The question of whether health insurance is still worth it is a pressing concern for many individuals and families. With rising premiums, deductibles, and copays, it's natural to wonder if the benefits of having health insurance outweigh the costs. This is especially true for those who are generally healthy and may not see the need for frequent medical care. However, health insurance provides a crucial safety net in case of unexpected illnesses or accidents, which can be financially devastating without proper coverage. Additionally, health insurance can offer preventive care and wellness programs that can help maintain good health and potentially reduce long-term healthcare costs. Ultimately, the value of health insurance depends on individual circumstances, including one's health status, financial situation, and personal preferences.

| Characteristics | Values |

|---|---|

| Topic | Health Insurance |

| Context | Evaluating the worth of health insurance in current times |

| Purpose | To inform and analyze the benefits and drawbacks of health insurance |

| Audience | Individuals seeking information on health insurance |

| Scope | Covers various aspects such as cost, coverage, and necessity |

| Bias | Neutral, providing balanced information |

| Format | Informative article or guide |

| Length | Approximately 1000-1500 words |

| Language | English |

| Style | Formal and educational |

| Key Points | - Rising costs of health insurance - Changes in healthcare policies - Importance of coverage for unexpected medical expenses - Alternatives to traditional health insurance - Impact of health insurance on financial stability |

| Sources | Reputable health and finance websites, expert opinions |

| Conclusion | Health insurance is still worth considering due to its ability to provide financial protection against unforeseen medical costs, despite increasing premiums and changing policies. |

Explore related products

What You'll Learn

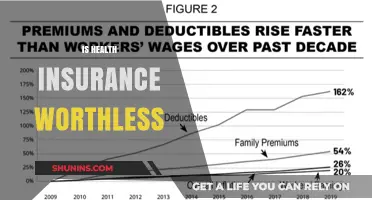

- Rising Costs: Premiums, deductibles, and out-of-pocket expenses continue to increase, making health insurance less affordable

- Limited Coverage: Many plans restrict coverage for pre-existing conditions, leaving individuals with high medical bills

- Network Limitations: Insurers often have narrow provider networks, limiting access to preferred doctors and hospitals

- Preventive Care: While some plans cover preventive services, the overall value may not justify the cost for healthy individuals

- Alternative Options: With the rise of telemedicine and urgent care centers, some may find alternative healthcare options more cost-effective

![]()

Rising Costs: Premiums, deductibles, and out-of-pocket expenses continue to increase, making health insurance less affordable

The relentless rise in healthcare costs has become a pressing concern for many individuals and families. Premiums, deductibles, and out-of-pocket expenses have all seen significant increases in recent years, leading to a growing debate about the affordability and value of health insurance. This trend is particularly troubling given that healthcare is often considered a fundamental right, yet the escalating costs are making it increasingly difficult for people to access the care they need.

One of the primary drivers of these rising costs is the increasing price of medical services and treatments. As healthcare providers face their own financial pressures, they often pass these costs on to patients in the form of higher bills. Additionally, the growing prevalence of chronic diseases and the aging population are contributing to the upward trend in healthcare spending. Insurance companies, in turn, are raising premiums to cover these higher costs, which can make health insurance seem less and less affordable for the average person.

Another factor contributing to the rising costs of health insurance is the increasing complexity of insurance plans themselves. Many plans now come with high deductibles and co-pays, which can make it difficult for individuals to predict their out-of-pocket expenses. This lack of transparency can lead to unexpected medical bills, further exacerbating the financial strain on policyholders. Moreover, the administrative costs associated with managing these complex plans can also drive up premiums.

The impact of these rising costs is being felt across all segments of the population. For those with lower incomes, the increasing premiums and out-of-pocket expenses can be particularly devastating, as they may be forced to choose between paying for health insurance and covering other essential expenses. Even those with higher incomes are not immune, as the rising costs can still represent a significant financial burden. This has led many to question whether health insurance is still worth the investment, especially if they are generally healthy and do not anticipate needing extensive medical care.

Despite these challenges, it is important to note that health insurance can still provide valuable protection and peace of mind. A serious illness or injury can result in substantial medical bills, and having health insurance can help mitigate these costs. Additionally, many insurance plans now offer preventive care benefits, which can help individuals stay healthy and potentially avoid more costly medical issues down the line. However, it is crucial for individuals to carefully evaluate their options and choose a plan that best fits their needs and budget.

In conclusion, the rising costs of health insurance premiums, deductibles, and out-of-pocket expenses are a significant concern that requires careful consideration. While health insurance can still offer important benefits, it is essential for individuals to weigh these benefits against the increasing costs and make informed decisions about their healthcare coverage.

Millennials and Health Insurance: How Many Are Uninsured?

You may want to see also

Explore related products

![]()

Limited Coverage: Many plans restrict coverage for pre-existing conditions, leaving individuals with high medical bills

Individuals with pre-existing conditions often face significant challenges when seeking health insurance coverage. Many plans impose limitations or exclusions on these conditions, leaving policyholders with substantial out-of-pocket expenses. This can be particularly burdensome for those with chronic illnesses or long-term health issues, who may require ongoing medical care and medications.

