The concept of insurance within the Atena marketplace is a critical aspect for both buyers and sellers, offering a layer of financial protection and security in transactions. Atena marketplace insurance typically covers risks such as product damage, loss during shipping, or disputes between parties, ensuring that all participants can engage in trade with greater confidence. This type of insurance is particularly important in online marketplaces, where the physical inspection of goods before purchase is often not possible, and where the potential for fraud or miscommunication exists. By providing insurance options, Atena not only safeguards its users but also enhances the overall trustworthiness and reliability of its platform, fostering a more robust and dynamic trading environment.

Explore related products

$4.99

$15.89

What You'll Learn

![]()

Atena Marketplace Insurance Coverage Options

Atena Marketplace Insurance offers a range of coverage options tailored to meet diverse needs, ensuring that individuals and businesses can find a plan that aligns with their specific requirements. Whether you’re a small business owner, a freelancer, or an individual seeking comprehensive protection, Atena’s marketplace provides flexibility and choice. The key lies in understanding the available options and selecting the one that best fits your circumstances.

One standout feature of Atena Marketplace Insurance is its tiered coverage plans, which cater to different budgets and risk levels. For instance, the Basic Plan is ideal for those seeking essential coverage at a lower cost, typically covering liability and minimal property damage. This plan is particularly suited for startups or individuals with limited assets. On the other end, the Premium Plan offers extensive protection, including higher liability limits, business interruption coverage, and specialized add-ons like cyber liability insurance. This option is recommended for established businesses with significant assets and higher risk exposure.

When evaluating Atena’s coverage options, it’s crucial to consider your unique risk profile. For example, a tech company might prioritize cyber liability coverage, while a retail business may focus on property and inventory protection. Atena’s marketplace allows for customization, enabling you to add riders or endorsements to tailor your policy. Practical tip: Use Atena’s online assessment tool to identify potential risks and receive personalized recommendations based on your industry and business size.

Comparatively, Atena’s marketplace stands out for its transparency and user-friendly interface. Unlike traditional insurance providers, Atena provides clear breakdowns of each plan’s inclusions and exclusions, making it easier to make informed decisions. Additionally, their customer support team offers guidance without pushing unnecessary upgrades, ensuring you only pay for what you need. This approach fosters trust and long-term satisfaction among policyholders.

In conclusion, Atena Marketplace Insurance coverage options are designed to be adaptable, comprehensive, and accessible. By carefully assessing your needs and leveraging the available tools, you can secure a policy that provides peace of mind without breaking the bank. Whether you opt for a basic plan or a fully customized premium package, Atena ensures you’re covered for whatever comes your way.

How Much Life Insurance Can You Get?

You may want to see also

Explore related products

![]()

Claims Process for Atena Marketplace Policies

Navigating the claims process for Atena Marketplace policies requires clarity and precision. Unlike traditional insurance, Atena’s marketplace model often integrates multiple providers, meaning claims may involve tiered approvals or shared liability. Policyholders must first identify whether their claim falls under a single provider or a collaborative network, as this dictates the initial point of contact and documentation requirements. For instance, a health-related claim might require pre-authorization from both the primary insurer and a secondary specialist network within the marketplace.

The first step in filing a claim is to gather all necessary documentation, which typically includes proof of purchase, medical records (if applicable), and incident reports. Atena’s marketplace policies often emphasize digital submissions, so ensure all files are in compatible formats (PDF, JPEG) and uploaded via their secure portal. A common oversight is failing to include the policy number in the file names, which can delay processing. Pro tip: Use the policy number as a prefix for every document to streamline verification.

Once submitted, claims enter a review phase that varies in duration based on complexity. Simple claims, such as minor property damage, may resolve within 7–10 business days, while medical or liability claims can take 30–45 days. Atena’s marketplace structure sometimes introduces an additional layer: cross-provider reviews. For example, a claim involving a workplace injury might require approval from both the health insurer and the employer’s liability provider. Policyholders can expedite this by proactively contacting both parties to confirm receipt of documents.

