The cost of insurance varies depending on whether you are a homeowner or a landlord. Homeowners insurance provides dwelling coverage and includes personal property and personal liability protection. Landlord insurance, on the other hand, covers the structure and not the contents, and it is usually more expensive than homeowners insurance because landlords face different risks and have higher probabilities of legal action and tenant claims. However, dwelling insurance is commonly used to insure only the structure and is typically cheaper than homeowners insurance.

| Characteristics | Values |

|---|---|

| Cost of dwelling insurance | Typically more expensive than homeowners insurance |

| Cost of homeowners insurance | Cheaper than dwelling insurance |

| Reasons for difference in cost | Insurance companies receive more claims from rental properties than owner-occupied homes; landlords face different risks than homeowners; higher liability coverage for landlords |

| Factors affecting insurance cost | Location, type, and value of rental property; deductible amount; credit score |

| Discounts | Upgrades and updates to the property, such as a new roof or stormproof windows |

Explore related products

$16.95 $16.95

What You'll Learn

![]()

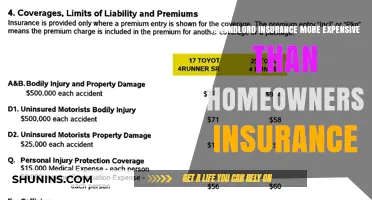

Landlord insurance costs more due to higher tenant risks and liability

Landlord insurance is more expensive than homeowners' insurance, with landlord policies typically costing about 25% more than a homeowners insurance policy for the same property. This is because tenants have less interest in preventive maintenance and reporting minor problems before they develop into issues that cause costly damage.

Landlord insurance provides similar fire and hazard protection for the dwelling and related structures. It can also include clauses to cover the landlord's personal property, liability, loss of income, legal fees, and various natural hazards, such as windstorms.

Homeowners' insurance provides protection for the dwelling, personal possessions, and other structures, such as a studio, garage, or fence. It also provides personal liability coverage should someone be injured or suffer damage to their property while on the premises. However, homeowners' insurance is designed for owner-occupied homes and does not cover the additional risks associated with renting out a property.

Landlords have different risks and, therefore, need different insurance. Landlord liability protection covers the property owner against financial loss if a tenant or visitor to the property is injured or suffers damage to their property, and the landlord is held legally responsible. For example, if someone is injured due to a failure of a porch railing, the landlord may be required to pay medical bills or legal fees. Although regular homeowners' policies include this protection, an insurance provider must account for a statistically higher probability of legal action against a landlord.

Uninsured Homes: What's the Risk?

You may want to see also

Explore related products

![]()

Homeowner's insurance covers personal property and liability

Homeowners insurance provides financial protection against loss due to disasters, theft and accidents. Most standard policies include four essential types of coverage: coverage for the structure of your home; coverage for your personal belongings; liability protection; and coverage for additional living expenses.

Personal property insurance is the part of a homeowners policy that pays to replace your belongings if they are stolen or destroyed. This includes everything from appliances, books, and music to cell phones, tablets, laptops, clothes, and shoes. Expensive items like jewellery, art, and collectibles are also covered, but there are usually dollar limits if they are stolen. To insure these items to their full value, purchase a special personal property endorsement or a floater and insure the item for its officially appraised value. Trees, plants, and shrubs are also covered under standard homeowners insurance, generally for about $500 per item.

The liability portion of a homeowners insurance policy pays for both the cost of defending you in court and any court awards—up to the limit stated in your policy documents. Liability limits generally start at about $100,000, but it is recommended to discuss purchasing a higher level of protection with your insurance professional. Your policy also provides no-fault medical coverage, so if a friend or neighbour is injured in your home, they can submit medical bills to your insurance company directly. This way, expenses can be paid without a liability claim being filed against you.

Homeowners insurance is designed to cover a residential property based on the typical hazards associated with an owner-occupied property. Landlord insurance, on the other hand, provides similar fire and hazard protection for the dwelling and related structures, but it also includes clauses to cover the landlord's personal property, liability, loss of income, legal fees, and various natural hazards. Coverage for a tenant-occupied dwelling typically costs more than homeowners coverage because insurance companies receive more claims from rental properties.

Farmers Insurance: Unraveling the Mystery of Gap Insurance

You may want to see also

Explore related products

![]()

Rental properties are more expensive to insure due to higher claim rates

Rental properties are more expensive to insure than owner-occupied homes due to higher claim rates. This is because tenants have less interest in preventive maintenance and reporting minor problems before they develop into more significant issues that result in costly damage.

