Life insurance proceeds received as a beneficiary due to the death of the insured person are generally not included in gross income and do not need to be reported. However, any interest accrued on the life insurance payout is taxable and must be reported as interest received. The Affordable Care Act requires employers to report the cost of coverage under an employer-sponsored group health plan on Form W-2, specifically in Box 12 with Code DD. This reporting is for informational purposes and does not imply that the coverage is taxable. Additionally, if you are in a registered domestic partnership and your partner/children do not qualify as eligible dependents, the cost of their insurance coverage must be reported as imputed wages on your W-2, appearing in boxes 1, 3, and 5.

| Characteristics | Values |

|---|---|

| Life insurance proceeds received as a beneficiary | Not includable in gross income and do not need to be reported |

| Interest received from life insurance | Taxable and must be reported as interest received |

| Life insurance W-2 form | Lists benefits paid and taxes withheld |

| Reporting employer-sponsored health coverage | Reported in Box 12 of the Form W-2 with Code DD |

| Form 1095 | Indicates whether an individual had health coverage during the prior tax year |

Explore related products

What You'll Learn

![]()

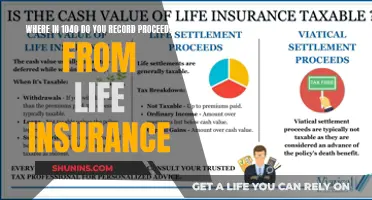

Life insurance proceeds are not taxable

Life insurance payouts are generally not subject to income taxes or estate taxes. However, there are certain exceptions. The type of policy, the size of the estate, and how the benefit is paid out can determine whether life insurance proceeds are taxed.

If you are the beneficiary of a life insurance policy and receive a payout due to the death of the insured, this money is typically not taxable. However, if you receive the benefit as an annuity (a series of payments over several years) instead of a lump sum, any interest accrued by the annuity account may be subject to taxes. This is because the interest accrued in the annuity account is considered taxable income.

If you own a whole life policy, you may owe income tax if you sell or surrender your policy or if you withdraw or borrow against your policy's cash value. If you surrender your policy and the surrender proceeds exceed the cumulative premiums, the excess may be subject to income taxes. Similarly, if you sell your policy to a third party and the sales proceeds exceed your cumulative premiums, minus the portion attributed to the cost of insurance, the excess may be subject to income taxes.

Additionally, if the life insurance policy does not have any named beneficiaries, the proceeds may be included in the deceased's estate. If the value of the estate exceeds the federal estate tax threshold (which was $13.61 million as of 2024), estate taxes must be paid on the amount over the limit. Some states also assess inheritance or estate taxes, depending on the estate's value and the deceased's residence.

It is important to consult a tax advisor about your specific situation to determine the taxability of life insurance proceeds.

Life Insurance Loans: How They Work and Why

You may want to see also

Explore related products

![]()

Report life insurance on Form 1040

Life insurance proceeds that you receive as a beneficiary due to the death of the insured person are typically not considered gross income and do not need to be reported. However, any interest accrued on the proceeds is taxable and must be reported as interest income. If the life insurance policy was transferred to you in exchange for cash or other valuable considerations, the exclusion for the proceeds is limited to the sum of the consideration paid, additional premiums paid, and certain other amounts. In such cases, you would generally use forms like 1099-INT or 1099-R to report the taxable amount.

Form 1040 is a standard federal income tax return form used by individuals to report their income and calculate the tax liability or refund due. While life insurance proceeds received as a beneficiary are generally not reported on Form 1040, there are a few scenarios where life insurance-related information may need to be disclosed on this form:

- Interest Income: If you receive any interest on a life insurance contract, you must report this interest as income on Form 1040. This interest is taxable, and you should include it in your total income calculations.

- Reportable Policy Sale: If you acquire a life insurance contract or any interest in a life insurance contract through a reportable policy sale, you may need to file Form 1099-LS. This form is related to the sale or exchange of life insurance policies and certain interests in life insurance policies. While Form 1099-LS itself is not filed with Form 1040, the information disclosed on it may have tax implications that need to be addressed on Form 1040.

- Premium Tax Credit: If you are claiming a Premium Tax Credit, you may need to file Form 1095, which is related to health insurance coverage. Individuals who wish to file for the Premium Tax Credit cannot use Form 1040 EZ and must instead file a traditional Form 1040 or 1040-A. Therefore, life insurance information may be relevant when claiming this credit on Form 1040.

- Domestic Partnership and Dependent Reporting: If you are in a registered domestic partnership and your partner/children do not qualify as eligible dependents under IRC 152, the cost of insurance provided for these dependents and your insurance contributions must be reported as "imputed wages" on your W-2. This information may then be relevant when completing Form 1040, as it affects your total income and tax liability.

In summary, while life insurance proceeds received as a beneficiary are generally not reported on Form 1040, there are specific scenarios where life insurance-related information may need to be disclosed or considered when filing this form. These scenarios include reporting interest income, reportable policy sales, claiming the Premium Tax Credit, and reporting domestic partnership insurance costs as "imputed wages."

Drug Use: Life Insurance Approval Impact

You may want to see also

Explore related products

![]()

Guardian Life Insurance W-2

A W-2 form is a document that lists the benefits paid and taxes withheld. It is required for every calendar year that you receive benefit payments. If you have a life insurance policy, your W-2 will come from the insurance company and will detail the benefits you have received and any taxes that have been withheld.

