The question of whether health insurance penalties are calculated based on gross or net income is a crucial aspect of understanding the financial implications of the Affordable Care Act (ACA). This topic delves into the specifics of how the penalty for not having health insurance is determined, which can significantly impact an individual's tax liability. The ACA mandates that individuals must have health insurance or pay a penalty, with the amount of the penalty being linked to their income. However, the exact method of calculating this penalty—whether it's based on gross income before deductions or net income after taxes and other deductions—can be a point of confusion for many. Understanding this distinction is essential for accurate tax planning and compliance with healthcare regulations.

Explore related products

$0.99

What You'll Learn

- Understanding Health Insurance Penalties: Explanation of how penalties are calculated based on income

- Gross vs. Net Income: Differences between gross and net income and their impact on penalty calculations

- Affordable Care Act (ACA) Penalties: Specific penalties under the ACA for not having health insurance

- Exemptions and Waivers: Circumstances under which individuals may be exempt from health insurance penalties

- Impact on Tax Returns: How health insurance penalties are reported and paid through tax returns

![]()

Understanding Health Insurance Penalties: Explanation of how penalties are calculated based on income

The calculation of health insurance penalties is intricately linked to an individual's income. Specifically, the penalty for not having health insurance, as mandated by the Affordable Care Act (ACA), is determined based on a percentage of one's adjusted gross income (AGI). The AGI is a measure of taxable income calculated after certain deductions and adjustments are made to the gross income.

To understand how the penalty is calculated, it's essential to first determine the AGI. This figure is derived from the gross income by subtracting specific deductions such as alimony payments, student loan interest, and certain business expenses. Once the AGI is established, the penalty is calculated as a percentage of this amount. For instance, as of the cutoff date in June 2024, the penalty is 2.5% of the AGI for individuals who do not have health insurance coverage.

It's important to note that the penalty is not a flat rate but rather a percentage, which means it increases as the AGI increases. This progressive approach ensures that the penalty is more substantial for higher-income individuals who can more easily afford health insurance. The penalty is capped at the cost of the average premium for a bronze plan in the health insurance marketplace.

Furthermore, the penalty is prorated based on the number of months an individual is without health insurance coverage. If someone is uninsured for only part of the year, the penalty is calculated based on the proportion of the year they were without coverage. This prorated approach provides some flexibility and acknowledges that circumstances can change throughout the year.

In summary, the health insurance penalty is calculated as a percentage of an individual's adjusted gross income, with the specific percentage and cap determined by the ACA. The penalty is prorated for partial years of coverage, and the AGI is calculated after certain deductions and adjustments are made to the gross income. Understanding these details is crucial for individuals to accurately assess their potential penalty and make informed decisions about health insurance coverage.

Understanding Health Insurance: Key Factors That Influence Your Coverage and Costs

You may want to see also

Explore related products

![]()

Gross vs. Net Income: Differences between gross and net income and their impact on penalty calculations

Understanding the distinction between gross and net income is crucial when determining the penalty for not having health insurance. Gross income refers to the total amount of money earned before any deductions or taxes are taken out. This includes wages, salaries, tips, bonuses, and any other form of compensation. On the other hand, net income is the amount of money left after all deductions, such as taxes, social security, and Medicare, have been subtracted from the gross income.

The Affordable Care Act (ACA) uses the modified adjusted gross income (MAGI) to determine eligibility for subsidies and penalties. MAGI is calculated by taking the gross income and subtracting certain deductions, such as the standard deduction and personal exemptions. This means that the penalty for not having health insurance is based on the gross income, not the net income.

The penalty for not having health insurance is calculated as a percentage of the MAGI. For example, in 2020, the penalty was 10% of the MAGI. This penalty is capped at the cost of the average bronze plan in the area. It's important to note that the penalty is assessed on a month-by-month basis, so if an individual goes without health insurance for only part of the year, the penalty will be prorated accordingly.

One common misconception is that the penalty is based on net income, which can lead to confusion when calculating the penalty. For instance, if an individual has a high gross income but a low net income due to significant deductions, they may be surprised to find that the penalty is based on their gross income. This highlights the importance of understanding the difference between gross and net income when it comes to health insurance penalties.

