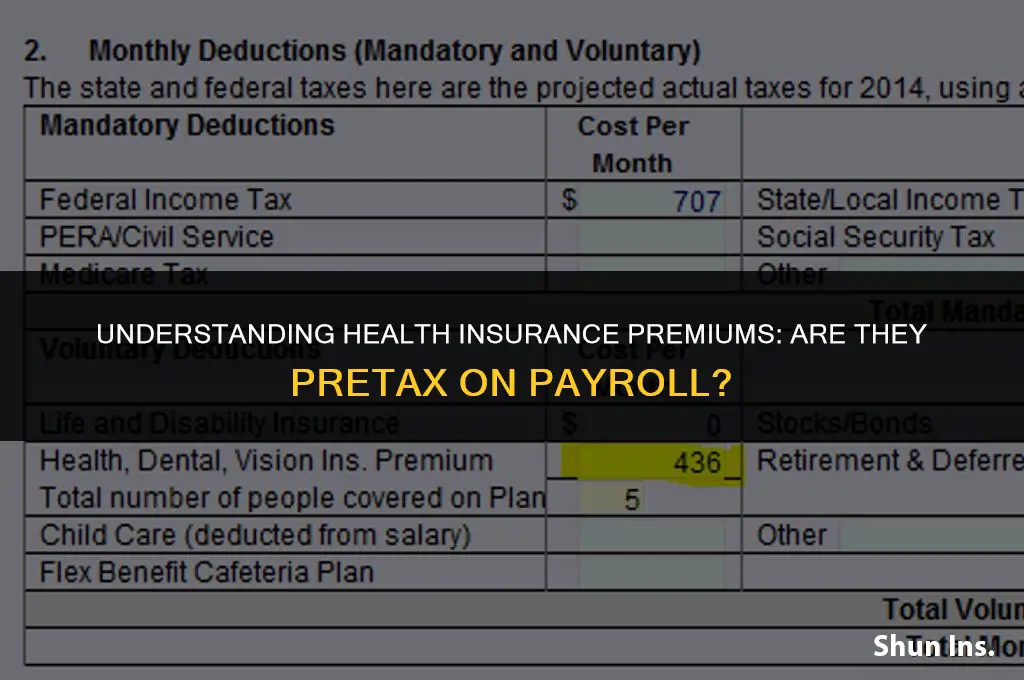

Health insurance premiums are often deducted from an employee's paycheck before taxes are applied, which is known as pretax payroll deductions. This practice can provide significant tax savings for both employees and employers. By deducting health insurance premiums pretax, employees reduce their taxable income, which can lower their overall tax liability. Employers also benefit from this arrangement as it reduces their payroll tax obligations. However, it's important to note that not all health insurance plans are eligible for pretax deductions, and there may be limitations on the amount that can be deducted. Understanding the specifics of pretax health insurance deductions can help individuals make informed decisions about their health coverage and tax planning.

Explore related products

$5.89 $7.99

$14.41 $15.95

What You'll Learn

- Definition of Pretax: Understanding what pretax means in the context of payroll and health insurance

- Tax Advantages: Exploring the tax benefits of pretax health insurance deductions for employees

- Employer Contributions: Discussing how employers contribute to pretax health insurance plans

- Impact on Take-Home Pay: Analyzing how pretax health insurance affects an employee's net pay

- Common Pretax Plans: Listing examples of common pretax health insurance plans like FSAs and HSAs

![]()

Definition of Pretax: Understanding what pretax means in the context of payroll and health insurance

Pretax deductions are amounts withheld from an employee's gross pay before taxes are calculated. These deductions are typically used for contributions to retirement plans, health insurance premiums, and other benefits. In the context of payroll and health insurance, understanding pretax deductions is crucial for both employers and employees.

For employers, pretax deductions reduce the amount of taxable income they report for each employee, which can lower their payroll tax liabilities. This is because pretax deductions are subtracted from gross wages before federal, state, and local taxes are applied. As a result, employers need to accurately calculate and report these deductions to comply with tax regulations and avoid penalties.