Landlord insurance provides coverage for risks unique to rental properties, such as damage sustained while a guest or tenant is renting the property. It also includes liability protection, covering financial losses if a tenant or visitor is injured or suffers damage to their property, and the landlord is held legally responsible. The higher claim rates associated with rental properties lead to higher insurance costs.

Additionally, landlord insurance offers expanded liability protection, often with higher limits than standard home insurance policies. This increased liability coverage is another factor that contributes to the higher cost of insuring rental properties. Rental properties also tend to have higher claim amounts, further increasing the overall cost of insurance.

The cost of landlord insurance also depends on factors such as the location, type, and value of the rental property. For example, properties in areas prone to natural disasters or with a higher risk of flooding or earthquakes may require additional coverage, increasing the cost of insurance.

While landlord insurance is generally more expensive than homeowners' insurance, there are ways to reduce the cost. Landlords can consider their deductible, which is the portion of the claim that they pay. By choosing a higher deductible, landlords can often obtain lower premiums. Additionally, insurers may offer discounts for updates such as a new roof or storm-proof windows, which can help to offset the higher cost of insurance for rental properties.

Understanding Insurance Loss Run Reports: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Dwelling insurance is for vacant properties

Dwelling insurance is a type of coverage that is commonly used to insure only the structure of a building, also known as the 'dwelling'. This type of insurance is often referred to as 'Investment Property Insurance' or 'Second Home Insurance'. It is important to note that dwelling insurance does not cover personal property or personal liability protection, which are typically included in homeowners insurance.

If you have a vacant building that is not currently in use, or if you are trying to sell or renovate a property, you will need dwelling insurance. The insurance industry considers a property vacant if it is not used as a permanent residence. Since there is no full-time resident, vacant dwellings tend to cost more to insure and may be more challenging to obtain coverage for. However, a knowledgeable insurance agent can assist in finding suitable coverage for a vacant property.

Dwelling insurance is particularly relevant for landlords who rent out their properties and earn rental income. In this scenario, homeowners insurance is no longer applicable, and landlord insurance, a type of dwelling insurance, is required. Landlord insurance covers the structure of the building and provides protection against risks associated with renting, such as damage sustained by tenants. It can also include coverage for the landlord's personal property, liability, loss of income, legal fees, and natural hazards.

While landlord insurance typically costs more than homeowners insurance, the extra protection against the added risks of managing a rental property is well worth the difference in premiums. The cost of landlord insurance depends on factors such as property size, features, and the type and amount of coverage required. It is recommended to consult with an insurance specialist to determine the appropriate level of coverage and explore ways to reduce costs, such as discounts for upgrades or higher deductibles.

Reporting 1099 Income: Insurance Cash Value

You may want to see also

Explore related products

![]()

Landlord insurance covers the building, not contents

Landlord insurance is more expensive than homeowners' insurance. This is because insurance companies receive more claims from rental properties than from owner-occupied homes. The higher cost also reflects the increased liability coverage that landlord insurance provides. Landlord insurance policies are typically all-risk policies, covering all types of property damage except for those explicitly excluded by the policy. These exclusions often include preventable losses, such as neglect or intentional damage, as well as location-specific risks like earthquakes or floods.

While landlord insurance covers the building, it does not cover the contents of the rental property. Landlords who offer their properties as furnished need to be aware of this distinction. Landlords' insurance covers the structure of the building and any items used to maintain the property, such as a lawnmower or hedge trimmer. However, it does not cover the tenants' belongings. Tenants are responsible for obtaining their own insurance to protect their personal possessions.

In addition to covering the building, landlord insurance provides protection against a range of risks unique to rental properties. These include loss of income, legal fees, and natural hazards such as windstorms. Landlord insurance also offers liability protection, covering financial losses if a tenant or visitor is injured or suffers damage to their property while on the rental premises. This liability coverage also extends to legal costs if a tenant files a personal injury claim against the landlord.

The cost of landlord insurance varies depending on factors such as the location, type, and value of the rental property. It is recommended that landlords shop around and obtain quotes from multiple insurance providers to find the most suitable policy for their needs. Landlords should also be aware of potential discounts offered by insurers for upgrades to the property, such as a new roof or stormproof windows, which can help reduce overall costs.

TravelGuard Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Dwelling insurance is commonly used to insure only the structure of the home, whereas homeowners' insurance covers the dwelling and personal property and liability protection. Homeowners' insurance is typically cheaper than dwelling insurance.

Homeowners' insurance is for people residing in their property, whereas landlord insurance is for those renting out their property and earning rental income. Landlord insurance is more expensive than homeowners' insurance because landlords face different risks, such as damage caused by tenants.

Insurers often offer discounts for updates to the property, such as a new roof or stormproof windows. You can also consider your deductible—choosing a higher deductible can save you money on premiums.