In the US, insurance subsidies are generally not considered taxable income. For example, Obamacare subsidies are not considered income and are not taxed. Similarly, insurance claim income for an auto accident injury is typically not taxable and does not need to be included in your income. However, there may be specific circumstances where insurance-related payments may be subject to taxation. For instance, if you previously deducted insurance-related expenses from your taxes, any subsequent reimbursements might be considered taxable income. It's important to carefully review your specific situation and consult official sources or experts for accurate guidance on tax matters.

| Characteristics | Values |

|---|---|

| Are insurance subsidies considered taxable income? | No |

| What if I received insurance claim income for an injury? | Not taxable income unless reimbursed for lost income |

| What if I received insurance claim income for a car accident? | Not taxable income |

| What if I received insurance claim income for a home repair/replacement? | Not taxable income unless for an investment property |

| Are death benefits on a life insurance policy taxable income? | Not taxable income but may be subject to estate taxes depending on the policy amount, ownership, and state |

| Are dividends on a life insurance policy taxable income? | Considered a return of premiums paid and not taxable unless premiums were previously deducted from taxes |

| Are disability insurance benefits taxable income? | Depends on how premiums are paid; if paid with pretax income, benefits are taxable income, if paid with after-tax income, benefits are tax-free |

| Are long-term care insurance benefits taxable income? | Typically tax-free but may be taxed if premiums were deducted from taxes or if benefits exceed medical expenses |

| Is employer-sponsored health insurance for domestic partners taxable income? | Considered taxable income under federal law unless the domestic partner qualifies as a dependent |

Explore related products

What You'll Learn

![]()

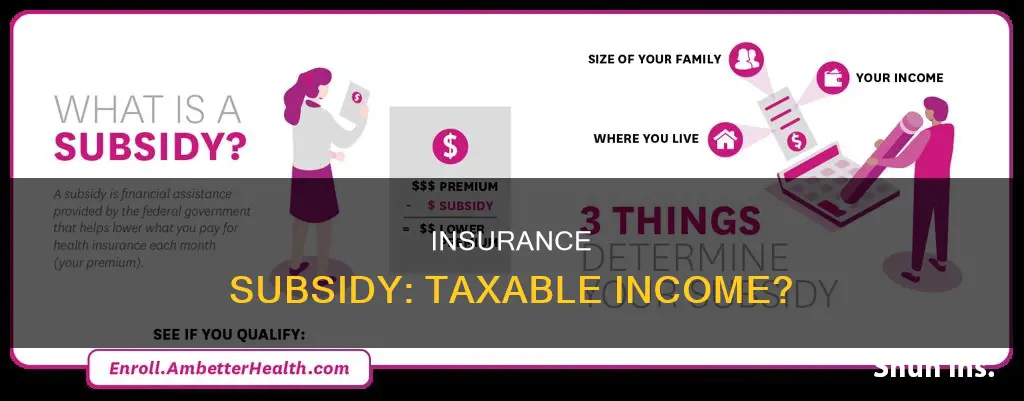

Obamacare subsidies are not taxed

Obamacare subsidies, also known as premium tax credits, are available to eligible individuals and families who purchase coverage through a health insurance marketplace. To be eligible, an individual must meet certain criteria, including having a household income that is at least equal to the Federal Poverty Level (FPL) and not having access to affordable coverage through an employer.

The premium tax credit reduces enrollees' monthly payments for insurance coverage, while the cost-sharing reduction (CSR) lowers deductibles and other out-of-pocket costs when enrollees seek medical care.

It is important to note that the amount of the Obamacare subsidy is based on an individual's estimated income for the year. If an individual's actual income for the year ends up being higher than anticipated, they may have to pay back a portion of the subsidy when filing their taxes. On the other hand, if their income is lower than expected, they may receive an additional subsidy.

Navigating Insurance Changes: A Smooth Transition Guide

You may want to see also

Explore related products

![]()

Insurance claim income for an auto-accident is not taxable

Insurance claim income for an auto accident is generally not taxable. However, there are certain situations in which you may have to include the reimbursement as income.