Employees benefit from pretax deductions because they reduce the amount of income subject to taxation, which can increase their take-home pay. For example, if an employee contributes $100 per month to a pretax health insurance plan, this amount is deducted from their gross pay before taxes are calculated. Assuming a combined federal and state tax rate of 25%, the employee would save $25 in taxes per month, resulting in a net increase in take-home pay of $75.

Pretax deductions for health insurance are particularly important because they can make health coverage more affordable for employees. By reducing the cost of health insurance premiums through pretax deductions, employers can offer more competitive benefits packages and attract and retain top talent. Additionally, pretax health insurance deductions can help employees save money on their health care expenses, which can improve their overall financial well-being.

In conclusion, pretax deductions play a significant role in the payroll and health insurance landscape. By understanding how pretax deductions work and their benefits, employers and employees can make informed decisions about their compensation and benefits packages, ultimately leading to more efficient and effective management of payroll and health insurance costs.

Does Your Employer Need to Provide Health Insurance? Key Facts

You may want to see also

Explore related products

![]()

Tax Advantages: Exploring the tax benefits of pretax health insurance deductions for employees

One of the most significant advantages of pretax health insurance deductions is the reduction in an employee's taxable income. By deducting health insurance premiums before taxes are calculated, employees can lower their overall tax liability. This is because the premiums are not subject to federal, state, and local income taxes, which can result in substantial savings depending on the employee's tax bracket and the cost of their health insurance.

Another key benefit is that pretax deductions can also reduce the amount of Social Security and Medicare taxes that employees pay. Since these taxes are calculated based on an employee's gross income, lowering the taxable income through pretax health insurance deductions can lead to a decrease in the amount withheld for these programs. This can put more money in an employee's pocket each paycheck, potentially increasing their take-home pay.

Employers also benefit from offering pretax health insurance deductions. By providing this option, employers can attract and retain top talent, as employees often view pretax deductions as a valuable perk. Additionally, employers may be able to reduce their own tax liabilities by offering pretax deductions, as they may be able to deduct the administrative costs associated with managing the pretax deduction program.

It's important to note that there are some limitations to pretax health insurance deductions. For example, the amount that can be deducted is typically limited to the actual cost of the health insurance premiums. Employees cannot deduct more than they are actually paying for health insurance. Additionally, pretax deductions may not be available for all types of health insurance plans, such as health savings accounts (HSAs) or flexible spending accounts (FSAs).

To maximize the tax advantages of pretax health insurance deductions, employees should carefully review their health insurance options and consult with a tax professional. By understanding the rules and limitations of pretax deductions, employees can make informed decisions about their health insurance and potentially save money on their taxes.

Do Taxes Inquire About Health Insurance? What You Need to Know

You may want to see also

Explore related products

![]()

Employer Contributions: Discussing how employers contribute to pretax health insurance plans

Employers play a significant role in the pretax health insurance landscape by contributing to their employees' health plans. These contributions are typically made on a pretax basis, meaning they are deducted from the employee's gross income before taxes are calculated. This arrangement provides a financial benefit to both the employer and the employee. For the employer, pretax contributions can reduce their payroll tax liabilities, while for the employee, it lowers their taxable income, potentially resulting in a lower tax bill.

The mechanics of employer contributions to pretax health insurance plans involve a straightforward process. Employers set up a health insurance plan and agree to contribute a certain percentage or dollar amount towards each employee's premiums. These contributions are then deducted from the employee's paycheck on a pretax basis. It's important to note that the specific details of these contributions, such as the percentage or amount, can vary widely between employers and are often influenced by factors like the size of the company, the industry, and the overall benefits package offered.

One of the key considerations for employers when setting up pretax health insurance contributions is compliance with IRS regulations. Employers must ensure that their plans meet certain criteria to qualify for pretax treatment. This includes offering the plan to all eligible employees, maintaining accurate records of contributions, and providing employees with information about the plan's terms and conditions. Failure to comply with these regulations can result in penalties and the loss of pretax status for the contributions.

In addition to the direct financial benefits, employer contributions to pretax health insurance plans can also have a positive impact on employee morale and retention. By offering a valuable benefit like health insurance, employers can attract and retain top talent, as well as demonstrate their commitment to the well-being of their workforce. This can lead to increased job satisfaction and loyalty among employees, which can ultimately benefit the company's bottom line.

