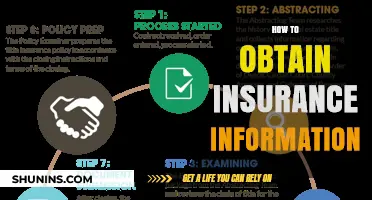

Obtaining insurance for contractors is a critical step in safeguarding both the business and its clients from potential risks and liabilities. Contractors, whether in construction, consulting, or other industries, face unique challenges such as property damage, bodily injury, and professional errors, making tailored insurance coverage essential. To secure the right policy, contractors should first assess their specific needs, considering factors like the scope of work, project size, and regulatory requirements. Next, they should research insurance providers that specialize in contractor policies, comparing coverage options, premiums, and deductibles. Consulting with an insurance broker or agent can also provide valuable insights and help navigate complex policy terms. Finally, contractors should ensure compliance with state and industry regulations, as some jurisdictions mandate certain types of insurance. By taking these steps, contractors can protect their livelihoods, build trust with clients, and operate with confidence in an often unpredictable business environment.

Explore related products

What You'll Learn

- Types of Contractor Insurance: Liability, workers' comp, property, and professional indemnity coverage options

- Assessing Coverage Needs: Evaluate project risks, contract requirements, and legal obligations for adequate protection

- Finding Reliable Providers: Research insurers, compare quotes, and check reviews for trusted contractor policies

- Application Process: Gather business details, claims history, and safety records to complete insurance applications

- Cost Management: Bundle policies, improve safety practices, and adjust deductibles to reduce insurance premiums

![]()

Types of Contractor Insurance: Liability, workers' comp, property, and professional indemnity coverage options

Contractors face unique risks on the job, from property damage to bodily injury claims. Liability insurance is the cornerstone of any contractor’s policy, protecting against third-party claims for accidents or damage caused by your work. For instance, if a client trips over your equipment and sues for medical expenses, this coverage steps in. Most policies start at $1 million per occurrence, but high-risk trades like roofing or electrical work may require higher limits. When shopping, compare general liability policies for exclusions—some omit coverage for specific tools or completed operations. Pro tip: Bundle liability with other coverages for a multi-policy discount, often saving 10-15% on premiums.

Workers’ compensation insurance is legally required in most states if you have employees, but even solo contractors should consider it. This coverage pays for medical bills and lost wages if a worker is injured on the job. For example, a carpenter who falls from a ladder could face months of recovery and thousands in medical costs. Without workers’ comp, the contractor could be personally liable. Premiums vary by payroll size and job risk—a roofing company pays more than a painter. Audit your payroll annually to avoid overpaying, and implement safety programs to reduce claims and lower rates over time.

Property insurance safeguards your tools, equipment, and materials from theft, fire, or damage. Imagine a plumber’s van broken into, with $10,000 worth of tools stolen—without coverage, this loss could cripple their business. Policies typically cover replacement costs, but verify if your insurer uses actual cash value (ACV) instead, which factors in depreciation. Contractors with expensive equipment should consider inland marine insurance, a specialized policy for tools in transit or at job sites. Inventory your equipment annually and update your policy limits to reflect current values.

Professional indemnity insurance, also known as errors and omissions (E&O) coverage, is critical for contractors offering design or consulting services. If a client sues for financial losses due to your advice or work, this policy covers legal fees and settlements. For example, a general contractor who misinterprets blueprints could face a six-figure claim. Premiums depend on your revenue and claim history, with deductibles ranging from $1,000 to $5,000. To reduce costs, document all client communications and contracts thoroughly—clear records can prevent claims from escalating.

Each type of insurance serves a distinct purpose, but they overlap in protecting your business from financial ruin. Liability shields you from third-party claims, workers’ comp covers employee injuries, property safeguards your assets, and professional indemnity defends against service-related lawsuits. Assess your risks annually—a growing team or new service offerings may require additional coverage. Work with an independent agent who specializes in contractor policies to tailor a plan to your needs. Remember, the cheapest policy isn’t always the best; focus on adequate limits and comprehensive coverage to ensure long-term stability.

Do I Need Texas Insurance? Understanding State Requirements and Coverage

You may want to see also

Explore related products

![]()

Assessing Coverage Needs: Evaluate project risks, contract requirements, and legal obligations for adequate protection

Contractors face a unique set of risks that demand tailored insurance solutions. Before securing a policy, a thorough assessment of coverage needs is essential to ensure adequate protection. This process involves a meticulous evaluation of project risks, contract requirements, and legal obligations. Each of these factors plays a critical role in determining the type and extent of insurance necessary to safeguard against potential liabilities.

