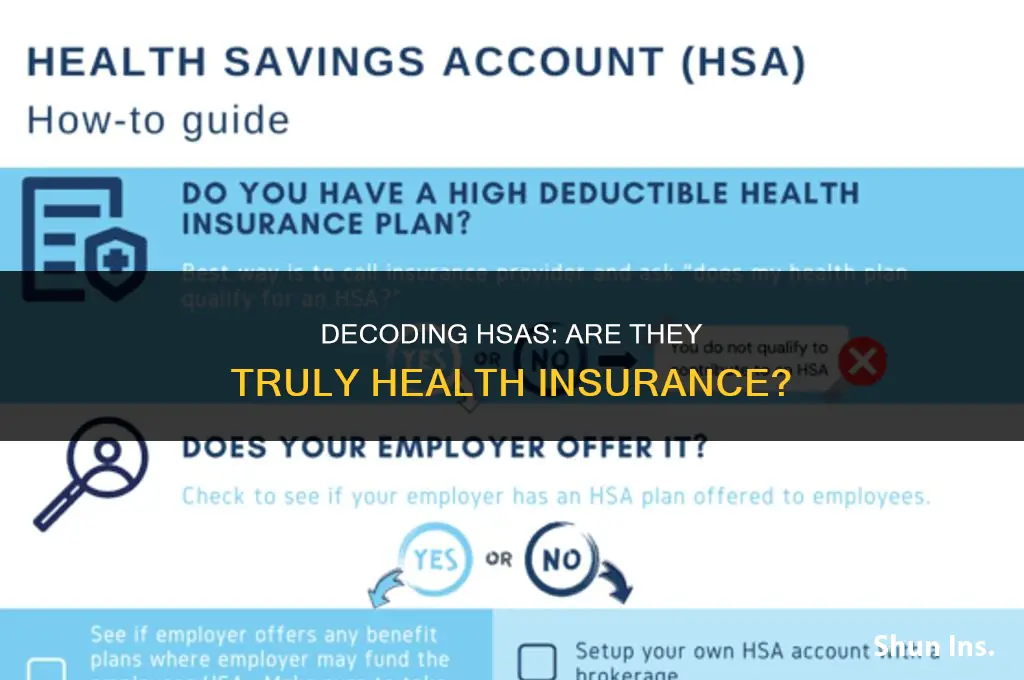

An HSA, or Health Savings Account, is a type of savings account that allows individuals to set aside money on a tax-advantaged basis to pay for qualified medical expenses. While an HSA is not traditional health insurance, it can be used in conjunction with a high-deductible health plan (HDHP) to help cover out-of-pocket healthcare costs. Contributions to an HSA are tax-deductible, and the funds can be invested and grow tax-free over time. When used for qualified medical expenses, withdrawals from an HSA are also tax-free. This makes an HSA a valuable tool for managing healthcare costs and saving for future medical needs.

Explore related products

What You'll Learn

- HSA Basics: An HSA is a savings account for health expenses, offering tax advantages

- Insurance Comparison: HSAs differ from traditional health insurance; they're supplemental and not primary coverage

- Eligibility: To have an HSA, you must be enrolled in a high-deductible health plan (HDHP)

- Tax Benefits: Contributions to an HSA are tax-deductible, and withdrawals for qualified expenses are tax-free

- Usage Flexibility: HSA funds can be used for a wide range of health-related expenses, including deductibles and copays

![]()

HSA Basics: An HSA is a savings account for health expenses, offering tax advantages

An HSA, or Health Savings Account, is a specialized savings account designed to help individuals set aside funds for qualified medical expenses. One of the primary benefits of an HSA is the tax advantages it offers. Contributions to an HSA are typically tax-deductible, and the earnings on the account grow tax-free. Additionally, withdrawals for qualified medical expenses are tax-free, making an HSA a powerful tool for managing healthcare costs.

To open an HSA, individuals must be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare. The IRS sets annual contribution limits for HSAs, which are adjusted for inflation. For example, in 2023, the contribution limit for individuals is $3,850, while the limit for families is $7,750. Those who are 55 or older can make additional "catch-up" contributions of up to $1,000 per year.

When using HSA funds, it's important to keep track of qualified medical expenses, as these are the only expenses that can be paid for with tax-free withdrawals. Qualified expenses include doctor visits, hospital stays, prescription medications, and many other healthcare costs. However, expenses such as health insurance premiums (with some exceptions), cosmetic procedures, and over-the-counter medications (unless prescribed) are generally not considered qualified expenses.

