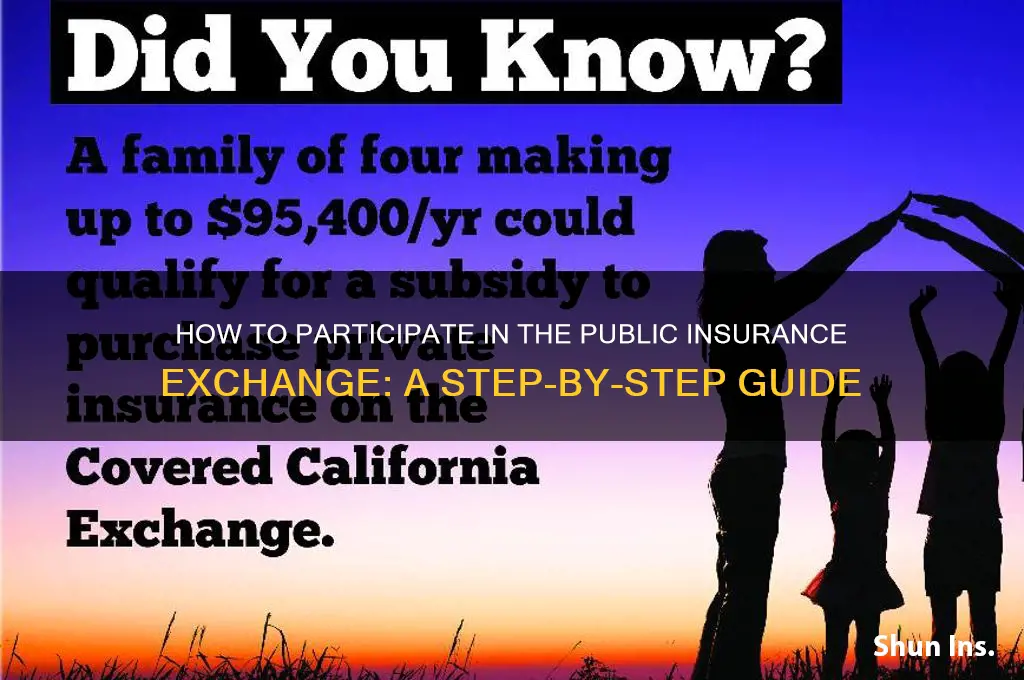

Participating in a public insurance exchange, also known as a health insurance marketplace, is a straightforward process designed to help individuals and families find affordable health coverage. To begin, you’ll need to determine if you qualify for the exchange, which is typically open to U.S. citizens or lawfully present immigrants who meet specific income criteria. During the annual Open Enrollment Period, usually from November to December, you can visit the official marketplace website, such as Healthcare.gov, or your state’s exchange platform to create an account. You’ll provide personal information, including income details and household size, to determine eligibility for subsidies or Medicaid. Once verified, you can browse available plans, compare coverage options, and select the one that best fits your needs. If you miss the Open Enrollment Period, you may qualify for a Special Enrollment Period due to life events like marriage, job loss, or the birth of a child. Assistance is available through navigators, brokers, or customer service representatives to guide you through the process and ensure you secure the right coverage.

Explore related products

What You'll Learn

- Understand Eligibility Criteria: Check income, citizenship, and residency requirements for public exchange participation

- Explore Available Plans: Compare coverage options, premiums, and provider networks offered on the exchange

- Enroll During Open Enrollment: Sign up within the specified period or qualify for special enrollment

- Apply for Subsidies: Determine eligibility for premium tax credits or cost-sharing reductions

- Submit Required Documents: Provide proof of income, identity, and household information for verification

![]()

Understand Eligibility Criteria: Check income, citizenship, and residency requirements for public exchange participation

Eligibility for public insurance exchanges hinges on three critical factors: income, citizenship, and residency. Each plays a distinct role in determining whether you qualify for subsidized health plans. Income thresholds, for instance, are tied to the Federal Poverty Level (FPL), with subsidies available to individuals earning between 100% and 400% of the FPL. For 2023, this translates to an annual income range of $13,590 to $54,360 for a single-person household. Understanding where you fall within this spectrum is the first step in assessing your eligibility.

