Federal health insurance, such as Medicare and Medicaid, plays a crucial role in providing healthcare coverage to millions of Americans, particularly the elderly, low-income individuals, and those with disabilities. While these programs have been instrumental in ensuring access to medical care, there is ongoing debate about whether they are the best approach to healthcare. Proponents argue that federal health insurance offers comprehensive benefits, cost controls, and negotiating power with healthcare providers. However, critics contend that these programs can be bureaucratic, inefficient, and may not provide the same level of choice and flexibility as private insurance options. As the healthcare landscape continues to evolve, it is essential to examine the strengths and weaknesses of federal health insurance to determine if it remains the most effective solution for meeting the healthcare needs of the nation.

Explore related products

What You'll Learn

- Cost Comparison: Evaluate premiums, deductibles, and out-of-pocket costs against private insurance options

- Coverage Analysis: Examine the comprehensiveness of coverage, including pre-existing conditions and prescription drugs

- Provider Accessibility: Assess the availability and quality of healthcare providers within the federal insurance network

- Customer Satisfaction: Review beneficiary feedback on service quality, claims processing, and overall satisfaction

- Eligibility Criteria: Outline the requirements for qualifying for federal health insurance programs

![]()

Cost Comparison: Evaluate premiums, deductibles, and out-of-pocket costs against private insurance options

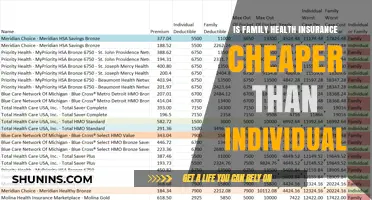

Federal health insurance, such as Medicare and Medicaid, often comes with lower premiums compared to private insurance options. However, it's essential to consider the full cost picture, including deductibles and out-of-pocket expenses. For instance, while Medicare Part A (hospital insurance) is typically premium-free for those who have worked and paid Medicare taxes for at least 10 years, Medicare Part B (medical insurance) requires a monthly premium. In 2023, the standard Part B premium is $164.90 per month.

Deductibles also play a significant role in the cost comparison. In 2023, the Medicare Part A deductible is $1,556 per benefit period, while the Part B deductible is $233 per year. Once these deductibles are met, Medicare covers 80% of approved medical expenses, leaving you responsible for the remaining 20%. This is where supplemental insurance plans, such as Medigap, can help cover these out-of-pocket costs.

Private insurance options, on the other hand, often come with higher premiums but may offer lower deductibles and out-of-pocket costs. For example, a private insurance plan might have a monthly premium of $300-$500 or more, depending on the plan and your age, health, and location. However, these plans might have lower deductibles, such as $500-$1,000 per year, and better coverage for prescription drugs and preventive care.

When comparing costs, it's also important to consider the network of providers. Federal health insurance plans typically have a larger network of providers, which can be an advantage if you live in a rural area or have specific healthcare needs. Private insurance plans, however, might have more restrictive networks, which could limit your choice of providers but potentially offer lower costs.

Ultimately, the best option for you will depend on your individual circumstances, including your age, health, income, and healthcare needs. It's essential to carefully evaluate the costs and benefits of both federal and private health insurance options to make an informed decision.

Decoding VA Health Insurance Taxes: What You Need to Know

You may want to see also

Explore related products

![]()

Coverage Analysis: Examine the comprehensiveness of coverage, including pre-existing conditions and prescription drugs

Federal health insurance, such as Medicare and Medicaid, provides extensive coverage for millions of Americans. However, understanding the comprehensiveness of this coverage is crucial for individuals seeking the best health insurance options. A thorough coverage analysis reveals that while federal health insurance programs generally offer robust benefits, there are nuances and limitations that must be considered.