A critical aspect of Atena’s claims process is the appeals mechanism. If a claim is denied, policyholders have 60 days to file an appeal, supported by additional evidence or a detailed explanation. Unlike standard insurance, Atena’s marketplace policies often allow for mediation between providers during appeals, particularly in cases of disputed liability. For instance, if a health claim is denied due to a provider’s exclusion clause, the marketplace’s ombudsman may intervene to negotiate coverage.

Finally, policyholders should leverage Atena’s digital tools to track claims in real time. The marketplace’s app provides updates on each stage of the process, from initial submission to final resolution. However, be cautious of relying solely on automated notifications; periodic follow-ups via phone or email can prevent claims from stagnating in administrative limbo. By understanding these nuances, policyholders can navigate Atena’s claims process with confidence and efficiency.

Whole Life Insurance: A Child's Smart Investment Strategy?

You may want to see also

Explore related products

![]()

Premiums and Cost Factors in Atena Plans

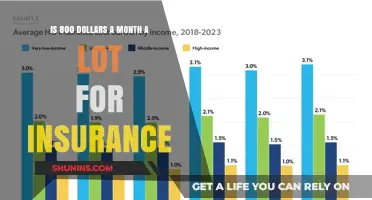

Atena marketplace insurance plans, like any health insurance, are influenced by premiums and cost factors that can vary widely based on individual circumstances. Understanding these elements is crucial for making informed decisions. Premiums, the monthly payments for coverage, are not one-size-fits-all. They are calculated using a combination of personal and plan-specific factors, ensuring that the cost reflects the level of risk and coverage provided.

One of the primary determinants of premiums in Atena plans is age. Younger individuals typically pay lower premiums because they are statistically less likely to require extensive medical care. For example, a 25-year-old might pay $200–$300 monthly for a mid-tier plan, while a 55-year-old could see premiums of $600–$800 for similar coverage. This age-based pricing reflects the increased health risks associated with aging. Additionally, location plays a significant role, as healthcare costs vary by region. Urban areas with higher living costs often have more expensive premiums compared to rural regions.

Another critical factor is the plan’s metal tier—Bronze, Silver, Gold, or Platinum—which determines the balance between premiums and out-of-pocket costs. Bronze plans have the lowest premiums but higher deductibles and copays, making them suitable for those who rarely need medical care. Conversely, Platinum plans offer the lowest out-of-pocket costs but come with significantly higher premiums, ideal for individuals anticipating frequent medical visits. For instance, a Bronze plan might have a $400 monthly premium with a $6,000 deductible, while a Platinum plan could cost $800 monthly with a $500 deductible.

Lifestyle and health habits also impact premiums. Smokers, for example, often face higher rates due to increased health risks. Some Atena plans may charge smokers up to 50% more than non-smokers. Similarly, pre-existing conditions can affect costs, though the Affordable Care Act limits how much insurers can charge based on health status. Subsidies and tax credits available through the marketplace can offset these costs for eligible individuals, making coverage more affordable.

To optimize costs, consider these practical tips: assess your healthcare needs annually to choose the right metal tier, take advantage of preventive services covered at no cost, and explore subsidy eligibility using the marketplace’s calculator. By understanding these cost factors and leveraging available resources, you can select an Atena plan that balances affordability with comprehensive coverage.

Mastering Cobra Insurance: A Step-by-Step Guide to Seamless Enrollment

You may want to see also

Explore related products

![]()

Eligibility Requirements for Atena Marketplace Insurance

Atena Marketplace Insurance, often sought by individuals and families navigating health coverage options, has specific eligibility criteria that determine who can enroll. Understanding these requirements is crucial for anyone considering this insurance plan. The first key factor is residency status: applicants must be lawful residents of the state where the insurance is offered. This ensures compliance with local regulations and guarantees that the coverage aligns with state-specific healthcare mandates.

Another critical eligibility requirement is income level. Atena Marketplace Insurance is designed to assist individuals and families whose income falls within certain thresholds, typically between 100% and 400% of the Federal Poverty Level (FPL). For example, in 2023, a family of four with an annual income between $28,000 and $112,000 would generally qualify. These income limits are adjusted annually, so it’s essential to verify the current figures during enrollment.