Citizenship and immigration status are equally pivotal. To participate in a public exchange, you must be a U.S. citizen, a lawfully present immigrant, or meet specific criteria under the Affordable Care Act (ACA). For example, lawfully present immigrants, including those with green cards or refugee status, are eligible for marketplace plans. However, undocumented immigrants are excluded, though they may qualify for emergency services or state-specific programs. Verifying your status through documentation like a Social Security number or immigration papers is essential.

Residency requirements add another layer of complexity. You must live in the state where you’re applying for coverage, as each state operates its own exchange or uses the federal marketplace. Proof of residency, such as a driver’s license or utility bill, is typically required. Additionally, some states have expanded Medicaid under the ACA, offering coverage to adults with incomes up to 138% of the FPL. If your state has expanded Medicaid, you might qualify for this program instead of a marketplace plan, depending on your income.

Practical tips can streamline the eligibility verification process. Start by gathering key documents: tax returns for income verification, citizenship or immigration papers, and proof of residency. Use the Healthcare.gov subsidy calculator to estimate your eligibility for premium tax credits. If you’re near the income threshold, consider consulting a tax professional to optimize your financial situation. For those with fluctuating income, such as freelancers, averaging monthly earnings can provide a clearer picture of eligibility.

In summary, navigating eligibility criteria requires a meticulous approach to income, citizenship, and residency. By understanding these requirements and leveraging available tools, you can determine your qualification for public exchange participation and access affordable health coverage tailored to your circumstances.

Life Insurance Agents: What Not to Say

You may want to see also

Explore related products

![]()

Explore Available Plans: Compare coverage options, premiums, and provider networks offered on the exchange

Navigating the public insurance exchange can feel overwhelming, but exploring available plans is a critical step to securing coverage that fits your needs and budget. Start by understanding the four metal tiers—Bronze, Silver, Gold, and Platinum—each representing different levels of coverage and cost-sharing. Bronze plans typically have lower premiums but higher out-of-pocket costs, while Platinum plans offer the most comprehensive coverage with higher premiums. For example, a healthy 30-year-old might opt for a Bronze plan to save on monthly costs, while a family with frequent medical needs may find a Gold plan more cost-effective in the long run.

Once you’ve identified your preferred metal tier, compare premiums—the monthly amount you pay for coverage. Premiums vary based on factors like age, location, and household size. Use the exchange’s subsidy calculator to determine if you qualify for premium tax credits, which can significantly reduce your monthly costs. For instance, a single individual earning up to $60,000 annually may still be eligible for subsidies, depending on their state’s guidelines. Pairing premium analysis with subsidy eligibility ensures you’re not overpaying for coverage.

Provider networks are another crucial factor to evaluate. HMOs (Health Maintenance Organizations) typically require you to choose a primary care physician and stay within a specific network for care, while PPOs (Preferred Provider Organizations) offer more flexibility but often come with higher premiums. If you have a preferred doctor or specialist, verify their inclusion in a plan’s network before enrolling. For example, a PPO might be worth the extra cost if you require out-of-network care for a chronic condition.

Coverage options extend beyond premiums and networks—consider additional benefits like prescription drug coverage, mental health services, and maternity care. Silver plans, for instance, often include cost-sharing reductions for lower-income individuals, reducing out-of-pocket expenses like deductibles and copays. If you take regular medications, compare each plan’s formulary to ensure your prescriptions are covered at a reasonable cost. A plan with a slightly higher premium might save you money if it covers your medications with lower copays.

Finally, leverage the exchange’s comparison tools to streamline your decision-making process. Most exchanges allow you to filter plans by premium range, provider network, and specific benefits, making it easier to identify options that align with your priorities. Take notes on key differences between plans, such as deductibles, out-of-pocket maximums, and included services. By systematically comparing coverage options, premiums, and provider networks, you’ll be better equipped to choose a plan that balances affordability with the care you need.