One of the key advantages of an HSA is its flexibility. Unlike other types of health savings accounts, such as FSAs (Flexible Spending Accounts), HSAs do not have a "use it or lose it" policy. This means that individuals can carry over unused funds from year to year, allowing the account to grow over time. Additionally, HSAs can be invested, similar to retirement accounts, which can help the funds grow even faster.

In summary, an HSA is a valuable financial tool for individuals looking to save on healthcare costs. By offering tax advantages, flexibility, and the ability to invest, HSAs can help individuals prepare for future medical expenses while also potentially building long-term wealth.

Understanding the Barriers: Why Many Remain Uninsured

You may want to see also

Explore related products

![]()

Insurance Comparison: HSAs differ from traditional health insurance; they're supplemental and not primary coverage

Health Savings Accounts (HSAs) are often misunderstood as a replacement for traditional health insurance, but they serve a distinct purpose. Unlike primary health insurance plans, which cover a wide range of medical expenses, HSAs are designed to be supplemental. They offer a tax-advantaged way to save money for qualified medical expenses, providing an additional layer of financial protection.

One key difference between HSAs and traditional health insurance is that HSAs are typically used in conjunction with a high-deductible health plan (HDHP). This means that the HSA holder is responsible for paying a higher portion of their medical costs out-of-pocket before their primary insurance coverage kicks in. In contrast, traditional health insurance plans often have lower deductibles and provide more immediate coverage for medical expenses.

HSAs also offer unique tax benefits that traditional health insurance plans do not. Contributions to an HSA are tax-deductible, and the funds grow tax-free as long as they are used for qualified medical expenses. This makes HSAs an attractive option for individuals looking to save money on their healthcare costs while also reducing their taxable income.

However, it's important to note that HSAs are not for everyone. They are best suited for individuals who are generally healthy and do not anticipate high medical expenses. For those with chronic conditions or who require frequent medical care, a traditional health insurance plan with lower out-of-pocket costs may be a better option.

In summary, while HSAs are a form of health insurance, they differ significantly from traditional health insurance plans. HSAs are supplemental, tax-advantaged savings accounts designed to be used in conjunction with a high-deductible health plan, offering a unique way to save for qualified medical expenses.

Cobra Health Insurance Coverage for Peniculectomy: What You Need to Know

You may want to see also

Explore related products

![]()

Eligibility: To have an HSA, you must be enrolled in a high-deductible health plan (HDHP)

To be eligible for a Health Savings Account (HSA), an individual must be enrolled in a high-deductible health plan (HDHP). This requirement is set by the Internal Revenue Service (IRS) and is a fundamental aspect of HSA eligibility. An HDHP is a type of health insurance plan that typically has lower premiums but higher deductibles compared to traditional health plans. This means that the policyholder is responsible for paying a larger portion of their healthcare costs out-of-pocket before the insurance coverage kicks in.

The IRS sets specific guidelines for what qualifies as an HDHP. For example, as of 2023, the minimum deductible for an individual to qualify for an HSA is $1,350, while the maximum out-of-pocket expense is $6,750. For families, the minimum deductible is $2,700, and the maximum out-of-pocket expense is $13,500. These figures are subject to change annually based on inflation adjustments.

It's important to note that not all health plans are eligible for HSA contributions. Plans that include co-pays for doctor visits or prescription drugs before meeting the deductible, or that do not meet the IRS's minimum deductible and maximum out-of-pocket expense requirements, do not qualify. Additionally, individuals who are enrolled in Medicare or who are claimed as dependents on someone else's tax return are not eligible for an HSA.

Enrolling in an HDHP and contributing to an HSA can offer several tax advantages. Contributions to an HSA are tax-deductible, and the funds can be used tax-free for qualified medical expenses. This can make an HSA a valuable tool for saving money on healthcare costs. However, it's crucial to understand the eligibility requirements and the specifics of the plan to ensure that an individual is making the most of this savings opportunity.

In summary, eligibility for an HSA is closely tied to enrollment in an HDHP. Understanding the IRS guidelines for what constitutes an HDHP, as well as the specific requirements and limitations of HSA eligibility, is essential for individuals looking to take advantage of the tax benefits and savings opportunities offered by these accounts.

Who Dominates the Medical Insurance Industry?

