Earthquake insurance is an optional coverage that homeowners can purchase to protect their homes and belongings from earthquake damage. While earthquakes are not common in Kansas, they have occurred in 39 states since 1900, and about 90% of Americans live in areas considered seismically active. Homeowners insurance typically excludes damage caused by earthquakes, and earthquake insurance can provide financial protection in the event of earthquake-related losses. The cost of earthquake insurance varies depending on location and the type of home, and it's recommended to consult an expert to evaluate your specific situation and determine the need for earthquake coverage.

| Characteristics | Values |

|---|---|

| Is earthquake insurance necessary for homeowners in Kansas? | Earthquake insurance is not necessary for homeowners in Kansas, but it can be inexpensive and is recommended. |

| What does earthquake insurance cover? | Earthquake insurance covers damage to your home and property caused by earthquakes, including landslides, mudslides, and damage to personal property. |

| What is not covered by earthquake insurance? | Earthquake insurance typically does not cover damage caused by floods and tidal waves, even when caused by an earthquake. It also may not cover landscaping, pools, fences, masonry, or separate buildings. |

| How much does earthquake insurance cost? | The cost of earthquake insurance varies depending on the risk level of the area. It can be inexpensive in lower-risk areas and more expensive in high-risk zones. |

| How do I determine my risk level for earthquakes? | You can refer to published seismic hazard maps and consult an expert to evaluate your specific situation. |

| What deductible must you pay for earthquake insurance? | Deductibles for earthquake insurance plans are typically between 5% and 15% of the policy limit, but can vary depending on the provider and your home's characteristics. |

| Where can I purchase earthquake insurance? | You can purchase earthquake insurance from your current home insurance provider as an endorsement or add-on to your existing policy. You can also buy a standalone earthquake insurance policy from specialized providers or independent organizations. |

Explore related products

What You'll Learn

- Earthquake insurance in Kansas can be inexpensive

- Earthquake damage is not covered by standard homeowner's insurance

- Earthquake insurance is available as an endorsement or separate policy

- The deductible for earthquake insurance is higher than standard homeowner's insurance

- Seismic hazard maps can help determine the risk of earthquakes in your area

![]()