Renewing Jetty Insurance: A Step-by-Step Guide for Policyholders

You may want to see also

Explore related products

![]()

Enroll During Open Enrollment: Sign up within the specified period or qualify for special enrollment

Open Enrollment is your annual opportunity to secure health insurance through the public exchange, typically running from November 1 to January 15 in most states. Missing this window means you could go without coverage for an entire year unless you qualify for a Special Enrollment Period (SEP). Mark your calendar, set reminders, and prepare necessary documents like income verification and identification ahead of time to streamline the process.

Qualifying for an SEP is your safety net if you miss Open Enrollment, but it’s not automatic. Life events such as losing job-based coverage, getting married, having a baby, or moving to a new state trigger eligibility. You generally have 60 days from the event to enroll, so act quickly. Keep detailed records of the qualifying event, as you may need to provide proof during the application process.

To enroll during Open Enrollment, visit Healthcare.gov or your state’s exchange website, create an account, and compare plans based on premiums, deductibles, and network coverage. Use the subsidy calculator to estimate financial assistance, which can significantly reduce costs for households earning up to 400% of the federal poverty level. For SEP enrollment, follow the same steps but select the option to report a life event during the application.

A common mistake is assuming Open Enrollment dates are the same nationwide—they’re not. Some states, like California and New York, extend their enrollment periods, so verify your state’s timeline. Another pitfall is delaying enrollment until the last minute, risking technical glitches or incomplete applications. Start early, review your options thoroughly, and don’t hesitate to seek assistance from navigators or brokers if needed.

Enrolling during Open Enrollment or qualifying for an SEP ensures you’re protected against unexpected medical expenses while avoiding penalties in states with individual mandates. It’s not just about compliance—it’s about peace of mind. Take control of your health and finances by understanding these windows and acting promptly. Your future self will thank you.

Does Arbella Insurance Allow Drivers? Coverage and Policy Insights

You may want to see also

Explore related products

![]()

Apply for Subsidies: Determine eligibility for premium tax credits or cost-sharing reductions

Applying for subsidies through a public insurance exchange can significantly reduce your healthcare costs, but eligibility hinges on specific criteria. Premium tax credits and cost-sharing reductions are primarily determined by your household income relative to the federal poverty level (FPL). For 2023, individuals earning between 100% and 400% of the FPL qualify for premium tax credits, while those between 100% and 250% of the FPL may also receive cost-sharing reductions. For example, a single individual earning up to $54,360 annually (400% FPL) could be eligible for premium tax credits, while a family of four earning up to $111,000 falls within the same range. Understanding these thresholds is the first step in determining your eligibility.

Once you’ve assessed your income, the next step is to gather necessary documentation. This includes recent tax returns, pay stubs, and any other proof of income. If you’re self-employed or have variable income, provide a detailed estimate of your annual earnings. The exchange will use this information to calculate your subsidy amount. For instance, if your income is 200% of the FPL, you may qualify for both premium tax credits and cost-sharing reductions, which can lower out-of-pocket costs like deductibles and copayments. Be precise in your documentation to avoid delays or miscalculations.

A common misconception is that subsidies are only for the unemployed or extremely low-income individuals. In reality, middle-income earners often qualify, especially in high-cost-of-living areas. For example, a family of three earning $80,000 in a state with a high FPL adjustment might still be eligible for premium tax credits. Additionally, special enrollment periods (e.g., after losing job-based coverage) allow you to apply for subsidies outside the annual open enrollment period. Knowing these exceptions can ensure you don’t miss out on financial assistance.

Finally, leverage available tools to streamline the process. Most public insurance exchanges offer online calculators to estimate your subsidy eligibility based on income and household size. For instance, Healthcare.gov’s "See Plans and Prices" tool provides a quick snapshot of potential savings. If you’re unsure about eligibility or need personalized guidance, consider consulting a certified navigator or broker. They can help interpret complex rules, such as how alimony or investment income affects your subsidy calculation. By combining self-research with expert assistance, you can maximize your chances of securing the subsidies you qualify for.