Age and citizenship status also play a role in eligibility. Applicants must be under 65 years old, as those eligible for Medicare are not qualified for Marketplace plans. Additionally, while U.S. citizens and lawfully present immigrants are eligible, undocumented immigrants are not. This distinction is vital for households with mixed immigration statuses, as it may affect family coverage options.

Lastly, existing health coverage can impact eligibility. Individuals with access to affordable employer-sponsored insurance or government programs like Medicaid may not qualify for Atena Marketplace Insurance. The plan is intended to fill gaps for those without other viable options, so applicants must demonstrate that they lack adequate coverage elsewhere. Practical tip: Use the Healthcare.gov screening tool to assess eligibility before applying, as it simplifies the process by pre-qualifying applicants based on their unique circumstances.

Life Insurance and W-2s: Where Does it Belong?

You may want to see also

Explore related products

![]()

Benefits and Limitations of Atena Coverage

Atena Marketplace insurance, often referred to as Atena coverage, is a popular choice for individuals seeking comprehensive health insurance plans. One of its standout benefits is the extensive network of healthcare providers, ensuring policyholders have access to a wide range of doctors, specialists, and hospitals. This network flexibility is particularly advantageous for those who travel frequently or require specialized care, as it minimizes out-of-network costs and simplifies the process of finding in-network providers. For example, Atena’s PPO plans allow members to visit any doctor without a referral, offering both convenience and autonomy in healthcare decisions.

However, a notable limitation of Atena coverage is its potentially higher premiums compared to other marketplace plans. While the comprehensive benefits justify the cost for many, budget-conscious individuals may find these premiums less appealing. Additionally, some plans come with high deductibles, which can delay significant cost savings until substantial medical expenses are incurred. For instance, a family plan with a $5,000 deductible may require careful financial planning to manage out-of-pocket costs before coverage fully kicks in.

Another benefit of Atena coverage is its robust preventive care offerings, which align with the Affordable Care Act’s mandate for essential health benefits. Policyholders can access free preventive services such as annual check-ups, vaccinations, and screenings for conditions like diabetes and cancer. This proactive approach not only promotes long-term health but also reduces the likelihood of costly treatments for preventable illnesses. For example, a 40-year-old policyholder could benefit from regular cholesterol screenings and smoking cessation programs included in their plan.

Despite these advantages, Atena coverage may fall short in customization options for certain demographics. While it offers a variety of plans, including HMO, PPO, and EPO options, individuals with specific healthcare needs—such as those requiring extensive mental health services or fertility treatments—may find that coverage is limited or requires additional riders. For instance, mental health coverage might be capped at a certain number of therapy sessions per year, necessitating out-of-pocket expenses for additional care.

In conclusion, Atena Marketplace insurance provides significant benefits, such as a broad provider network and strong preventive care, but its limitations, including higher premiums and restricted customization, warrant careful consideration. Prospective policyholders should evaluate their healthcare needs, budget, and long-term goals to determine if Atena coverage aligns with their priorities. Practical tips include comparing plans during open enrollment, leveraging telehealth services for minor ailments, and maximizing preventive care benefits to optimize the value of the coverage.

Qualifying for MassHealth: A Step-by-Step Guide to Eligibility

You may want to see also

Frequently asked questions

Atena Marketplace Insurance refers to health insurance plans offered through the Atena (or Anthem) network, often available via state or federal health insurance marketplaces. These plans comply with the Affordable Care Act (ACA) and provide essential health benefits.

Yes, Atena Marketplace Insurance covers pre-existing conditions. Under the ACA, all marketplace plans, including those from Atena, are required to provide coverage regardless of pre-existing health conditions.

You can enroll in Atena Marketplace Insurance during the annual Open Enrollment Period or during a Special Enrollment Period if you qualify due to a life event. Visit the Health Insurance Marketplace website or contact Atena directly to explore available plans and complete your enrollment.