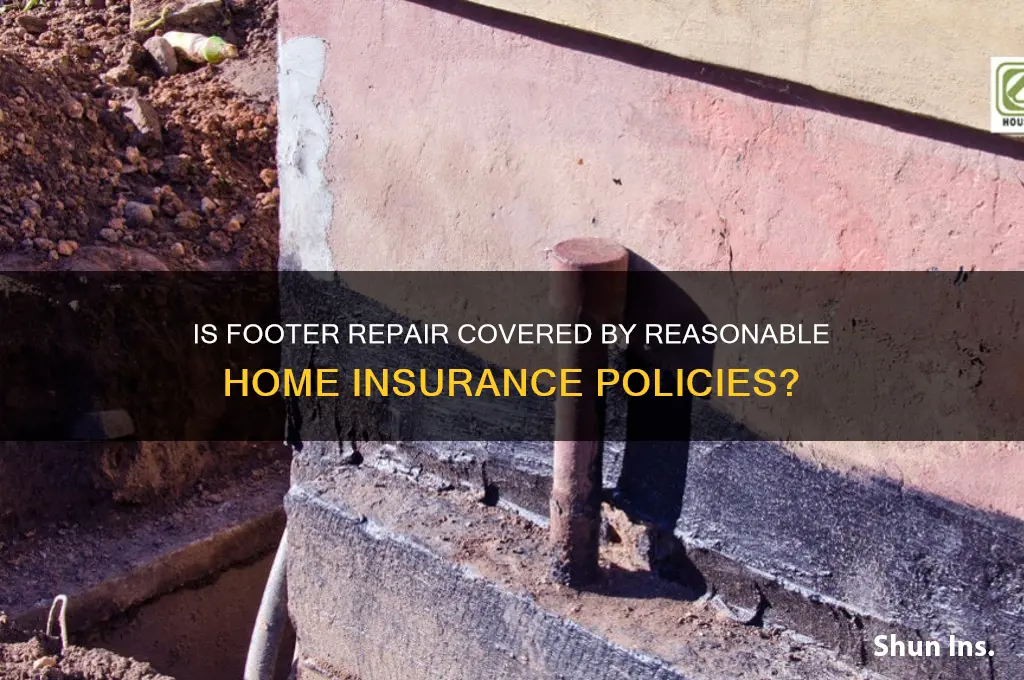

Footer repair can be a significant concern for homeowners, as damage to this structural component can compromise the integrity of an entire building. When considering whether footer repair is a reasonable claim under a repair insurance policy, it's essential to examine the specific terms and conditions of the coverage. Typically, insurance policies may cover footer repairs if the damage results from a covered peril, such as water damage from a burst pipe or ground movement due to a natural disaster. However, if the damage is attributed to normal wear and tear, poor maintenance, or pre-existing conditions, the insurance company may deny the claim. Homeowners should carefully review their policy details, including any exclusions or limitations, to determine if footer repair is indeed a reasonable and covered expense under their insurance plan.

Explore related products

What You'll Learn

- Footer damage causes (water, soil, age, pests, poor construction)

- Insurance coverage limits (policy terms, exclusions, deductibles, claim process)

- Repair cost estimates (materials, labor, extent of damage, contractor fees)

- Preventive measures (drainage, inspections, waterproofing, proper landscaping)

- Claim approval factors (documentation, policy compliance, damage severity, timely reporting)

![]()

Footer damage causes (water, soil, age, pests, poor construction)

Footer damage is a silent threat to any structure, often going unnoticed until it’s too late. Water is one of the primary culprits, seeping into cracks and eroding the foundation over time. Heavy rainfall, poor drainage, or plumbing leaks can saturate the soil around the footer, weakening its integrity. For instance, a single inch of rainfall on a 1,000-square-foot roof generates about 600 gallons of water—imagine that volume pooling around your foundation. To mitigate this, ensure gutters are clean, downspouts direct water at least 5 feet away from the foundation, and the ground slopes away from the house at a 5% grade.