Insurance claim income is usually considered reimbursement for expenses rather than income. If there is nothing to indicate what the payment is for, it is likely meant to cover medical expenses and "pain and suffering". In this case, you don't need to include the amount in your income.

However, you may have to pay tax on insurance claim income if:

- You reported the resulting medical expenses as itemized deductions in a previous year.

- The funds were designated for something else, such as reimbursement for lost income.

- You receive compensation for future lost income.

- The settlement includes punitive damages.

- The settlement is for emotional distress resulting from a physical injury.

- You receive compensation for lost wages.

It is important to note that tax laws can vary by state, so it is always a good idea to consult a tax professional or a Certified Public Accountant (CPA) to determine your specific tax obligations.

Birthing Costs: Unraveling the Insurance Billing Process for New Mothers

You may want to see also

Explore related products

$79.2 $99

![]()

Insurance benefits are generally not taxable

However, there are some exceptions where insurance benefits are taxable. For example, if you deduct part of the cost of your car as a business expense, any insurance benefit you receive might be considered a gain and you will be taxed on the benefit if the insurance reimbursement is above the amount of your tax deduction.

Another exception is employer-sponsored health insurance for workers' domestic partners, which is considered taxable income under federal law. An employee must pay tax on what their partner's coverage costs the company, although some employers will increase the employee's salary to compensate for this. If a domestic partner qualifies as a dependent of the employee, then the health insurance coverage is tax-free. To qualify as a dependent, the partners must reside in the same household and one partner must provide over half of their support.

Understanding Rebating in Insurance: Unraveling the Practice and Its Implications

You may want to see also

Explore related products

![]()

Death benefits on a life insurance policy are not taxable income

Death benefits on a life insurance policy are not considered taxable income. However, there are some exceptions to this rule.

If the death benefit is paid out in installments, any interest that accrues on the benefit will be taxable. The interest generated is considered income and will need to be reported.

If the policyholder names an estate as the beneficiary, the estate may be subject to estate taxes. In 2024, the federal estate tax exemption limit is $13.61 million for an individual. This means that if the total taxable value of the estate's assets exceeds this amount, the IRS will levy an estate tax.

If the policy has three different people fulfilling the three roles of the insured, the policy owner, and the beneficiary, the death benefit may be subject to gift tax. In this case, the death benefit is considered a gift from the policy owner to the beneficiary.

Billing Aetna Insurance for Acupuncture Services: A Guide for Practitioners

You may want to see also

Explore related products

![]()

Dividends on insurance are not taxable

Dividends on insurance are generally not taxable, as they are considered a return of premium. However, there are a few exceptions to this rule.

Firstly, if the sum of dividends paid on a specific policy exceeds the sum of premiums paid, the excess amount may be subject to taxation as ordinary income. This is because any dividends that surpass the amount paid are considered income rather than a return of premium. For example, if you pay $1,000 in annual life insurance premiums and receive a $1,250 dividend, you may be required to pay taxes on the additional $250.

Secondly, if you earn interest on your dividends, this interest income may be taxable if it exceeds the amount of premiums you have paid.

It is important to note that these exceptions may vary depending on the specific circumstances and tax laws in your country or state. It is always recommended to consult with a tax professional or financial advisor to understand the tax implications of your insurance dividends.

In the context of health insurance, it is worth noting that subsidies, such as premium assistance tax credits and cost-sharing reductions, are generally not considered taxable income. However, if your income for the year exceeds what you projected when enrolling, you may need to repay some or all of the subsidy when filing your taxes.

Understanding Cobra Insurance Billing: The Arrears Conundrum

You may want to see also

Frequently asked questions

No, insurance subsidies are not considered taxable income.

No, you do not need to pay taxes on Obamacare subsidies.

Yes, you need to report your insurance subsidy on your tax return. If your income for the year was more than projected, you might have to pay back some or all of your subsidy.

Premium subsidies are advance premium tax credits (APTC) sent directly to your insurance company each month to offset your premium amount. Cost-sharing subsidies are benefits provided throughout the year and do not need to be repaid.

MAGI is the total income of all household members who are required to file a tax return. It is used by the Marketplace to determine eligibility for savings.