You may want to see also

Explore related products

![]()

Tax Benefits: Contributions to an HSA are tax-deductible, and withdrawals for qualified expenses are tax-free

Contributions to a Health Savings Account (HSA) offer significant tax advantages, making them an attractive option for those looking to save on healthcare costs. The funds you deposit into your HSA are tax-deductible, reducing your taxable income for the year. This deduction is available whether you itemize your deductions or take the standard deduction, providing a universal benefit to HSA contributors.

One of the key benefits of an HSA is the ability to withdraw funds tax-free for qualified medical expenses. This includes a wide range of healthcare costs, from doctor's visits and prescription medications to dental care and vision services. By using HSA funds for these expenses, you can avoid paying taxes on the money you withdraw, effectively lowering your overall healthcare costs.

To maximize the tax benefits of your HSA, it's important to understand the rules governing contributions and withdrawals. For example, you must be enrolled in a high-deductible health plan (HDHP) to contribute to an HSA, and you cannot be enrolled in Medicare. Additionally, there are annual contribution limits, which vary based on your age and whether you have family coverage.

When it comes to withdrawals, it's crucial to ensure that you're using the funds for qualified expenses. Non-qualified withdrawals are subject to income tax and may also incur a penalty. However, if you use the funds for eligible expenses, you can enjoy the full tax-free benefit of your HSA.

In summary, an HSA can be a powerful tool for managing healthcare costs, thanks to its tax-deductible contributions and tax-free withdrawals for qualified expenses. By understanding the rules and making the most of this savings vehicle, you can potentially save hundreds or even thousands of dollars on your healthcare expenses each year.

Does Aetna Offer Individual Health Insurance Plans? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Usage Flexibility: HSA funds can be used for a wide range of health-related expenses, including deductibles and copays

One of the key advantages of Health Savings Accounts (HSAs) is their usage flexibility. Unlike other health savings vehicles, HSA funds can be used for a broad spectrum of health-related expenses, providing account holders with significant leeway in managing their healthcare costs. This flexibility extends to covering deductibles and copays, which are often substantial out-of-pocket expenses for individuals and families. By allowing these funds to be applied towards such costs, HSAs can help mitigate the financial burden of healthcare, making it more accessible and affordable.

Moreover, the versatility of HSA funds goes beyond just deductibles and copays. Account holders can also use their HSA savings to pay for prescription medications, over-the-counter drugs, medical equipment, and even certain types of alternative care, such as acupuncture or chiropractic services. This wide range of eligible expenses means that HSA holders can tailor their healthcare spending to their specific needs and preferences, rather than being limited to a narrow set of approved costs.

Another significant benefit of HSA usage flexibility is the ability to save for future healthcare expenses. Unlike Flexible Spending Accounts (FSAs) or Health Reimbursement Arrangements (HRAs), which often have strict deadlines for using funds, HSAs allow account holders to carry over unused funds from year to year. This feature enables individuals to build up a substantial savings cushion for unexpected medical costs or to save for long-term care needs. Additionally, HSA funds can be invested, potentially growing the account balance over time and further enhancing the account holder's ability to manage healthcare expenses.

In conclusion, the usage flexibility of HSA funds is a critical component of their appeal. By allowing account holders to use their savings for a wide range of health-related expenses, including deductibles and copays, HSAs provide a valuable tool for managing healthcare costs. This flexibility, combined with the ability to save for future expenses and invest funds, makes HSAs a powerful financial instrument for individuals seeking to take control of their healthcare spending.

Does Health First Insurance Cover Therapy? A Comprehensive Guide

You may want to see also

Frequently asked questions

An HSA, or Health Savings Account, is not health insurance itself but rather a financial tool that can be used to pay for qualified medical expenses. It is typically paired with a high-deductible health plan (HDHP) and allows individuals to save money tax-free for healthcare costs.

An HSA works in conjunction with an HDHP by allowing individuals to contribute a portion of their income into the account tax-free. The funds in the HSA can then be used to pay for out-of-pocket medical expenses, such as deductibles, copays, and coinsurance, reducing the overall cost of healthcare.

The benefits of having an HSA include tax advantages, as contributions are tax-deductible and withdrawals for qualified medical expenses are tax-free. Additionally, HSAs offer flexibility, as the funds can be used for a wide range of medical expenses and can be carried over from year to year, unlike FSAs (Flexible Spending Accounts).

To be eligible for an HSA, an individual must be enrolled in an HDHP and not be enrolled in Medicare. Additionally, they cannot be claimed as a dependent on someone else's tax return. It's important to note that eligibility may vary based on specific circumstances and it's recommended to consult with a financial advisor or tax professional for personalized guidance.