If you've paid for gap insurance upfront and then cancel it, you may be eligible for a refund on the unused portion of the policy. This usually happens when you pay off your loan early, or sell or trade in your vehicle before the loan is paid off. The amount of the refund will depend on how far into the policy you are, and how you've been paying – if you pay monthly, you will only get a refund on the current month if you're early on in the month. If you're cancelling within 30 days of the policy start date, you may be able to get a full refund minus any fees.

| Characteristics | Values |

|---|---|

| When you can get a refund | Paying off your loan, switching insurance companies, selling or trading your car |

| When you cannot get a refund | Your car is declared a total loss and your insurance policy has paid out, your insurance policy has expired, you have not paid your premium |

| How to get a refund | Contact your insurance company, provide proof of sale/trade/payoff, submit any required forms |

| How long it takes to get a refund | Typically 4-6 weeks, but can vary by company and state |

| How to calculate a refund | Divide the total cost of insurance by the number of months of coverage, then multiply the monthly premium by the number of months left on the policy |

Explore related products

$8.49 $14.99

What You'll Learn

![]()

When you can get a refund

You can get a gap insurance refund in several situations. Here are the most common ones:

Paying Off Your Loan Early

If you pay off your car loan early, you can get a partial refund for the GAP coverage that you haven't used yet. This is because you've already used a portion of your GAP insurance policy while your loan was active, so you'll only get back a prorated refund for the unused part.

Switching to a Different Insurance Company

If you're not satisfied with your current insurance provider, you can switch to a different company and cancel your original policy. In this case, you'll be eligible for a refund for the cancelled coverage you didn't use. If you cancel within 30 days of the policy's start date, you may receive a full refund (including GAP insurance costs). Cancelling after 30 days will usually result in a prorated refund, but this can vary depending on your insurance provider and your policy details.

Selling or Trading In Your Car

If you sell or trade in your car, you can get a refund on the amount of GAP insurance coverage you didn't use. It's important to wait until the car is legally sold or traded before cancelling your insurance to ensure you receive the refund. For example, if you bought a year's worth of GAP insurance and sold your car after three months, you would be eligible for a refund for the remaining nine months of unused coverage.

Refinancing Your Car Loan

Refinancing your car loan can also lead to a GAP insurance refund. If you refinance with a shorter loan term and a lower interest rate, you may pay off your car faster and no longer need GAP insurance. Check your loan documents to see if GAP insurance is still necessary, and if it's not, contact your insurance agent to discuss getting a refund for the unused premium.

Vehicle or Person: Who's Insured?

You may want to see also

![]()

When you can't get a refund

There are a few scenarios in which you are not eligible for a GAP insurance refund. These include:

- Your car being declared a total loss and your GAP policy paying out the difference between the car's value and your loan balance. In this case, the insurance provider considers their obligation met or exceeded, and they are no longer responsible for payouts on the policy.

- Your GAP insurance policy has expired.

- The deadline by which you must formally make a claim has expired, as detailed in your policy.

- You have not paid your GAP policy premium.

- You have filed a claim against the policy.

- Your car has been totaled or stolen and you file a GAP insurance claim.

It is important to note that the eligibility criteria and specific situations that allow for a GAP insurance refund may vary depending on your insurance provider and the specific terms of your policy. Be sure to carefully review your policy and contact your insurance provider for clarification if needed.

Recording Insurance Proceeds: Vehicle Loss

You may want to see also

![]()

How to request a refund

To request a refund for your gap insurance, you must meet certain criteria. You need to have paid for your coverage upfront and in full. If you pay monthly, you may still get a refund, but it will be much smaller. You also need to cancel your policy before the period expires. If you have filed a claim, you will not be eligible for a refund.

If you meet the criteria, the first step is to contact your insurance company or agent and inform them that you want to cancel your policy. They will let you know what paperwork you need to fill out and what other information is required. Most insurance companies will need to see an odometer disclosure statement verifying the car's current mileage, which you can get from your state's DMV website. If you have paid off your auto loan, the insurance company may also request a letter from your lender verifying that the loan has been closed.

Once you have submitted all the necessary paperwork and documentation, you should receive your refund. Most insurance companies will allow you to choose between receiving a physical check or a direct deposit to your bank account.

It is important to note that you will only receive a refund for the gap insurance that you have not used. For example, if you paid for a year of coverage but cancel after three months, you will only get a refund for the remaining nine months. The amount of your refund will also depend on how far into your coverage you are when you cancel your policy. If you cancel within 30 days of the policy start date, you may be able to get a full refund. If you cancel after 30 days, your refund will be prorated.

Vehicle Insurance: Active or Not?