Earthquake insurance in Kansas can be inexpensive

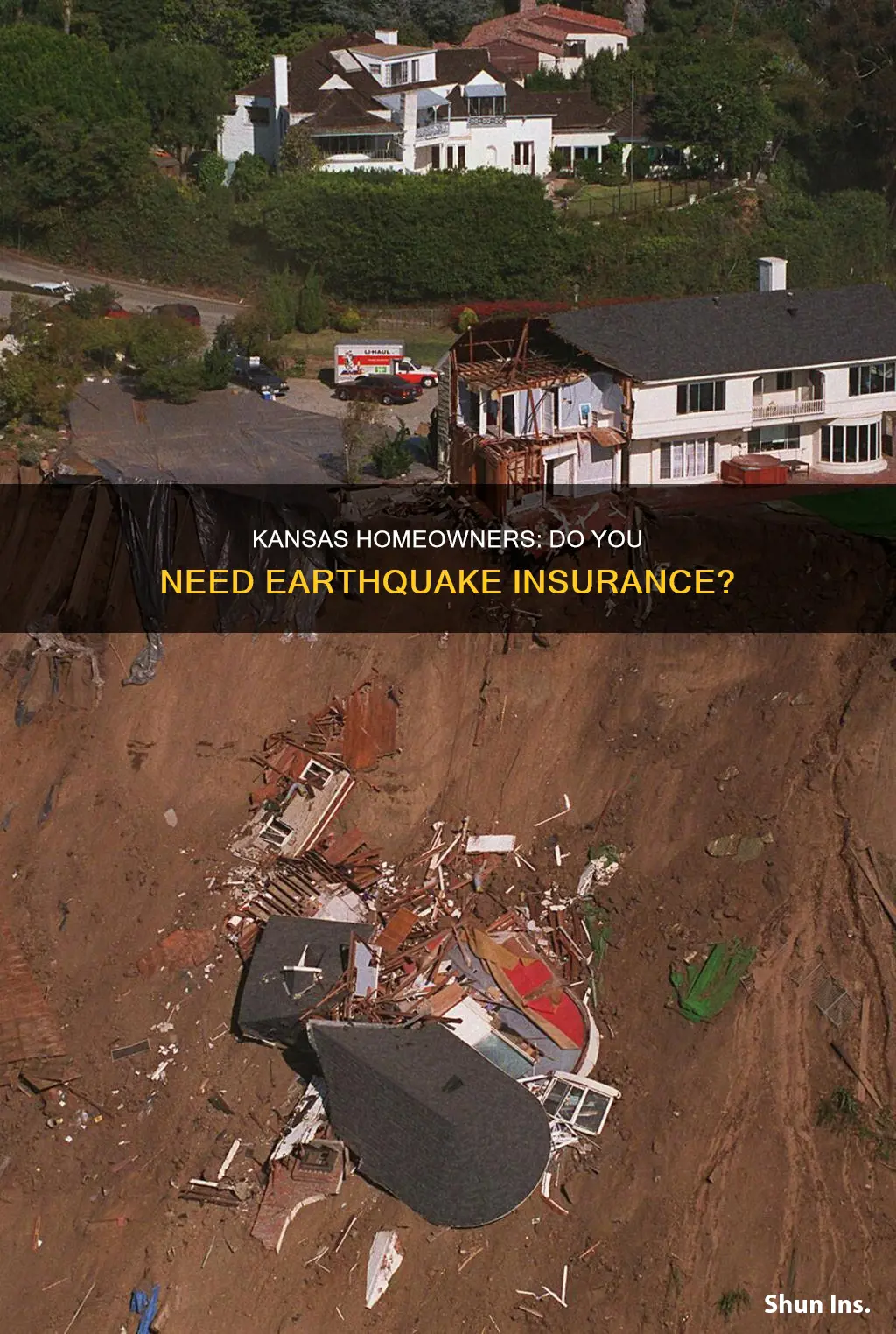

Earthquake insurance is a separate endorsement that you must buy and add to your homeowner or renters policy. It covers a range of damage caused by earth movement, including landslides, mudslides, and damage to the home and property. Standard homeowners insurance doesn't cover earthquake damage, so it's important to consider purchasing earthquake insurance if you live in an area prone to seismic activity.

While the cost of earthquake insurance varies depending on your location and the type of home you live in, for many customers in Kansas, earthquake insurance can be inexpensive. This is because Kansas is not typically considered a high-risk area for earthquakes. However, it's worth noting that earthquakes have occurred in 39 states since 1900, and about 90% of Americans live in areas considered seismically active.

When shopping for earthquake insurance in Kansas, it's important to consider your individual needs and risks. You may want to consult a seismic hazard map to understand the relative hazards in different areas. Additionally, you can ask the insurance company to help identify possible repairs and improvements that will make your home safer and minimize damage in the event of an earthquake. This could include securing water heaters, gas appliances, and other fixtures, as well as developing a family emergency plan.

Ultimately, the decision to purchase earthquake insurance in Kansas depends on your personal circumstances and risk tolerance. While it may not be a necessity for everyone, it can provide valuable peace of mind and financial protection in the event of an earthquake. Contacting local insurance agencies in Kansas, such as the Blue Valley Insurance Agency in Overland Park, can help you understand the costs and benefits of earthquake insurance for your specific situation.

Earth Movement: Is Your Home Covered?

You may want to see also

Explore related products

![Earthquake [Blu-ray]](https://m.media-amazon.com/images/I/81j73RxVEKL._AC_UY218_.jpg)

![]()

Earthquake damage is not covered by standard homeowner's insurance

Earthquake damage is not covered by standard homeowners insurance. This means that if an earthquake damages your home, you will have to pay for the repairs yourself unless you have purchased earthquake insurance.

Earthquake insurance is a type of coverage that protects your home and property from damage caused by earthquakes. It is available as an endorsement or a separate policy and is offered by most private insurers. In some states, such as California, earthquake insurance is provided by a dedicated entity like the California Earthquake Authority (CEA).

The cost of earthquake insurance varies depending on factors such as the location and type of home. It tends to be less expensive in areas with lower earthquake risk and can be relatively high in places prone to earthquakes. Earthquake insurance typically has a separate deductible, which can range from 5% to 25% of the policy limit.

When considering earthquake insurance, it is important to review the policy carefully as different companies may have varying inclusions and exclusions. For example, some policies may cover damages caused by landslides or mudslides, while others may exclude certain features like fences, pools, or landscaping.

In Kansas, earthquake insurance can be relatively inexpensive, and it is worth considering even if earthquakes are not common in the area. Standard homeowners insurance in Kansas does not typically cover earthquake damage, so purchasing earthquake insurance can provide valuable protection in the event of an earthquake.

Homeowners Insurance Deductibles: A Percentage of Your Property's Value?

You may want to see also

Explore related products

![Earthquake [DVD]](https://m.media-amazon.com/images/I/81MT0hUCk6L._AC_UY218_.jpg)

![]()

Earthquake insurance is available as an endorsement or separate policy

Earthquake insurance is not typically included in standard homeowners insurance policies. Homeowners will need to purchase earthquake coverage separately. This can be done by adding an endorsement to an existing policy or by purchasing a standalone earthquake policy.

An earthquake endorsement can be bought from most private insurers and added to your existing homeowner or renters policy. This endorsement generally covers damage or losses caused by earthquakes, landslides, mudslides, and other earth movements. However, it typically excludes damages caused by floods and tidal waves, even when compounded by an earthquake. It is important to carefully review the terms of the endorsement, as some policies may also exclude coverage for certain structures or items such as fences, pools, and landscaping.