Soil composition plays a critical role in footer damage, yet it’s often overlooked. Expansive soils, like clay, swell when wet and shrink when dry, creating pressure that can crack footers. In regions with high clay content, such as the Midwest and Southeast U.S., this is a common issue. A soil test can determine your soil type, and solutions like installing root barriers or using soil stabilization techniques can help. For example, mixing 5% lime into clay soil reduces its expansiveness by improving its structure.

Age is an inevitable factor in footer deterioration. Over decades, concrete naturally weakens due to carbonation, where CO2 reacts with cement, reducing its pH and structural strength. Footers in homes over 50 years old are particularly vulnerable. Regular inspections every 5–10 years can catch early signs of wear, such as hairline cracks or uneven floors. Reinforcing older footers with steel rebar or epoxy injections can extend their lifespan, but prevention through proper maintenance is always cheaper than repair.

Pests, though small, can cause significant damage. Termites and carpenter ants burrow into wood and soil, compromising the footer’s support system. In the U.S., termites alone cause over $5 billion in property damage annually. Signs of infestation include hollow-sounding wood, mud tubes, or discarded wings near windowsills. To prevent this, keep woodpiles away from the house, reduce moisture in crawl spaces, and schedule annual pest inspections. Treatments like liquid termiticides or bait stations can protect against infestations.

Poor construction is a preventable yet common cause of footer damage. Inadequate compaction of soil, insufficient steel reinforcement, or using low-quality concrete can lead to premature failure. For example, a footer poured in freezing temperatures may not cure properly, reducing its strength by up to 40%. Always hire licensed contractors and ensure they follow building codes, such as using a minimum of 2500 psi concrete for footers. Documenting the construction process with photos and material receipts can also help with insurance claims if issues arise later.

Understanding these causes empowers homeowners to take proactive steps, making footer repair a reasonable consideration for insurance coverage. While some damage is unavoidable, many risks can be minimized through preventative measures. Insurance policies that include foundation repair can save thousands in out-of-pocket costs, especially in regions prone to these risks. After all, a strong footer is the backbone of any structure—protecting it is an investment in your home’s longevity.

Term Life Insurance Simplified: Express Term Insurance Explained

You may want to see also

Explore related products

![]()

Insurance coverage limits (policy terms, exclusions, deductibles, claim process)

Understanding insurance coverage limits is crucial when considering whether footer repair qualifies as a reasonable claim. Policy terms often dictate the scope of coverage, and homeowners must scrutinize these details to avoid surprises. For instance, some policies explicitly cover foundation repairs, including footers, under dwelling coverage, while others may lump such repairs into broader categories like "structural damage." Always verify if your policy uses terms like "footers," "foundation," or "basement walls" to ensure clarity. Without this step, you risk assuming coverage that doesn’t exist, leaving you financially exposed when repairs are needed.

Exclusions are the silent deal-breakers in insurance policies, and footer repairs often fall into gray areas. Common exclusions include damage from gradual wear and tear, poor maintenance, or acts of nature like earthquakes or floods (unless specifically added as riders). For example, if a footer cracks due to soil erosion caused by improper drainage, the insurer might deny the claim, citing negligence. To navigate this, document maintenance efforts and consult with a structural engineer to establish the cause of damage. Proactive measures like these can strengthen your case and reduce the likelihood of a denied claim.

Deductibles play a pivotal role in determining whether pursuing a footer repair claim is financially prudent. High-deductible policies, often chosen to lower premiums, may render small to moderate footer repairs cost-ineffective. For instance, if your deductible is $2,500 and the repair estimate is $3,000, the out-of-pocket cost is nearly the same as paying outright. Conversely, low-deductible policies make filing a claim more appealing but come with higher premiums. Evaluate the potential repair cost against your deductible before deciding to file, and consider setting aside an emergency fund for such scenarios.

The claim process for footer repairs can be complex, requiring thorough documentation and patience. Start by notifying your insurer immediately after discovering the damage, as delays may void coverage. Insurers typically require detailed photos, repair estimates from licensed contractors, and sometimes a professional inspection report. Be prepared for an adjuster’s visit, during which they’ll assess the damage and determine coverage. Keep all communication records and follow up regularly to avoid delays. Understanding this process beforehand can streamline your experience and increase the chances of a successful claim.