Overall, employer contributions to pretax health insurance plans are a critical component of many companies' benefits packages. They provide financial advantages to both employers and employees, while also helping to ensure that employees have access to affordable health care. By carefully managing these contributions and ensuring compliance with IRS regulations, employers can maximize the benefits of pretax health insurance plans for their workforce.

Liability and Malpractice Insurance: Are They Synonymous?

You may want to see also

![]()

Impact on Take-Home Pay: Analyzing how pretax health insurance affects an employee's net pay

The impact of pretax health insurance on an employee's take-home pay is a critical aspect to consider when evaluating the overall compensation package. Pretax health insurance deductions reduce the gross income subject to federal, state, and local taxes, which can result in a lower tax liability and, consequently, a higher net pay. For instance, if an employee's gross income is $50,000 and the annual health insurance premium is $5,000, the pretax deduction would reduce the taxable income to $45,000. This reduction in taxable income can lead to significant savings, depending on the employee's tax bracket.

To analyze the effect of pretax health insurance on take-home pay, employees should first understand their tax brackets and how the deductions impact their overall tax liability. Using tax calculators or consulting with a financial advisor can help in determining the exact impact. Additionally, employees should consider the trade-off between the tax savings and the actual cost of the health insurance premiums. In some cases, the tax savings may not fully offset the cost of the premiums, resulting in a net decrease in take-home pay.

Employers also play a crucial role in this analysis. By offering pretax health insurance options, employers can help employees maximize their tax savings and potentially increase their net pay. However, employers should also be transparent about the costs associated with these benefits and provide resources to help employees make informed decisions.

In conclusion, the impact of pretax health insurance on take-home pay is multifaceted and requires careful consideration of tax implications, premium costs, and overall compensation. Both employees and employers should work together to ensure that the benefits of pretax health insurance are maximized while minimizing any potential drawbacks.

Supplemental Insurance Options for TennCare Medicaid: What You Need to Know

You may want to see also

![]()

Common Pretax Plans: Listing examples of common pretax health insurance plans like FSAs and HSAs

Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) are two prevalent types of pretax health insurance plans. FSAs allow employees to set aside a portion of their earnings, on a pretax basis, to cover qualified medical expenses such as deductibles, copayments, and prescription drugs. HSAs, on the other hand, are available to individuals who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. Contributions to HSAs are tax-deductible, and the funds can be used to pay for qualified medical expenses, with the added benefit of earning interest over time.

Another example of a pretax plan is the Health Reimbursement Arrangement (HRA). HRAs are employer-funded plans that reimburse employees for qualified medical expenses. Unlike FSAs and HSAs, HRAs do not require employees to contribute their own funds. Instead, employers allocate a certain amount of money to each employee's HRA, which can then be used to cover medical costs.

Pretax plans offer several advantages, including reducing an individual's taxable income and providing a way to save money on healthcare expenses. However, it's essential to understand the specific rules and limitations of each plan. For instance, FSAs typically have a "use-it-or-lose-it" policy, meaning that any unused funds at the end of the plan year are forfeited. HSAs, on the other hand, allow funds to roll over from year to year and can even be invested, offering a potential long-term savings benefit.

When considering pretax health insurance plans, it's crucial to evaluate one's healthcare needs and financial situation. Factors such as the cost of premiums, the likelihood of incurring medical expenses, and the potential tax benefits should all be taken into account. By carefully weighing these considerations, individuals can make informed decisions about whether a pretax plan is right for them.

Understanding Texas Women's Health Insurance Coverage: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, health insurance premiums are typically pretax on payroll. This means that the amount deducted from your paycheck for health insurance is not subject to federal income tax, Social Security tax, or Medicare tax.

Pretax health insurance reduces your taxable income. The premiums you pay are subtracted from your gross income before taxes are calculated, which can lower your overall tax liability.

There are no federal limits on the amount of health insurance premiums that can be pretax. However, some states may have their own limits or restrictions, so it's important to check your state's regulations.