![]()

Check Provider Networks: Ensure your preferred doctors, hospitals, and specialists are included in the plan's network. Out-of-network care can be significantly more expensive

When selecting a health insurance plan, one of the most critical factors to consider is the provider network. This refers to the list of doctors, hospitals, and specialists that are contracted with the insurance company to provide services at a negotiated rate. Ensuring that your preferred healthcare providers are included in this network is essential to avoid unexpected costs and complications.

Out-of-network care, which involves receiving treatment from providers not listed in the plan's network, can be significantly more expensive. This is because these providers have not agreed to the same rate structures as in-network providers, and the insurance company may not cover the full cost of the services rendered. In some cases, the patient may be responsible for paying the entire bill out-of-pocket, or the insurance company may only cover a portion of the costs, leaving the patient with a substantial financial burden.

To avoid these issues, it's crucial to carefully review the provider network of any health insurance plan you're considering. This can typically be done by visiting the insurance company's website or contacting their customer service department. They should be able to provide you with a comprehensive list of in-network providers, which you can then cross-reference with your own healthcare needs and preferences.

If you have specific medical conditions or require specialized care, it's especially important to ensure that the providers you need are included in the network. This may involve researching the credentials and expertise of individual doctors, as well as the facilities and services offered by hospitals and clinics. By taking the time to do this research upfront, you can help ensure that you have access to the care you need without facing unexpected financial challenges.

In addition to checking the provider network, it's also a good idea to consider the overall quality of the insurance plan. This may involve looking at factors such as the plan's premiums, deductibles, copays, and coinsurance rates, as well as any additional benefits or features that may be included. By carefully evaluating all of these factors, you can make an informed decision about which health insurance plan is right for you and your family.

Choosing the Right Medical Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Read Reviews and Ratings: Research the insurance company's reputation, customer service quality, and claims processing efficiency. Look for reviews from current and former policyholders

Researching an insurance company's reputation is crucial when selecting a health insurance provider. Start by checking online review platforms such as Yelp, Google Reviews, and the Better Business Bureau (BBB) to get an overview of customer experiences. Pay attention to both positive and negative reviews, noting common themes and specific incidents that may indicate the company's strengths and weaknesses. Look for reviews that mention the company's customer service quality, claims processing efficiency, and overall satisfaction.

In addition to online reviews, consider reaching out to friends, family, and colleagues who may have experience with the insurance company you're considering. Personal recommendations can provide valuable insights and help you gauge the company's reliability and trustworthiness. You can also check with your state's insurance department for any complaints or regulatory actions against the company.

When evaluating an insurance company's reputation, it's important to consider the context of the reviews and ratings. For example, a single negative review may not necessarily indicate a poor company, but a pattern of complaints about the same issue could be a red flag. Similarly, a high overall rating may not guarantee a perfect experience, but it can suggest that the company generally meets its customers' needs.

Another aspect to consider is the company's financial stability. A financially strong company is more likely to be able to pay claims and provide reliable service. You can check the company's financial ratings through agencies such as A.M. Best, Moody's, and Standard & Poor's.

Finally, don't forget to consider the company's claims processing efficiency. A company that processes claims quickly and accurately can make a significant difference in your overall experience, especially when you're dealing with medical emergencies or unexpected health issues. Look for reviews that mention the company's claims processing time and accuracy, and consider reaching out to the company directly to ask about their claims processing procedures.

Why Insurance Companies Play Doctor: Unraveling Medical Decision-Making Power

You may want to see also

Frequently asked questions

When searching for health insurance, consider factors such as coverage options, premium costs, deductibles, co-pays, network providers, prescription drug coverage, and customer reviews.

To determine the right health insurance plan, assess your healthcare needs, budget, and preferences. Compare plans based on coverage, costs, and provider networks to find the best fit.

HMO (Health Maintenance Organization) plans require you to use in-network providers and often need referrals for specialists. PPO (Preferred Provider Organization) plans offer more flexibility to use out-of-network providers but at a higher cost. EPO (Exclusive Provider Organization) plans are similar to HMOs but do not require referrals for specialists.

To save money on health insurance premiums, consider choosing a plan with a higher deductible, opting for a Health Savings Account (HSA) or Flexible Spending Account (FSA), bundling health insurance with other policies, and maintaining a healthy lifestyle to qualify for discounts.

The open enrollment period for health insurance is the time when individuals can enroll in, switch, or renew their health insurance plans. This period is important because it allows you to make changes to your coverage without facing penalties or being denied due to pre-existing conditions.