Silver Sneakers: Humana's Fitness Program for Seniors

You may want to see also

Explore related products

![]()

Repair cost estimates (materials, labor, extent of damage, contractor fees)

Footer repair costs can vary widely, influenced by factors such as the extent of damage, materials required, labor intensity, and contractor fees. Understanding these components is crucial for homeowners considering whether footer repair is a reasonable claim under their insurance policy. For instance, minor cracks might only require epoxy injections, costing around $250 to $750, while severe structural damage could necessitate complete footer replacement, ranging from $5,000 to $15,000 or more. Insurance coverage often hinges on whether the damage is deemed sudden and accidental or the result of long-term neglect, making accurate cost estimates essential for policyholders.

Labor typically accounts for 40% to 60% of the total repair cost, depending on the complexity of the job and local wage rates. Skilled contractors charge anywhere from $50 to $150 per hour, with specialized foundation repair experts often on the higher end. For example, excavating and replacing a section of footer requires heavy machinery, precise engineering, and meticulous backfilling, driving up labor costs. Homeowners should obtain multiple quotes to ensure competitive pricing, but beware of unusually low bids, which may indicate subpar materials or workmanship.

The extent of damage directly impacts material costs, which can range from affordable concrete mixes to high-end waterproofing compounds. A simple repair might involve hydraulic cement at $10 to $20 per bag, while extensive work could require steel reinforcement bars ($0.50 to $2 per linear foot) or advanced drainage systems ($1,000 to $4,000). Contractors often add a markup of 10% to 20% on materials, so requesting a detailed breakdown of material and labor costs can help homeowners assess the fairness of the estimate.

Contractor fees vary based on experience, location, and the scope of the project. Flat fees for inspections and estimates are common, typically ranging from $200 to $500, while larger projects may include a project management fee of 5% to 10% of the total cost. Homeowners should verify a contractor’s licensing, insurance, and references to avoid scams or poor-quality work. Additionally, some contractors offer warranties on their repairs, which can add value but also increase the overall cost.

Finally, homeowners should consider hidden costs that can arise during footer repairs. For example, unforeseen issues like soil instability or underground utilities may require additional work, inflating the budget. Permits, which can cost $100 to $500 depending on the locality, are often necessary for structural repairs. By factoring in these variables and securing a comprehensive estimate, homeowners can make informed decisions about whether footer repair is a reasonable expense to cover under insurance or out of pocket.

Insurance's Grip: How Profit-Driven Policies Destroyed Healthcare Accessibility

You may want to see also

Explore related products

![]()

Preventive measures (drainage, inspections, waterproofing, proper landscaping)

Footer repair can be a costly and disruptive process, but many issues can be prevented with proactive measures. One of the most critical aspects of foundation maintenance is effective drainage. Poor drainage is a leading cause of foundation problems, as water accumulation around the base of a structure can lead to soil erosion, hydrostatic pressure, and moisture infiltration. To combat this, homeowners should ensure that their properties have a well-designed drainage system. This includes installing gutters and downspouts to direct rainwater away from the foundation, grading the landscape to slope away from the house, and considering the use of French drains or perimeter drains in areas with high water tables or heavy rainfall.

Regular inspections are another vital preventive measure. Foundation issues often develop gradually, and early detection can save homeowners from extensive and expensive repairs. It is recommended that homeowners conduct visual inspections at least twice a year, looking for signs of cracking, shifting, or moisture intrusion. Additionally, hiring a professional inspector every 3-5 years can provide a more comprehensive assessment, as they have the expertise to identify subtle issues and potential problem areas. These inspections should include a thorough examination of the foundation, basement, or crawl space, as well as the surrounding soil and drainage systems.

Waterproofing is a powerful tool in the fight against foundation damage. By creating a barrier against moisture, waterproofing treatments can prevent water from seeping into the foundation and causing cracks, mold, or structural deterioration. There are various waterproofing methods available, such as exterior waterproofing membranes, interior sealants, and drainage systems like sump pumps. For instance, applying a silicone-based sealant to the exterior foundation walls can provide a flexible and durable barrier against water infiltration. It's essential to choose the right waterproofing solution based on the specific needs of the property, considering factors like climate, soil type, and the extent of water exposure.

