When it comes to life insurance, it's crucial to understand your options and make informed decisions. While seeking advice from a licensed life insurance agent can be beneficial, it's important to remember that their primary goal is often to sell policies and earn commissions. To make the most of your interaction with an agent, be cautious about what you disclose. Avoid providing unnecessary personal information or expressing your fears and anxieties, as these can be used to influence your choices. Be mindful of high-pressure sales tactics and take your time to consider various options before committing to a policy. Remember, you have the right to shop around, compare prices, and choose what best suits your financial goals and risk tolerance.

| Characteristics | Values |

|---|---|

| Communication skills | An agent must be a good listener and communicator to earn the trust of their clients |

| Availability | Customers are more likely to be happy if their agent is available to answer their questions |

| Honesty | Agents should be honest and transparent about the terms of the insurance policy |

| Knowledgeable | Agents should be knowledgeable about the various policies and their features to help the customer make an informed decision |

| Licensed | Customers should only do business with licensed and well-reviewed agents or companies |

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

What You'll Learn

![]()

Don't say you want a policy without understanding your needs and budget

When it comes to life insurance, it's crucial to understand your needs and budget before committing to a policy. Here are some reasons why saying "I want a policy" without this understanding can be detrimental:

Understanding Your Needs: Life insurance is meant to provide financial security for your loved ones in the event of your passing. By understanding your needs, you can ensure that the policy you choose adequately covers those you leave behind. This includes considering your current financial situation, such as income, expenses, and any debts or liabilities. You should also think about your long-term and short-term financial goals to ensure the policy aligns with your overall financial plan.

Assessing Your Budget: Different life insurance policies come with varying costs, known as premiums. By understanding your budget, you can choose a policy with premiums that you can comfortably afford over the long term. Failing to consider your budget may result in choosing a policy with premiums that strain your finances, leading to potential lapses in coverage if payments become unaffordable.

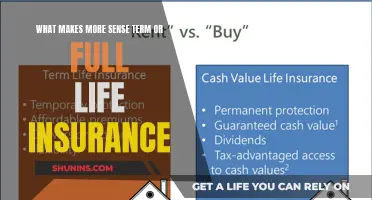

Selecting the Right Type of Policy: There are two main types of life insurance policies: term and permanent. Term insurance provides coverage for a specific period, often with lower premiums, while permanent insurance offers lifelong coverage and builds cash value over time. Understanding your needs and budget can help you decide which type of policy is more suitable. For example, if you have a limited budget and only need coverage for a certain period, term insurance might be a better option.

Customizing Your Coverage: Life insurance policies can be tailored to your specific needs and budget. By understanding your requirements, you can explore additional coverage options, such as riders or adjusted premiums to account for high-risk activities or pre-existing medical conditions. This customization ensures that your policy provides the necessary protection without breaking the bank.

Avoiding Overinsurance: Without a clear understanding of your needs and budget, you may end up purchasing more coverage than you require, resulting in overinsurance. This not only increases your premiums but may also lead to unnecessary financial burden on your beneficiaries, who could end up paying higher taxes on the benefits they receive.

In conclusion, taking the time to assess your needs and budget before meeting with a life insurance agent is crucial. It ensures that you make a well-informed decision, choose a policy that aligns with your financial goals, and avoid unnecessary costs or inadequate coverage. Remember, a good insurance agent should listen to your needs and help you find a policy that best suits your circumstances.

Gerber Life Insurance: Term or Whole Life?

You may want to see also

Explore related products

![]()

Avoid committing to a policy without knowing the exclusions

When purchasing a life insurance policy, it is crucial to understand the exclusions to ensure that your beneficiaries are adequately covered in the event of your death. Exclusions refer to specific situations or circumstances that could prevent your beneficiaries from receiving the death benefit payout. Here are some reasons why you should avoid committing to a life insurance policy without a clear understanding of the exclusions:

Understanding the Impact of Exclusions:

Firstly, knowing the exclusions in your policy is essential because it directly impacts whether your beneficiaries will receive the death benefit payout. If your death falls under an excluded situation, the insurance company may not be obligated to pay out any money, leaving your loved ones without the financial support you intended for them. This knowledge will help you make informed decisions about the level of coverage you need and whether you need additional policies to address specific risks.

Common Exclusions to Be Aware Of:

While exclusions vary across insurance providers, some common exclusions include suicide within a certain timeframe after purchasing the policy, dangerous or high-risk activities (such as skydiving, racing, or illegal activities), misstatement of age, and misrepresenting information during the application process. Additionally, some policies may not cover deaths related to illness, medical issues, or chronic health conditions, especially if they are pre-existing conditions. Understanding these common exclusions can help you ask the right questions and tailor the policy to your specific needs.