In conclusion, the penalty for not having health insurance is based on the gross income, specifically the MAGI. This means that individuals need to be aware of their gross income when determining their potential penalty for not having health insurance. Understanding the difference between gross and net income can help individuals make informed decisions about their health insurance coverage and avoid unexpected penalties.

Health Insurance and Taxes: What You Need to Know

You may want to see also

Explore related products

![]()

Affordable Care Act (ACA) Penalties: Specific penalties under the ACA for not having health insurance

The Affordable Care Act (ACA) introduced several penalties for individuals who do not maintain health insurance coverage. One of the primary penalties is the individual shared responsibility payment, which is calculated based on a percentage of the individual's household income. Specifically, the penalty is determined using the gross income of the individual and their dependents. This means that the total income earned before any deductions or taxes are applied is used to calculate the penalty amount.

For example, if an individual's gross income is $50,000 and they do not have health insurance, they would be subject to a penalty. The penalty amount is calculated as a percentage of their gross income, which can add up significantly. It's important to note that this penalty is designed to encourage individuals to obtain health insurance coverage and is separate from any other taxes or fees associated with the ACA.

In addition to the individual shared responsibility payment, there are other penalties under the ACA for not having health insurance. For instance, there is a penalty for employers who do not offer health insurance coverage to their full-time employees. This penalty is also calculated based on the employer's gross income and the number of full-time employees they have.

It's crucial for individuals and employers to understand these penalties and how they are calculated to avoid any unexpected financial burdens. By maintaining health insurance coverage, individuals can not only avoid these penalties but also ensure they have access to necessary medical care. Employers who offer health insurance can also avoid penalties and provide a valuable benefit to their employees.

In summary, the ACA penalties for not having health insurance are based on gross income, and it's essential for individuals and employers to be aware of these penalties to make informed decisions about health insurance coverage.

Understanding Co-Payment Clauses in Health Insurance Policies

You may want to see also

Explore related products

![]()

Exemptions and Waivers: Circumstances under which individuals may be exempt from health insurance penalties

Individuals may be exempt from health insurance penalties under certain circumstances. These exemptions are designed to accommodate situations where obtaining health insurance is not feasible or necessary. For instance, individuals who are incarcerated are exempt from the penalty, as they are unable to purchase health insurance while in prison. Similarly, individuals who are members of a recognized religious sect that opposes health insurance may also be exempt, provided they meet specific criteria.

Another exemption applies to individuals who experience a short coverage gap of less than three months. This exemption is intended to prevent individuals from being penalized for brief periods without insurance, such as when transitioning between jobs or insurance plans. Additionally, individuals who are eligible for Medicaid but have not yet enrolled may be exempt from the penalty, as they are considered to have coverage once they enroll.

The process for claiming an exemption varies depending on the specific circumstance. In some cases, individuals may need to provide documentation or proof of their exemption status. For example, individuals claiming a religious exemption may need to provide a letter from their religious leader confirming their membership and opposition to health insurance. In other cases, such as for individuals who are incarcerated, the exemption may be automatically applied based on their status.

It is important to note that exemptions are not the same as waivers. Waivers are temporary suspensions of the penalty, often granted on a case-by-case basis due to exceptional circumstances. Exemptions, on the other hand, are permanent and apply to specific categories of individuals. Understanding the difference between exemptions and waivers can help individuals navigate the complexities of health insurance penalties and ensure they are not unfairly penalized.

Did Health Insurance Cover Jazz's Surgery? Unraveling the Facts

You may want to see also

Explore related products

![]()

Impact on Tax Returns: How health insurance penalties are reported and paid through tax returns

