Self-insurance is a risk management strategy where a business sets aside funds to pay for unexpected losses instead of buying insurance. This strategy can be applied to medical coverage, where employers can provide health benefits to their employees and fund claims from a specified pool of assets. Self-insurance for medical coverage is becoming increasingly popular among businesses of all sizes due to rising healthcare costs and regulatory changes. This approach allows businesses to have more control over their costs and benefit design, but it also comes with the risk of facing financial stress if a costly event occurs.

| Characteristics | Values |

|---|---|

| Definition | Self-insurance involves setting aside your own money to pay for a possible loss instead of purchasing insurance and expecting reimbursement. |

| Application | To receive self-insured status, an employer must qualify through an application process, meet specified financial requirements, and be approved by the relevant authority. |

| Benefits | Self-insurance can save money since you aren't paying insurance premiums, allow for greater benefit flexibility, and enable better cost management. |

| Risks | Self-insurance carries the risk of facing financial devastation if an event occurs that is costlier than anticipated. It may also create employee privacy concerns if a third-party administrator is not hired. |

| Suitability | Self-insurance is generally more suitable for larger companies with more significant financial resources and a larger pool of employees to spread the risk. |

Explore related products

What You'll Learn

![]()

Advantages of self-insuring a business for medical

There are several advantages to self-insuring a business for medical coverage. Firstly, it can reduce costs for the business by eliminating insurance premiums, administrative costs, and profit margins for the insurer. Self-insurance allows businesses to pay only for the cost of their claims, which can result in significant savings, especially for large companies with a large number of employees. This cost reduction can be a primary driver for companies deciding to self-insure.

Secondly, self-insurance provides benefit flexibility and control to the employer. They can design and customize their employee benefit package, making it more attractive to current and future employees. For example, they can offer their employees the choice to see any doctor or specialist they prefer. Additionally, they can set their own deductibles, co-payments, and maximum benefits, allowing them to manage their costs more effectively.

Thirdly, self-insurance can increase awareness of risks and encourage long-term risk management. Businesses are incentivized to analyze their risks and set aside funds accordingly, based on past and future risk assessments. This can lead to more informed financial planning and potentially reduce the impact of unforeseen events.

Lastly, self-insurance can be advantageous for businesses that want to provide specific benefits to their employees, such as chiropractic care, dental, vision, or life insurance benefits. It allows employers to tailor their benefits to the specific needs of their workforce, which can enhance employee satisfaction and retention.

While self-insuring offers these benefits, it is important to remember that there are also risks involved, particularly regarding the potential for high-cost claims. Businesses considering self-insurance should carefully evaluate their financial situation and risk exposure to ensure they can adequately cover potential claims.

Medical Insuring and Coding: A Quick Career Path

You may want to see also

Explore related products

![]()

Disadvantages of self-insuring a business for medical

While self-insuring a business for medical claims can offer greater control and flexibility, there are several disadvantages to consider. Here are some of the key disadvantages:

Financial Risk

The main disadvantage of self-insuring is the potential for greater financial risk. In a self-insured plan, the employer assumes the financial risk of providing healthcare benefits to employees and pays for medical claims out-of-pocket as they are incurred. This means that if claims are higher than anticipated or in the event of a catastrophic event, the business could face significant financial strain.

Administrative Burden

Self-insuring can also create an administrative burden for the business. Handling and processing claims in-house can be time-consuming and resource-intensive, requiring additional staff or the use of a third-party administrator (TPA). Additionally, businesses need to ensure that their claim processing complies with regulatory requirements.

Lack of Risk Pooling

Self-insuring means the business is not part of a risk pool, as they would be with traditional insurance. This can impact the business's ability to manage risk and may result in higher costs if claims exceed expectations.

Employee Privacy Concerns

Without a TPA, employee privacy concerns may arise as staff will be processing claims for their coworkers. This can create tensions and put the employer in the difficult position of having to deny coverage to an employee directly.

Cash Flow Fluctuations

With self-insurance, claim expenses can vary significantly from month to month, making it challenging to predict and manage cash flow. While self-insurance can improve overall cash flow management by eliminating the need for regular premium payments, the variability of claim costs can be a disadvantage.