Customizing Your Coverage:

By being aware of the exclusions, you can customize your coverage to ensure it aligns with your unique circumstances. For example, if you have a high-risk job or hobby, such as piloting or rock climbing, you may need to discuss additional coverage options or riders with your agent. Some companies offer adjusted premiums or high-risk policies to provide more comprehensive coverage for these activities. Understanding the exclusions will empower you to make informed decisions about the level of protection you and your family require.

Peace of Mind and Financial Planning:

Knowing the exclusions in your life insurance policy provides peace of mind, ensuring that you and your beneficiaries are protected in the event of unforeseen circumstances. It allows you to plan your finances effectively, calculate the necessary coverage, and make informed decisions about your budget and long-term goals. Understanding exclusions can also help you assess whether you need to increase your coverage over time as your life circumstances change.

Shopping Around and Making Informed Choices:

Before committing to a policy, it is beneficial to shop around and compare different insurance providers. By understanding the exclusions, you can make informed choices about which provider offers the most comprehensive coverage for your specific needs. Remember to work with licensed and well-reviewed agents or companies who can guide you through the entire process and help you find a policy that meets your budget and coverage requirements.

Universal Life Insurance: Paid Up or Not?

You may want to see also

Explore related products

![]()

Don't ignore your high-risk job or hobbies

When applying for life insurance, it's important to be transparent about your job and hobbies. If you have a high-risk job or engage in dangerous hobbies, this could impact your insurance policy and premiums. Here are some reasons why you shouldn't ignore disclosing such information:

Understanding Risk Factors

All occupations carry certain risks, but some jobs are inherently more dangerous than others. High-risk jobs are those that require individuals to engage in hazardous activities on a regular or semi-regular basis. This includes professions such as firefighting, roofing in high-rise cities, logging, and working with heavy machinery. Even certain specialties within a profession, like a police officer on the SWAT team, can be considered higher risk than others.

Impact on Premiums and Coverage

Insurers will consider the relative risk of your job and hobbies when determining your insurance policy. High-risk occupations may result in steeper insurance premiums or even denial of coverage from some insurers. The risk associated with your job or hobbies can significantly impact the cost of your life insurance policy. Some companies may offer adjusted premiums or riders to cover high-risk activities more comprehensively.

Financial Protection for Loved Ones

If you have financial dependents, such as a spouse or children, life insurance becomes even more crucial. In the unfortunate event of your demise, life insurance provides financial security for your loved ones. It ensures that your family can maintain their standard of living and cover expenses such as housing, groceries, and education. The amount of coverage you need should be based on your income, the percentage of family expenses you contribute, and the number of dependents relying on your income.

Transparency and Disclosure

When applying for life insurance, it is essential to be honest and transparent about your job and any high-risk hobbies. Failing to disclose this information could lead to issues with your insurance policy. Be sure to ask your agent about potential exclusions and ways to tailor your policy to ensure complete coverage. Review your contract carefully to understand exactly what is and isn't covered.

Shopping for the Right Policy

When considering life insurance, it's beneficial to shop around and explore various options. Consult with independent agents who specialize in life insurance and can offer policies from multiple carriers. They can help you navigate the complexities of high-risk occupations and find a policy that suits your specific needs and budget. Remember, each insurance company may assess risk differently, so don't assume that all insurers will view your job or hobbies in the same way.

Alex Trebek's Life Insurance: Who Does He Represent?

You may want to see also

Explore related products

![]()

Don't hide pre-existing conditions

When applying for life insurance, it is crucial to be transparent about any pre-existing conditions. While it may be tempting to hide or downplay a medical condition to secure a more favourable premium, doing so can have serious consequences. Here are several reasons why full disclosure is essential when speaking with a life insurance agent:

Avoid Policy Cancellation and Legal Complications

If an insurance company discovers that you withheld or falsified information about your medical history, they may cancel your policy. This means that your beneficiaries could lose the death benefit that you intended for them. In some cases, nondisclosure may even be prosecuted as insurance fraud, leading to legal complications. Being honest about your pre-existing conditions ensures that your policy remains valid and protects your loved ones' interests.

Find the Right Coverage for Your Needs

Pre-existing conditions can impact the type of coverage that is most suitable for you. By disclosing your medical history, your life insurance agent can provide tailored advice and help you navigate the various options available. They can assist in finding a policy that aligns with your specific health situation and ensure that you are adequately covered. Remember, not all insurance companies evaluate risk factors in the same way, so getting quotes from multiple providers can help you find the best fit.