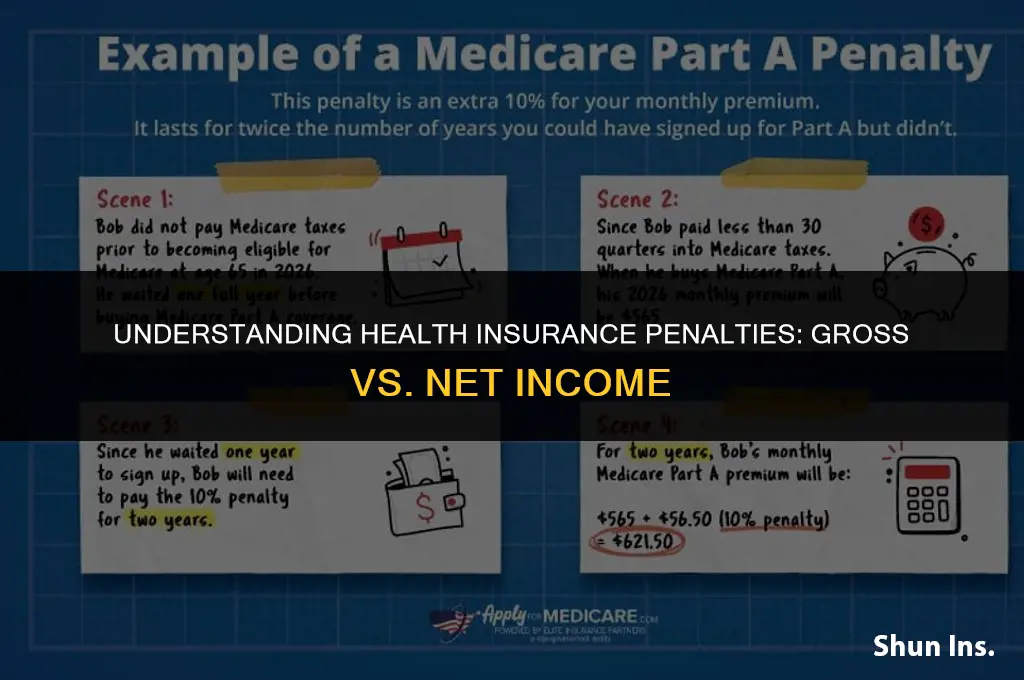

The impact of health insurance penalties on tax returns is a critical aspect of understanding the Affordable Care Act (ACA). Taxpayers are required to report their health insurance status on their federal tax returns, and those who fail to maintain minimum essential coverage may be subject to a penalty. This penalty is calculated based on the number of months without coverage and is reported on Form 1040. The penalty amount is added to the taxpayer's total tax liability for the year.

One common misconception is that the health insurance penalty is based on gross income. However, this is not the case. The penalty is actually calculated as a percentage of the taxpayer's adjusted gross income (AGI). AGI is the taxpayer's gross income minus certain deductions, such as the standard deduction or itemized deductions. This means that the penalty amount will vary depending on the taxpayer's AGI, and it is important to understand how this calculation works to accurately estimate the potential penalty.

To report the health insurance penalty, taxpayers must file Form 1040 with the IRS. On this form, they will need to provide information about their health insurance coverage, including the months they were covered and the months they were not. They will also need to calculate the penalty amount using the IRS's instructions and add it to their total tax liability. It is important to note that the penalty is not tax-deductible, so taxpayers cannot reduce their tax liability by claiming it as a deduction.

In addition to the federal penalty, some states have their own health insurance penalties. These state penalties may be calculated differently and reported on state tax returns. Taxpayers should check with their state's tax department to understand the specific requirements and penalties for their state.

To avoid the health insurance penalty, taxpayers should ensure they maintain minimum essential coverage throughout the year. This can include employer-sponsored health insurance, individual health insurance purchased through a health insurance exchange, or coverage through a government program such as Medicaid or Medicare. Taxpayers who experience a gap in coverage should consider purchasing short-term health insurance or exploring other coverage options to minimize their potential penalty.

In conclusion, understanding the impact of health insurance penalties on tax returns is essential for taxpayers to comply with the ACA and avoid unnecessary financial burdens. By maintaining minimum essential coverage and accurately reporting their health insurance status on their tax returns, taxpayers can minimize their potential penalty and ensure they are in good standing with the IRS.

Florida Insurance Cancellations: Which Companies Are Dropping Policies?

You may want to see also

Frequently asked questions

The health insurance penalty, also known as the individual mandate penalty, is calculated based on your gross income.

The penalty amount is determined as a percentage of your gross income, or a flat fee per person, whichever is greater. The percentage and flat fee amounts are set by the government and can change over time.

The purpose of the health insurance penalty is to encourage individuals to maintain health insurance coverage. This helps to ensure that everyone contributes to the healthcare system and can access necessary medical care.

Yes, there are several exemptions to the health insurance penalty. These include financial hardship, religious conscience, membership in a health care sharing ministry, and certain other circumstances. If you believe you may qualify for an exemption, you should consult with a tax professional or contact the relevant government agency for more information.