Standalone earthquake insurance policies are also available from specialized providers, such as the California Earthquake Authority (CEA) or Palomar. These policies typically cover damage to the dwelling, other structures, and personal belongings. They may also include additional living expenses if the home is uninhabitable during repairs and loss assessments from associations. When purchasing a standalone policy, it is important to consider the deductible, which can range from 5% to 25% of the dwelling coverage limit.

The cost of earthquake insurance varies depending on the location and the level of risk. For those in Kansas, earthquake insurance can be inexpensive, but it is still important to shop around and compare rates to get the best value. It is recommended to contact a local insurance agency or a specialized provider to discuss specific needs and obtain a quote.

Overall, while earthquake insurance may not be a necessity for everyone, it is an important consideration for homeowners, especially in areas with a higher risk of seismic activity. By purchasing earthquake insurance, individuals can protect their homes and finances from the potentially catastrophic damage caused by earthquakes.

Reporting Insurance Forms: What, Why, and How?

You may want to see also

Explore related products

![]()

The deductible for earthquake insurance is higher than standard homeowner's insurance

Earthquake insurance is available in Kansas from providers such as Blue Valley Insurance Agency in Overland Park. Earthquake insurance is a separate endorsement that must be added to a standard homeowner's insurance policy, which does not typically cover earthquake damage.

The deductible for earthquake insurance is the amount the policyholder must pay before the insurance coverage begins. Earthquake insurance deductibles are typically higher than those for standard homeowner's insurance, ranging from 2.5% to 25% of the policy limit. The higher deductible for earthquake insurance is due to the potential for significant damage to a home's structure and belongings in an earthquake. Even relatively mild tremors can destroy furnishings and belongings, and stronger earthquakes can damage housing foundations and collapse walls.

The California Earthquake Authority (CEA) offers deductibles of 5%, 10%, 15%, 20%, and 25%. The deductible selected will impact the insurance premium, with higher deductibles leading to lower premiums. The CEA's basic earthquake coverage includes dwelling coverage, which covers the cost of repairing or rebuilding the home up to a certain limit, and personal property coverage, which covers belongings such as furniture, electronics, and other items in the home.

When considering earthquake insurance, it is important to assess your level of risk and the potential costs of repairing or rebuilding your home and replacing damaged belongings. While earthquake insurance can provide valuable protection, the high premiums and deductibles may make it challenging to balance the costs with the potential benefits.

Is USPS Insurance Worth the Cost?

You may want to see also

![]()

Seismic hazard maps can help determine the risk of earthquakes in your area

Earthquakes can cause a lot of damage to homes and belongings, and homeowners' insurance does not typically cover earthquake damage. Earthquake insurance is available as a separate policy or an endorsement from most private insurers. Even if you live in an area where earthquakes are uncommon, you may still need earthquake insurance. Earthquakes have occurred in 39 states since 1900, and about 90% of Americans live in areas considered seismically active.

The U.S. Geological Survey, in cooperation with FEMA and the Building Seismic Safety Council (BSSC), has developed a web-based seismic design application for building designers. This program can be used to obtain the earthquake ground motion parameters needed to design structures for specific geographic locations in accordance with the latest building code reference documents. The maps also help engineers build structures that can withstand earthquake shaking.

The NSHM maps are designed to improve earthquake-resilient construction in the United States. They can help people become more aware of earthquake hazards across the country. While a high earthquake hazard does not necessarily mean high risk, it is important to consider the potential impact on populated areas. Town A and Town B, for example, may have the same earthquake hazard, but if Town B has buildings built to withstand earthquake ground shaking, then its risk is lower.

If you are considering purchasing earthquake insurance, it is important to understand the coverage options and exclusions. Earthquake insurance can help pay for losses and damage to your home, belongings, and other buildings on your property. However, it typically does not cover damages or losses from floods and tidal waves, even when caused or compounded by an earthquake. It is also important to note that deductibles for earthquake insurance plans are generally higher than those in standard homeowners' insurance policies.

When Can You Sue Your Homeowner Insurance Company?

You may want to see also

Frequently asked questions

Earthquake insurance is not considered necessary in Kansas, and it can be inexpensive. However, earthquakes can happen anywhere, and some areas are experiencing more seismic activity due to oil drilling efforts. You may need an expert to evaluate your situation.

Earthquake insurance covers damage to your home and property caused by earthquakes, including landslides, mudslides, and sinkholes. It can also cover additional living expenses if your home is badly damaged and uninhabitable.

You can purchase earthquake insurance as an endorsement on your existing homeowner's insurance or as a separate, standalone policy. You may be able to get it from the same company that provides your home insurance, or from a specialist earthquake insurance provider or independent organisation.