Medical Insurance: ED Treatment Coverage Explained

You may want to see also

Explore related products

![]()

Requirements for becoming self-insured

Financial Requirements

Businesses must be in an excellent financial position to become self-insured. In California, regulatory financial requirements include:

- Three calendar years in business in a legally authorized business form.

- Three years of certified, independently audited financial statements.

- An acceptable credit rating for three full calendar years before the application.

- A separate application for each subsidiary or affiliate company of a private applicant.

Administrative Requirements

Self-insured businesses must handle their own claims and make payments. This can be done by hiring additional staff or outsourcing to a third-party administrator (TPA). In California, new self-insurers are required to use a licensed TPA for their first three years of self-insurance. Self-insurers are also subject to periodic audits to verify the accuracy of claims and the correctness of reported liabilities.

Benefits and Coverage

Self-insured employers are required to provide the same scope of benefits as an insurance company. In California, self-insurers must implement an effective Injury and Illness Prevention Program as required by the Labor Code. Self-insured businesses can set their own deductibles, co-payments, and maximum benefits, and they have complete control over which benefits they want to offer.

Risk Management

Self-insurance is suitable for businesses with a low risk of claims or those that can afford to pay for potential losses. Self-insurance may be a good option for businesses with predictable, low-cost claims, as it can save money on insurance premiums. However, there is a risk of financial stress or devastation if an event occurs that is costlier than anticipated.

Size of the Business

Larger companies with many employees tend to benefit more from self-insurance as they can spread their risk over a larger pool of employees. However, even small businesses can benefit from self-insurance, depending on the area of coverage.

Please note that these are general guidelines, and specific requirements may vary depending on your location and industry. It is essential to review your business's unique circumstances and consult relevant regulatory agencies before making any decisions regarding self-insurance.

Private Medical Insurance: A Multi-Billion Dollar Industry

You may want to see also

Explore related products

![]()

How to save for self-insurance

Self-employed people can be eligible to deduct up to 100% of the premiums they pay for coverage. This includes medical, dental, and vision insurance, qualifying long-term care coverage, and Medicare premiums for yourself, your spouse, dependents, and any non-dependent children under 27 at the end of the tax year. However, you cannot deduct the premiums if you are eligible to participate in an employer-subsidized health plan.

To save for self-insurance, you can take advantage of other health-related deductions. For example, if you have a high-deductible health plan (HDHP), you may be eligible to contribute to a Health Savings Account (HSA). Contributions to an HSA are tax-deductible, and you can use the money to pay for qualified medical expenses. The money in an HSA can be withdrawn without penalties or taxes to pay for these expenses.

Another way to save for self-insurance is to review your health insurance options annually. Health insurance premiums tend to fluctuate each year, so reviewing your plan annually can help you ensure you're getting the best coverage for your money. You can also optimize your business structure to make it more tax-efficient. Work with a tax professional to determine how to structure your business to minimize your tax burden.

Additionally, keep detailed records of your health insurance payments. Save copies of invoices and proof of payment. Detailed records will make it easier to calculate deductions and provide documentation in case of an audit. Keep receipts from your healthcare providers and letters of medical necessity for any recommended purchases.

Medical Insurance and Teeth Whitening: What's Covered?

You may want to see also

Explore related products

![]()

Wellness programs and coverage options

Wellness programs are becoming an increasingly popular way for businesses to reduce healthcare expenses. These programs promote preventative health measures and disease management initiatives for employees, with the hope that early intervention will reduce incurred medical costs and absenteeism.

A study by the RAND Employer Survey found that 80% of employers reported that their wellness program decreased absenteeism and increased productivity. The Wellness Councils of America reported that for every dollar spent on a wellness program, three are saved.

Wellness programs can be offered by an insurance company and included in a company's insurance plan, or they can be provided by a vendor outside of the company's health insurance plan.

Some insurance companies that offer wellness programs include:

- Cigna: Cigna offers wellness programs that focus on five key areas: physical, emotional, environmental, social, and financial.

- Aetna: Aetna offers employees the option to work with a lifestyle coach, providing personalized one-on-one phone coaching, as well as group and self-paced digital coaching.

- Blue Cross Blue Shield: Offers wellness programs through their platform, Blue365.