Guardian Life Insurance offers a range of insurance policies, including life insurance, and it appears that they also provide W-2 forms to their customers. According to one source, they will mail out a W-2 form by January 31 each year for the previous calendar year. However, it is important to note that the responsibility for producing the W-2 form may fall to either Guardian or your employer, depending on your policy. Therefore, it is recommended that you contact your employer to determine who will be sending your W-2 form.

In terms of where life insurance fits into the W-2 form, it is not entirely clear. However, it seems that life insurance benefits would be included as part of the "benefits paid" section of the W-2. This section would detail any payments made to you as part of your life insurance policy, such as disability claim payments, for example.

It is worth noting that there have been some issues with importing W-2 forms from Guardian Life Insurance into tax software like TurboTax. In some cases, users have had to manually enter the information from their W-2 forms, rather than importing them directly. This may be due to a compatibility issue with the control number provided on the form.

Finally, it is important to remember that the tax implications of life insurance can be complex, and they may vary depending on your specific circumstances and the type of policy you have. Therefore, it is always a good idea to consult with a tax professional or financial advisor to ensure that you are correctly reporting your life insurance benefits on your tax returns.

Securities Benefit Life Insurance: Financial Strength and Stability

You may want to see also

Explore related products

![]()

Employer-sponsored health coverage reporting

The Affordable Care Act (ACA) requires employers to report the cost of coverage under an employer-sponsored group health plan on an employee's Form W-2, Wage and Tax Statement. This information is reported in Box 12, using Code DD. The amount reported includes both the portion paid by the employer and the employee. However, it is important to note that this amount does not affect the employee's tax liability, as the employer contribution is excludable from the employee's income and is not taxable.

Employers can be eligible for transition relief for tax years, which is determined by the IRS. For example, transition relief was provided for the 2015 tax year and will continue for future calendar years until the IRS publishes new guidance. In such cases, employers are not required to issue a Form W-2 solely to report the value of healthcare coverage for retirees or other employees who would not typically receive a Form W-2.

If an individual is in a registered domestic partnership, and their partner and/or children do not qualify as eligible dependents under IRC 152, the cost of the insurance provided for these dependents and the insurance contributions made by the individual must be reported as "imputed wages" on their W-2, displayed in boxes 1, 3, and 5.

Additionally, individuals who are Graduate Appointee Insurance Plan participants will receive a 1095 form directly from Lifewise, indicating their health coverage for the prior tax year and listing any enrolled family members. This form is required for those filing for a Premium Tax Credit but is not necessary for filing taxes.

It is important to note that employer contributions are generally tax-deductible and free of payroll taxes, and employee expense reimbursements are income tax-free as long as they are covered by a health plan that provides minimum essential coverage (MEC).

Life Insurance: Is It Difficult to Secure Coverage?

You may want to see also

Explore related products

![]()

Taxable interest on life insurance

Life insurance proceeds received by a beneficiary due to the death of the insured person are generally not included in gross income and do not need to be reported. However, any interest income received from a life insurance policy is taxable and must be reported. This includes interest received from policy distributions (dividends, withdrawals, or partial surrenders) and interest charged on outstanding policy loans.

If the life insurance policy was purchased through an employer, the tax treatment may differ. The cost of employer-provided group-term life insurance on the life of an employee's spouse or dependent is generally not taxable to the employee if the coverage amount does not exceed $2,000. However, if the coverage exceeds this threshold, the employee may be subject to Social Security and Medicare tax on the cost of coverage over $50,000. Additionally, if the employer subsidizes the cost of the insurance or redistributes it between employees, the benefit received by the employees is taxable, even if the employees are paying the full cost.

In the context of taxable interest on life insurance, it is important to consider the tax consequences of policy loans. Interest is charged on any outstanding policy loan, and this interest is generally taxable to the policyowner. If a policy loan is taken, any gains up to the amount of the loan are recognized and may be taxable. Additionally, if a policy is gifted to someone else, such as a family member, and there is an outstanding loan with interest, the transaction may be treated as part-gift/part-sale, with the excess of the loan and interest over the policy's basis considered a taxable sale.

To report taxable interest income from a life insurance policy, individuals can use various tax forms, such as Form 1099-INT or Form 1099-R. They may also need to submit Form W-4S, Request for Federal Income Tax Withholding From Sick Pay, to the insurance company or make estimated tax payments by filing Form 1040-ES. It is important to consult the Internal Revenue Service (IRS) guidelines or a tax professional for specific instructions on reporting taxable interest on life insurance.

Life Insurance Simplified: All-Cause Coverage Explained

You may want to see also

Frequently asked questions

Generally, life insurance proceeds received as a beneficiary due to the death of the insured person are not included in gross income and do not need to be reported. However, any interest earned on the proceeds is taxable and should be reported.

If you need to report life insurance proceeds as income, you would include the amount received on line "Total amount from Form(s) W-2, box 1" on Form 1040, U.S. Individual Income Tax Return or Form 1040-SR, U.S. Tax Return for Seniors.

Under the Affordable Care Act, employers are required to report the cost of coverage under an employer-sponsored group health plan on the W-2 form. This reporting is for informational purposes and does not mean that the coverage is taxable.