Landscaping plays a significant role in foundation health, often overlooked by homeowners. The strategic placement of plants, trees, and shrubs can either support or undermine the stability of a foundation. Large trees, for example, should be planted at a safe distance from the house, as their roots can extend far and wide, potentially causing soil displacement and foundation movement. Instead, opt for smaller, shallow-rooted plants closer to the structure. Regularly trimming and maintaining vegetation is also crucial to prevent roots from growing into drainage systems or causing soil erosion. Proper landscaping not only enhances the aesthetic appeal of a property but also contributes to the long-term integrity of its foundation.

In summary, implementing preventive measures is a wise strategy for homeowners to protect their foundations and avoid the need for extensive footer repairs. By focusing on drainage, regular inspections, waterproofing, and thoughtful landscaping, potential issues can be mitigated or even eliminated. These proactive steps not only save money in the long run but also provide peace of mind, ensuring the structural stability and safety of one's home. While insurance may cover certain foundation repairs, taking preventive action is a more cost-effective and less stressful approach to maintaining a healthy and durable foundation.

Expired Insurance Calculation Guide: Steps to Determine Your Policy's End Date

You may want to see also

Explore related products

![]()

Claim approval factors (documentation, policy compliance, damage severity, timely reporting)

Footer repair claims under insurance policies often hinge on meticulous documentation. Insurers require detailed records of the damage, including photographs, repair estimates, and, in some cases, professional assessments. For instance, if a homeowner notices cracks in the foundation, they should document the issue with timestamped photos and obtain at least two repair quotes from licensed contractors. Inadequate documentation can lead to claim denial, as insurers need concrete evidence to verify the extent and cause of the damage. A well-organized file, including maintenance records and previous inspections, can significantly strengthen a claim, demonstrating due diligence on the homeowner’s part.

Policy compliance is another critical factor in claim approval. Homeowners must ensure their actions align with the terms and conditions of their insurance policy. For example, some policies require regular maintenance of the property to prevent damage. If a footer issue arises due to neglect, such as failing to address water drainage problems, the insurer may deny the claim. It’s essential to review the policy annually and understand exclusions, such as damage from natural disasters or pre-existing conditions. Compliance also extends to using approved contractors for repairs, as some insurers mandate this to ensure quality work.

The severity of the damage plays a pivotal role in determining claim approval. Minor cracks or cosmetic issues may not qualify for coverage, as insurers typically assess whether the damage affects the structural integrity of the property. For instance, a small hairline crack might be deemed non-critical, while a significant shift in the foundation could warrant immediate attention. Insurers often use standardized severity scales to evaluate claims, with higher severity levels increasing the likelihood of approval. Homeowners should be prepared to provide evidence that the damage poses a substantial risk to the property’s stability.

Timely reporting is perhaps the most overlooked yet crucial factor in claim approval. Delays in reporting footer damage can lead to complications, as insurers may argue that the issue worsened due to inaction. For example, a homeowner who waits six months to report foundation cracks might face scrutiny, as the damage could have been mitigated earlier. Most policies require claims to be filed "as soon as reasonably possible" after discovering the issue. Practical tips include setting reminders for regular property inspections and keeping a log of any concerns, ensuring prompt action when problems arise. Quick reporting not only improves the chances of approval but also demonstrates responsibility, which insurers value.

Mercari Packages: Are They Insured?

You may want to see also

Frequently asked questions

Footer repair is typically not covered under standard home insurance policies unless the damage is caused by a covered peril, such as a sudden and accidental event like a flood or earthquake, and if the policy explicitly includes foundation or structural damage.

Factors include the cause of damage (e.g., natural disaster vs. wear and tear), the terms of your policy, whether the damage is sudden and accidental, and if the policy covers foundation or structural repairs.

Yes, some insurers offer endorsements or add-ons for foundation or structural damage, including footer repairs. Check with your provider to see if such coverage is available and if it aligns with your needs.