One key aspect of coverage analysis is examining how pre-existing conditions are handled. Under the Affordable Care Act, federal health insurance programs are prohibited from denying coverage or charging higher premiums based on pre-existing conditions. This ensures that individuals with chronic illnesses or prior health issues can access affordable care. However, the specifics of how these conditions are covered can vary, and individuals must carefully review their plans to understand any potential gaps or limitations.

Prescription drug coverage is another critical component of federal health insurance. Medicare Part D and Medicaid both offer prescription drug benefits, but the formularies and cost-sharing structures can differ significantly. For example, Medicare Part D plans may have tiered formularies, where drugs are categorized based on cost, and beneficiaries may face higher out-of-pocket costs for drugs in higher tiers. In contrast, Medicaid typically covers a broader range of medications with lower cost-sharing, but there may be restrictions on certain drugs or requirements for prior authorization.

When conducting a coverage analysis, it's essential to consider the overall comprehensiveness of the plan, including preventive care, mental health services, and long-term care benefits. Federal health insurance programs generally provide strong coverage in these areas, but individuals should still review their specific plans to ensure that their needs are met. Additionally, understanding the provider networks and appeal processes can help individuals navigate any potential issues with their coverage.

In conclusion, while federal health insurance programs offer extensive coverage, a detailed analysis is necessary to fully understand the benefits and limitations of these plans. By examining how pre-existing conditions and prescription drugs are covered, as well as considering other aspects of the plans, individuals can make informed decisions about their health insurance options and ensure they have the best possible coverage for their needs.

Understanding AIDS Coverage: What Your Health Insurance May or May Not Include

You may want to see also

Explore related products

![]()

Provider Accessibility: Assess the availability and quality of healthcare providers within the federal insurance network

The availability and quality of healthcare providers within the federal insurance network are critical factors to consider when assessing whether federal health insurance is the best option for an individual. One key aspect to evaluate is the provider network's breadth and depth. Federal health insurance plans typically have extensive networks that include a wide range of healthcare providers, from primary care physicians to specialists. However, the quality of these providers can vary significantly.

To assess provider accessibility, it's essential to consider the following factors: the number of providers in the network, their geographic distribution, their specialties, and their credentials. Additionally, it's important to evaluate the ease of scheduling appointments, the average wait times, and the providers' communication styles. These factors can have a significant impact on an individual's overall healthcare experience and satisfaction with their insurance plan.

Another important consideration is the provider network's ability to meet the specific needs of the individual. For example, if an individual has a chronic condition or requires specialized care, it's crucial to ensure that the network includes providers who are experienced in treating that condition. Furthermore, individuals who prefer alternative or complementary medicine may want to ensure that the network includes providers who offer these services.

When evaluating provider accessibility, it's also important to consider the individual's personal preferences and priorities. Some individuals may prioritize convenience and accessibility, while others may be more concerned with the quality of care. By carefully assessing the provider network's availability and quality, individuals can make an informed decision about whether federal health insurance is the best option for their unique needs and preferences.

Covenant Trucking's Health Insurance: Coverage, Benefits, and Employee Options

You may want to see also

Explore related products

![]()

Customer Satisfaction: Review beneficiary feedback on service quality, claims processing, and overall satisfaction

Analyzing beneficiary feedback is crucial in determining the effectiveness of federal health insurance programs. Recent surveys indicate that while many beneficiaries are satisfied with the coverage provided, there are significant concerns regarding service quality and claims processing. For instance, a study by the Kaiser Family Foundation found that 40% of Medicare beneficiaries reported difficulties in getting timely appointments with healthcare providers. This highlights the need for improved provider networks and better coordination of care.

Claims processing is another area where beneficiaries have expressed dissatisfaction. Delays in processing claims can lead to financial strain for individuals who are already dealing with health issues. The Government Accountability Office (GAO) reported that in 2022, the average time to process a Medicare claim was 14 days, which is longer than the 10-day standard set by the Centers for Medicare & Medicaid Services (CMS). This underscores the importance of streamlining claims processing procedures and investing in technology to expedite these processes.