Project Risks: Identifying Potential Pitfalls

Every project carries inherent risks that can vary widely depending on scope, location, and complexity. For instance, a high-rise construction project in an urban area may face risks like property damage from heavy machinery, while a residential renovation in a suburban setting might involve risks related to worker injury or material defects. Contractors must conduct a risk assessment to identify these potential pitfalls. Tools such as a risk register or SWOT analysis can help categorize risks into financial, operational, and legal domains. For example, a contractor working on a waterfront project should consider flood insurance, while one handling hazardous materials might need pollution liability coverage. Understanding these risks is the first step in tailoring an insurance policy that provides comprehensive protection.

Contract Requirements: Decoding the Fine Print

Contracts often dictate specific insurance requirements that contractors must meet to comply with the terms of the agreement. These requirements can include minimum liability limits, additional insured status for clients or project owners, and waivers of subrogation. For example, a commercial construction contract might mandate $2 million in general liability coverage and $1 million in workers’ compensation insurance. Failure to meet these requirements can result in contract termination or financial penalties. Contractors should carefully review all contracts and consult with legal or insurance professionals to ensure compliance. Additionally, maintaining open communication with clients about insurance needs can prevent misunderstandings and foster trust.

Legal Obligations: Navigating Regulatory Landscapes

Beyond contractual obligations, contractors must adhere to state and federal regulations that mandate certain types of insurance. For instance, most states require workers’ compensation insurance for businesses with employees, regardless of project size. Similarly, commercial auto insurance is mandatory for contractors using vehicles for work-related purposes. Non-compliance with these regulations can lead to fines, legal action, or even business closure. Contractors should stay informed about local laws and consult with an insurance broker to ensure all legal requirements are met. In some cases, industry-specific regulations may apply, such as environmental liability coverage for contractors working on government projects.

Practical Tips for Adequate Protection

To streamline the assessment process, contractors can follow a few practical steps. First, create a checklist of all potential risks, contract clauses, and legal mandates. Second, consult with an insurance broker who specializes in contractor policies to identify gaps in coverage. Third, consider bundling policies, such as a Business Owners Policy (BOP), to save costs while maintaining comprehensive protection. Finally, regularly review and update insurance coverage as projects evolve or regulations change. For example, a contractor expanding into a new state should verify whether their current policies meet local requirements.

By systematically evaluating project risks, contract requirements, and legal obligations, contractors can secure insurance that provides robust protection against unforeseen challenges. This proactive approach not only mitigates financial losses but also enhances credibility and competitiveness in the marketplace.

Life Insurance Rates: Recession Impact and You

You may want to see also

Explore related products

![]()

Finding Reliable Providers: Research insurers, compare quotes, and check reviews for trusted contractor policies

Securing reliable insurance is a cornerstone of any contractor's risk management strategy, but not all providers are created equal. The first step in finding a trustworthy insurer is to research insurers who specialize in contractor policies. General insurers may offer coverage, but specialists often have a deeper understanding of the unique risks contractors face, such as property damage, bodily injury, or project delays. Start by identifying insurers with a proven track record in the construction industry, leveraging industry associations, trade publications, and online directories like the National Association of Surety Bond Producers (NASBP) or the Independent Insurance Agents & Brokers of America (IIABA). These resources can provide a curated list of providers who understand the nuances of contractor insurance.

Once you’ve compiled a list of potential insurers, the next critical step is to compare quotes meticulously. Quotes can vary widely based on coverage limits, deductibles, and policy exclusions. For instance, a policy with a $1 million general liability limit might cost 20-30% more than one with a $500,000 limit, but the added protection could be invaluable for larger projects. Pay close attention to policy details like whether the coverage is occurrence-based (covers claims made for incidents during the policy period) or claims-made (covers claims filed during the policy period, regardless of when the incident occurred). Use comparison tools like Insureon or Simply Business to streamline this process, ensuring you’re not sacrificing essential coverage for a lower premium.

While quotes provide a quantitative basis for comparison, checking reviews offers qualitative insights into an insurer’s reliability. Scour platforms like Trustpilot, Google Reviews, and the Better Business Bureau (BBB) to gauge customer satisfaction, claims handling efficiency, and overall service quality. Look for patterns in reviews—consistent complaints about delayed payouts or poor customer service should raise red flags. Conversely, insurers with high ratings and positive testimonials about their responsiveness and transparency are worth prioritizing. Additionally, consult industry forums and peer networks for firsthand accounts from other contractors, as these can provide unfiltered perspectives on an insurer’s performance.

A practical tip for contractors is to request references directly from insurers. Reputable providers should be willing to share case studies or testimonials from clients in similar industries or with comparable project scopes. This step can help validate their expertise and reliability. Finally, consider working with an independent insurance broker who can act as your advocate, leveraging their market knowledge to negotiate better terms and ensure you’re getting the most value for your investment. By combining thorough research, careful quote comparisons, and diligent review-checking, contractors can secure policies that not only meet regulatory requirements but also provide robust protection for their business.