Understanding CSL in Insurance: Coverage, Limits, and Importance Explained

You may want to see also

Explore related products

![]()

Submit Required Documents: Provide proof of income, identity, and household information for verification

To participate in a public insurance exchange, one of the most critical steps is submitting the required documents for verification. This process ensures that your application is accurate and that you qualify for the appropriate coverage. The documents typically fall into three main categories: proof of income, proof of identity, and household information. Each serves a specific purpose in determining your eligibility and the level of assistance you may receive.

Proof of Income: This is perhaps the most scrutinized aspect of your application, as it directly influences your eligibility for subsidies or Medicaid. Acceptable documents include recent pay stubs, tax returns (Form 1040), W-2 forms, or a letter from your employer. If you’re self-employed, profit and loss statements or 1099 forms are often required. For those with irregular income, such as gig workers, bank statements or contracts can be submitted. It’s essential to provide documents that cover the most recent period, typically the past 30 days or the previous tax year, to ensure accuracy.

Proof of Identity: Verifying your identity is a mandatory step to prevent fraud and ensure that only eligible individuals receive coverage. Acceptable forms of identification include a valid driver’s license, state ID, passport, or birth certificate. For non-citizens, a Permanent Resident Card (Green Card), Employment Authorization Document (EAD), or other immigration documents are required. Ensure that the name on your identification matches the name on your application to avoid delays. If there’s a discrepancy, provide legal documentation, such as a marriage certificate or court order, to explain the difference.

Household Information: This category encompasses details about everyone in your household, including dependents and spouses. Required documents may include Social Security numbers, birth dates, and relationships to the primary applicant. For dependents, school records or custody agreements may be necessary to prove their inclusion in your household. If you’re applying for coverage as a family, ensure that all members’ information is accurate and up-to-date. Incomplete or incorrect household information can lead to denials or delays in processing your application.

Practical Tips for Submission: Organize your documents before beginning the application process to streamline submission. Keep digital copies of all documents for easy access and backup. If you’re unsure about which documents to provide, contact the exchange’s customer service for guidance. Be prepared to submit additional documentation if requested during the verification process. Finally, double-check all information for accuracy before submitting to avoid common errors that could delay your enrollment.

By carefully gathering and submitting the required documents, you can navigate the public insurance exchange process with confidence. This step is not just a formality—it’s the foundation of a successful application, ensuring you receive the coverage you need at the right cost.

Navigating Aetna: Am I Still Covered?

You may want to see also

Frequently asked questions

A public insurance exchange is a marketplace where individuals and small businesses can shop for and purchase health insurance plans. These exchanges are typically operated by state or federal governments and offer standardized plans with subsidies for eligible individuals based on income. Users can compare plans, check eligibility for financial assistance, and enroll in coverage during the open enrollment period or during a special enrollment period if they qualify.

Eligibility to participate in a public insurance exchange generally includes U.S. citizens, lawfully present immigrants, and individuals who are not incarcerated. Additionally, you must not have access to affordable employer-sponsored insurance. Eligibility for subsidies is based on income, typically between 100% and 400% of the federal poverty level, though this may vary by state.

To enroll, visit the exchange’s website (e.g., Healthcare.gov for the federal exchange or your state’s exchange site). Create an account, provide required information (income, household size, etc.), and compare available plans. Once you select a plan, complete the enrollment process and pay your first premium to activate coverage. Enrollment is typically open annually during the open enrollment period, but special enrollment periods may apply for qualifying life events.

You’ll need documents to verify your identity, income, and citizenship or immigration status. Common documents include a government-issued ID, Social Security numbers for all applicants, proof of income (e.g., tax returns, pay stubs), and immigration documents if applicable. Having these ready will streamline the application process.