Overall satisfaction with federal health insurance programs is also influenced by the perceived value of the benefits provided. While many beneficiaries appreciate the comprehensive coverage, there is a growing concern about the affordability of premiums and out-of-pocket costs. A survey by AARP found that 56% of Medicare beneficiaries believe that their premiums are too high. This suggests that policymakers need to consider measures to reduce costs and improve the financial sustainability of these programs.

In conclusion, while federal health insurance programs have their strengths, there are clear areas for improvement based on beneficiary feedback. Addressing issues related to service quality, claims processing, and affordability will be essential in enhancing overall satisfaction and ensuring that these programs continue to meet the needs of their beneficiaries.

Understanding CHIP: Comprehensive Health Insurance for Children

You may want to see also

Explore related products

![]()

Eligibility Criteria: Outline the requirements for qualifying for federal health insurance programs

To qualify for federal health insurance programs, individuals must meet specific eligibility criteria. These criteria vary depending on the program, but generally include factors such as income level, age, disability status, and citizenship or immigration status. For example, Medicaid is available to low-income individuals and families, while Medicare is primarily for those aged 65 and older, as well as certain younger people with disabilities. The Children's Health Insurance Program (CHIP) provides coverage for children from families with moderate income who do not qualify for Medicaid. Understanding these eligibility requirements is crucial for determining whether federal health insurance is the best option for an individual or family.

The process of determining eligibility for federal health insurance programs involves several steps. First, individuals must gather necessary documentation, such as proof of income, age, and citizenship or immigration status. This documentation may include tax returns, pay stubs, birth certificates, and Social Security cards. Next, individuals must apply for the program, either online, by phone, or in person at a local office. The application process may require additional information, such as details about employment status, health conditions, and current health insurance coverage. Once the application is submitted, it will be reviewed by program administrators to determine eligibility based on the provided information and documentation.

One common mistake individuals make when applying for federal health insurance programs is failing to provide complete and accurate information. This can lead to delays in the application process or even denial of coverage. To avoid this, it is important to carefully review the application instructions and ensure that all required information and documentation are provided. Additionally, individuals should be aware of any changes to eligibility criteria or application processes, as these can occur periodically due to updates in program policies or regulations.

In conclusion, understanding the eligibility criteria for federal health insurance programs is essential for determining whether these programs are the best option for an individual or family. By carefully reviewing the requirements and providing complete and accurate information during the application process, individuals can increase their chances of qualifying for coverage and accessing the health care services they need.

Gateway Insurance and Medicaid: What's the Connection?

You may want to see also

Frequently asked questions

Federal health insurance, such as Medicare and Medicaid, is designed to provide coverage for specific groups, including seniors, low-income individuals, and people with disabilities. While it can be an excellent option for those who qualify, it may not be the best choice for everyone, particularly younger, healthier individuals who might find more affordable or comprehensive coverage through private insurers.

Federal health insurance programs like Medicare and Medicaid offer several advantages, including guaranteed coverage regardless of pre-existing conditions, lower out-of-pocket costs, and a wide network of healthcare providers. Additionally, these programs are federally funded, which can provide more stability and predictability in terms of coverage and costs.

While federal health insurance has its benefits, there are also some potential drawbacks. For example, Medicare and Medicaid may have limited coverage for certain services, such as dental and vision care, and may require beneficiaries to pay premiums or copays. Additionally, these programs can be complex to navigate, and beneficiaries may face challenges in finding providers who accept federal insurance.

Federal health insurance and private health insurance serve different purposes and cater to different populations. Federal insurance programs like Medicare and Medicaid are designed to provide coverage for vulnerable populations, such as seniors and low-income individuals, while private insurance is typically purchased by individuals or families through employers or insurance marketplaces. Private insurance may offer more flexibility in terms of coverage options and provider networks, but it can also be more expensive and may not provide the same level of guaranteed coverage as federal programs.