Does the Department of Insurance Search Your SSN? Facts Revealed

You may want to see also

Explore related products

![]()

Application Process: Gather business details, claims history, and safety records to complete insurance applications

Contractors seeking insurance must prepare a comprehensive application that reflects their business operations, risk management practices, and historical performance. Insurers rely on detailed information to assess liability and tailor coverage, making accuracy and completeness critical. Begin by compiling essential business details: legal structure, years in operation, revenue figures, and employee count. Include a breakdown of services offered, such as residential remodeling or commercial construction, as these influence risk profiles. For instance, a contractor specializing in high-rise projects may face different exposures than one focused on landscaping. Organize this data in a clear, concise format to streamline the application process and avoid delays.

Claims history is another cornerstone of the application, offering insurers insight into past incidents and potential future risks. Gather records of all claims filed within the past 5–10 years, including dates, descriptions, and settlement amounts. Be transparent about unresolved cases or recurring issues, as omissions can lead to policy denial or cancellation. If your business has a clean claims record, highlight this as evidence of strong risk management. Conversely, if claims exist, provide context—such as steps taken to prevent recurrence—to demonstrate proactive mitigation. Insurers value honesty and improvement over concealment.

Safety records play a pivotal role in underwriting, as they directly correlate with risk levels. Compile documentation such as OSHA logs, safety training certificates, and incident reports. If your business has a formal safety program, include details on its structure, frequency of training, and enforcement policies. For example, a contractor with monthly safety meetings and a zero-tolerance policy for violations may qualify for lower premiums. Even small-scale contractors should maintain records, as insurers often require proof of basic safety practices, such as equipment inspections or fall protection protocols.

Completing the application requires synthesizing these elements into a cohesive narrative. Use a checklist to ensure no critical information is omitted: business details, claims history, safety records, and any additional requirements specified by the insurer. Tailor responses to the insurer’s questions, avoiding generic statements. For instance, instead of stating, “We prioritize safety,” describe specific measures like daily job site audits or investment in advanced protective gear. Finally, review the application for consistency and clarity before submission. Errors or inconsistencies can trigger requests for clarification, prolonging the process. A well-prepared application not only expedites approval but also positions your business as a low-risk candidate, potentially securing more favorable terms.

Understanding Multiplan PPO: Key Insurance Options Covered in Detail

You may want to see also

Explore related products

![]()

Cost Management: Bundle policies, improve safety practices, and adjust deductibles to reduce insurance premiums

Contractors often face steep insurance premiums due to the inherent risks in their work. However, strategic cost management can significantly reduce these expenses. One effective approach is bundling policies with a single insurer. By combining general liability, workers’ compensation, and commercial auto insurance, contractors can negotiate discounts of 10–25%. Insurers value the consolidated business and often reward it with lower rates. For instance, a mid-sized construction firm in Texas reported saving $12,000 annually by bundling their policies with a national carrier. This method not only cuts costs but also simplifies administration by having a single point of contact for claims and renewals.

Beyond bundling, improving safety practices is a proactive way to lower premiums. Insurers assess risk based on claims history and safety records. Implementing a robust safety program—such as OSHA-compliant training, regular equipment inspections, and incident reporting protocols—can reduce workplace accidents by up to 50%. A contractor in California saw their premiums drop by 15% after achieving an incident-free year, backed by documented safety measures. Investing in safety not only protects workers but also demonstrates to insurers that the contractor is a lower-risk client, leading to tangible savings.

Adjusting deductibles is another lever for cost control. Increasing the deductible on policies like general liability or property insurance can lower annual premiums by 10–30%. For example, raising a $1,000 deductible to $2,500 might save $500–$800 per year. However, this strategy requires careful consideration. Contractors should ensure they have sufficient cash reserves to cover the higher out-of-pocket costs in case of a claim. A small roofing company in Florida successfully reduced their premiums by 20% by opting for higher deductibles, but they also set aside a dedicated emergency fund to mitigate risk.

Combining these strategies amplifies their impact. A bundled policy with improved safety practices and higher deductibles can yield savings of 30% or more. For instance, a plumbing contractor in Illinois bundled their policies, implemented a safety program, and increased deductibles, reducing their total insurance costs by $8,500 annually. This holistic approach requires planning but delivers long-term financial benefits. By treating insurance as a manageable expense rather than a fixed cost, contractors can reinvest savings into their business, whether in equipment, training, or growth initiatives.

Can Insurance Companies Backtrack on Claims? Understanding Policy Limitations

You may want to see also

Frequently asked questions

Contractors should consider general liability insurance, workers' compensation insurance, commercial property insurance, and professional liability insurance (errors and omissions). Additionally, commercial auto insurance is essential if using vehicles for work.

Insurance costs are determined by factors such as the type of work, business size, claims history, coverage limits, and location. Higher-risk trades or larger operations typically result in higher premiums.

While some contractors may legally operate without certain types of insurance, doing so exposes them to significant financial risks, legal liabilities, and potential business closure in case of accidents, injuries, or property damage. Clients often require proof of insurance before hiring.