You may want to see also

![]()

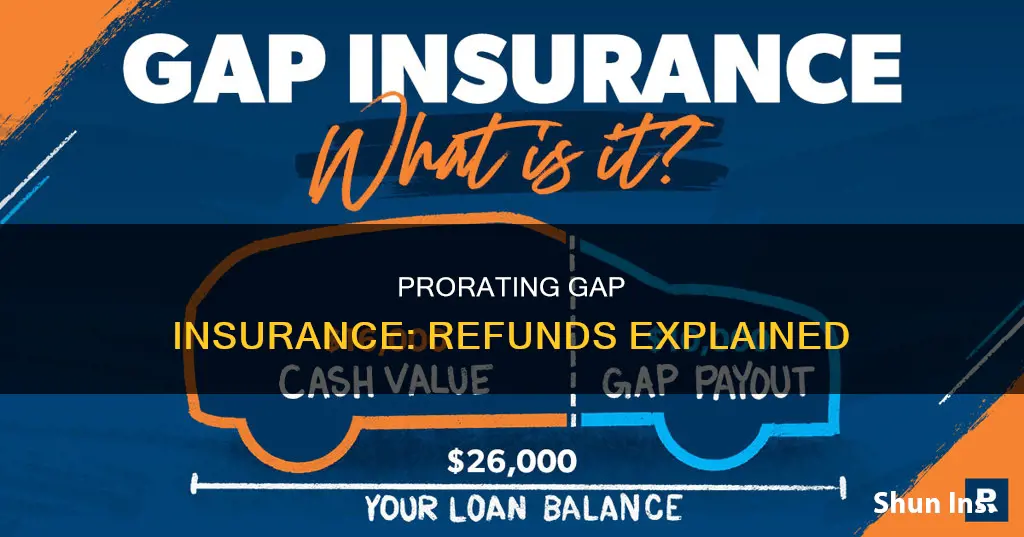

How much you'll get back

The amount of money you'll get back from a gap insurance refund depends on several factors. Firstly, you'll need to have paid for the GAP insurance upfront to qualify for a refund. If you paid monthly, you may still get a refund, but it will likely be much smaller than if you paid upfront.

The amount of your refund is also based on how you pay your insurance bill. If you pay monthly, you won't get a refund because you've only paid for the coverage you've received so far. If you pay your insurance in a lump sum, the amount of your refund will depend on how far into your coverage you were when you cancelled your policy.

The refund amount you may be eligible for will depend on the cost of your gap insurance premium and how long is left on your current policy. Most policies cover 12 months and are paid annually.

To calculate your refund, divide the total cost of the insurance by the number of months you had coverage. This gives you your monthly premium. Once you know the monthly premium, you can multiply it by the number of months left on your policy. This will give you a good indication of how much your refund should be, but all insurance providers have different processes, so you'll need to confirm the amount of your refund with them.

For example, if you paid for a gap insurance policy starting in early January and want to cancel in late April, you'll likely qualify for a refund equating to eight months of unused coverage. If your annual premium is $60, divided by 12 months, that's about $5 per month. If you are eligible for a refund of the unused eight months, that would total $40.

Insuring Rare Vehicles: Payout Process

You may want to see also

![]()

How long it takes to get a refund

The time it takes to get a refund on your gap insurance policy depends on your insurance provider and your location. Gap insurance refunds involve paperwork, so you can expect it to take at least a few weeks. The typical gap insurance refund payout time is within 30 days, but this can vary depending on the company and state regulations. Mark Friedlander, a spokesman for the Insurance Information Institute, states that refund timing can differ by company and state regulations.

To request a refund, you must first contact your insurance company and ask them to cancel your gap insurance and issue a refund for the unused coverage. They will then provide you with the necessary paperwork and inform you of any additional information or documentation required, such as proof of the sale, trade, or payoff of your vehicle. Most insurance carriers will need to see an odometer disclosure statement verifying the car's current mileage, which can be obtained for free from your state's DMV website. If you have paid off your auto loan, the insurance company may also request a letter from your lender confirming this.

Once you have submitted all the necessary paperwork and documentation, you should receive your refund. Most insurance companies will give you the option of receiving your refund via physical check or direct deposit into your bank account. Remember that you must proactively request a gap insurance refund, as most insurance companies will not offer them automatically.

Report Uninsured Vehicles: A Quick Guide

You may want to see also

Frequently asked questions

You can get a refund on your gap insurance if you pay off your car loan early, sell or trade in your car, or switch to a different insurance company. You can also get a refund if your loan balance is no longer more than the car's actual value.

You cannot get a refund on your gap insurance if your insured car is declared a total loss before the policy's expiration date. In this case, the gap insurance will pay the difference between the car's value and the loan balance, but you will not be eligible for a refund for the remaining months of coverage.

The amount of money you will get back through a refund varies but is usually based on the following factors: the value of the vehicle, the amount of the auto loan, the vehicle's current mileage, and the loan repayment term.

To get your refund, contact your gap insurance provider and tell them you want to cancel your gap insurance and get a refund for the remaining coverage. You will then need to submit the appropriate paperwork, such as proof of sale or auto payoff letter.