Take Advantage of Specialist Agents and Policies

There are life insurance agents who specialise in high-risk cases and policies designed for individuals with health concerns. These agents have the expertise to guide you through the complexities of obtaining life insurance with pre-existing conditions. They can match you with the right policy, ensuring that your unique needs are met. By being open about your pre-existing conditions, you can benefit from their specialised knowledge and find solutions that might not be available through standard policies.

Demonstrate Effective Management of Your Condition

When discussing your pre-existing conditions, it is essential to highlight the steps you are taking to manage your health effectively. Insurance companies consider the severity of your condition and the measures you are taking to control it. By demonstrating proactive management, such as regular medical care, medication adherence, or lifestyle changes, you can improve your chances of securing a policy. Insurance providers view applicants who actively manage their health more favourably, as it indicates a lower risk and may result in more favourable premium rates.

Peace of Mind and Long-Term Benefits

Obtaining life insurance with full disclosure of your pre-existing conditions provides peace of mind for you and your loved ones. Knowing that you have adequate coverage despite your medical history ensures confidence in your policy's validity and the benefits it provides. Additionally, as your health improves or your circumstances change, you may be able to adjust your policy or switch to a more conventional plan with lower premiums in the future. Being honest from the outset lays the foundation for long-term benefits and flexibility.

Switching Life Insurance: Is It Possible to Change Providers?

You may want to see also

Explore related products

![]()

Don't sign without reading the terms

When it comes to life insurance, it's crucial to understand the terms and conditions of your policy before signing on the dotted line. Here are some key reasons why you should never sign without thoroughly reading and understanding the terms:

Understanding Your Coverage: Life insurance policies can vary significantly in terms of coverage. By reading the terms, you'll know exactly what is and isn't covered. For instance, if you have a high-risk job or hobby, such as skydiving or piloting, some policies may exclude claims related to these activities. Understanding the exclusions and inclusions will help you make an informed decision about the level of coverage you need.

Financial Planning: Life insurance is an essential part of financial planning. By reading the terms, you can determine if the coverage aligns with your financial goals. Consider your current income and expenses, and the number of years you need the coverage for. This will help you calculate the appropriate death benefit amount to ensure your loved ones are financially protected after you're gone.

Policy Details and Definitions: Life insurance policies contain crucial details such as the death benefit amount, premium payments, policy number, issue date, and beneficiaries. Reading the terms will help you identify these key elements and ensure they meet your expectations. Understanding policy definitions is also vital to knowing exactly what you're signing up for.

Free-Look or Review Period: Many life insurance policies offer a "free-look" or review period, typically lasting 10 to 30 days, during which you can review and evaluate the policy. If you're not satisfied, you have the right to cancel during this period without penalty. By reading the terms, you'll be aware of this option and can utilize it if needed.

Insurable Interest and Beneficiaries: Life insurance policies require you to have an insurable interest, meaning you must prove financial dependence on the insured person. Reading the terms will help you understand this requirement and ensure you meet the criteria. Additionally, you'll want to confirm the beneficiaries listed in the policy and make any necessary changes.

Variable Life Insurance Considerations: If you're considering variable life insurance (VL), which allows investment of the cash value in subaccounts, it's crucial to understand the market risks involved. Reading the terms will help you assess the potential growth or fluctuation in the policy's cash value and death benefit due to market performance.

In conclusion, taking the time to read and understand the terms of your life insurance policy is of utmost importance. It ensures you make informed decisions about your financial future and guarantees that you and your loved ones receive the protection you need. Remember, if you have any questions or concerns, a licensed and well-reviewed independent agent can provide valuable guidance and help you find a policy that suits your specific needs.

Life Insurance at 90: Is It Possible to Get Covered?

You may want to see also

Frequently asked questions

A good insurance agent will be able to offer a comprehensive selection of products and services to meet your needs. They should listen carefully to your needs and be able to offer a range of options, not just the ones that will earn them the highest commission. They should also be able to explain the tax and legal aspects of the products they sell and how they fit into your financial situation.

Term insurance generally has lower premiums than permanent policies but does not build up cash value. Term covers you for a fixed term, and if you die within that term, death benefits are paid out. Permanent insurance policies remain in place as long as the premium is paid and build up cash value that increases over time. Variable life insurance (VL) policies allow you to invest the cash value in various subaccounts, which can lead to growth but also involves market risk.

Ask about potential exclusions and ways to tailor your policy for complete coverage, especially if you have a high-risk job or hobby. Discuss pre-existing conditions and no-medical-exam policies. Ask about the process for adjusting your coverage if your circumstances change.

Only do business with a licensed and well-reviewed insurance agent or company. Understand how much coverage you need, for how long, and what you can afford to pay. Remember that life insurance is not a one-size-fits-all purchase, so get expert advice and ensure the agent understands your financial situation and goals.