- Highmark: Offers mental health resources, personalized health and wellness coaching, preventative on-site screenings, and engagement rewards.

There are also independent vendors that offer wellness programs, such as:

- Wellness360: Provides a customizable platform that addresses the unique needs of a company's workforce, with incentivized wellness initiatives.

- Wellworks For You: A global provider of wellness services, offering a different approach to traditional corporate wellness programs to increase participation.

- Vitality: Offers a holistic approach to health and wellbeing through its Elevate platform, with personalized pathways to health and incentives for wellness activities.

- Avidon Health: Offers a digital coaching platform with a member portal, curated content, and a course library, which can be tailored to an organization's needs.

When choosing a wellness program, it is important to consider the unique needs and interests of your employees, and to gather ongoing feedback to ensure the program remains effective and relevant.

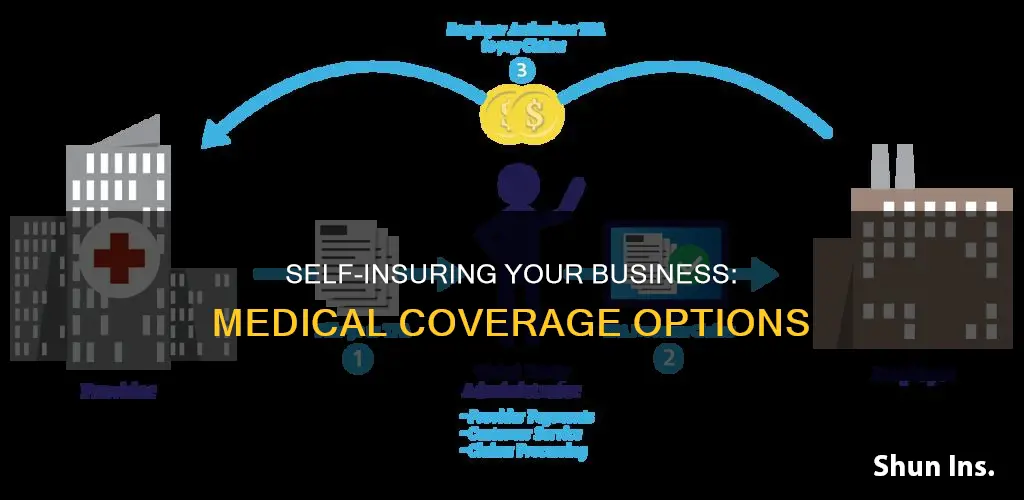

In addition to wellness programs, there are a variety of coverage options available for self-insured businesses. A self-insured group health plan, or 'self-funded' plan, is one in which the employer assumes the financial risk of providing healthcare benefits to its employees. The employer pays for each out-of-pocket claim as it is incurred, rather than paying a fixed premium to an insurance carrier. Self-insured employers often set up a special trust fund to earmark money for claims and may purchase stop-loss insurance to reimburse them for claims above a certain dollar level.

Some coverage options for self-insured businesses include:

- Fully-insured plans: The employer purchases insurance from an insurance company, paying a fixed premium.

- Self-funding plans: The employer pays the benefits administration and absorbs the risk for managing its claim costs.

- Balanced Funding: Florida Blue offers a combination of fully-insured and self-funding plans, with fixed monthly payments and potential credits if medical claims are lower than expected.

It is important to note that self-insurance may not be a viable option for small employers or those with poor cash flow, as they must have the financial resources to cover the risk of paying health claim costs.

Medicaid and Life Insurance: Cash Value at Risk?

You may want to see also

Frequently asked questions

Self-insurance involves setting aside money to pay for a possible loss instead of buying insurance and expecting reimbursement. Self-insurance is a strategy for mitigating the possibility of future loss by putting aside a set portion of your money.

Self-insurance can save money since you aren't paying insurance premiums. It also allows you to set your own deductibles, co-payments, and maximum benefits, as well as monitor your business's costs more easily. However, the biggest disadvantage of self-insurance is the risk of an event occurring that is costlier than what was anticipated, potentially causing financial stress or devastation.

Some things to consider include the size of your company, administrative costs, employee privacy concerns, and cash-flow fluctuations. It's also important to have an accurate understanding of the worst-case scenario so you're prepared financially.