One of the primary reasons for these limitations is the insurance industry's practice of underwriting, which involves assessing an individual's health risk to determine their eligibility for coverage and the premiums they will pay. Insurers may deny coverage or impose exclusions for pre-existing conditions if they deem the risk too high. This can result in individuals being left without adequate coverage for their health needs, leading to financial strain and potential medical complications.

Furthermore, even when coverage is provided, it may not be comprehensive. Some plans may only cover certain aspects of a pre-existing condition, such as medications or doctor visits, while excluding others, like hospital stays or surgical procedures. This can create gaps in coverage that leave individuals vulnerable to high medical bills.

The impact of these limitations can be far-reaching. Individuals with pre-existing conditions may delay or forgo necessary medical care due to cost concerns, potentially leading to worsening health outcomes. Additionally, the financial burden of high medical bills can lead to stress, anxiety, and even bankruptcy in extreme cases.

In light of these challenges, it is essential for individuals with pre-existing conditions to carefully evaluate their health insurance options. They should consider factors such as the scope of coverage, exclusions, and out-of-pocket costs when selecting a plan. Additionally, they may benefit from consulting with a healthcare advocate or insurance broker who can help them navigate the complexities of the insurance system and find the best possible coverage for their needs.

Exploring the Surge in Farm Insurance Companies: Causes and Impact

You may want to see also

Explore related products

![]()

Network Limitations: Insurers often have narrow provider networks, limiting access to preferred doctors and hospitals

One of the most frustrating aspects of health insurance for many policyholders is the limitation imposed by provider networks. Insurers often contract with a select group of healthcare providers, creating a network that policyholders must use to receive covered care. This can significantly restrict access to preferred doctors, specialists, and hospitals, particularly those that are renowned for their expertise or are located in convenient areas. For individuals with specific health conditions or those who have established relationships with certain healthcare professionals, these network limitations can be particularly burdensome.

The rationale behind these narrow networks is often rooted in cost control. By limiting the number of providers in their network, insurers can negotiate better rates and reduce their overall expenditure on healthcare services. However, this cost-saving measure can come at a high price for policyholders, who may find themselves unable to access the care they need or forced to travel long distances to receive treatment from in-network providers. This can lead to delays in care, increased stress, and potentially worse health outcomes.

Moreover, network limitations can also impact the quality of care received. When policyholders are restricted to a narrow network, they may not have access to the most specialized or advanced treatments available. This can be particularly problematic for individuals with rare or complex conditions that require care from highly specialized providers. In such cases, being forced to use in-network providers can result in suboptimal care and potentially poorer health outcomes.

Another issue with narrow networks is the lack of transparency surrounding them. Often, policyholders are not fully aware of the limitations of their network until they attempt to seek care. This can lead to unexpected denials of coverage and additional out-of-pocket expenses. Furthermore, the process of appealing these denials can be time-consuming and stressful, adding another layer of complexity to an already challenging situation.

In conclusion, while health insurance is intended to provide financial protection and access to healthcare, network limitations can significantly undermine these goals. Policyholders must carefully consider the provider network when selecting a health insurance plan and be prepared to navigate the potential challenges and limitations that may arise. It is essential for insurers to balance cost control with the need to provide comprehensive access to quality care, ensuring that policyholders can receive the treatment they need without undue burden or expense.

Should You Join Your Spouse's Health Insurance Plan? Pros and Cons

You may want to see also

Explore related products

![]()

Preventive Care: While some plans cover preventive services, the overall value may not justify the cost for healthy individuals

For healthy individuals, the calculus around preventive care coverage can be particularly complex. While it's undeniable that preventive services such as annual check-ups, vaccinations, and screenings can play a crucial role in maintaining good health, the cost-benefit analysis isn't always clear-cut. Many health insurance plans do cover these services, but the premiums for such plans can be prohibitively high, especially for those who are young and healthy.

One approach to evaluating the worth of preventive care coverage is to consider the likelihood of needing these services. For instance, a 25-year-old with no pre-existing conditions may not require frequent medical attention, making the cost of a comprehensive plan with preventive care coverage seem unjustified. However, this perspective overlooks the potential long-term benefits of early detection and prevention. Certain conditions, such as hypertension or diabetes, can be asymptomatic in their early stages but can lead to serious complications if left untreated.

Another factor to consider is the availability of free or low-cost preventive services outside of insurance plans. Many community health clinics and public health initiatives offer screenings and vaccinations at little to no cost, which can make the additional expense of insurance coverage for these services seem redundant. However, these resources may not be universally accessible or comprehensive, and they may not provide the same level of personalized care as a private physician.

Ultimately, the decision of whether to opt for preventive care coverage through health insurance depends on a variety of factors, including individual health status, financial situation, and personal preferences. While it may not be necessary for everyone, particularly healthy individuals, to have comprehensive preventive care coverage, it's essential to weigh the potential benefits against the costs and to consider alternative options for accessing preventive services.

Understanding 1099-C Health Insurance: Benefits, Eligibility, and Tax Implications

You may want to see also

![]()

Alternative Options: With the rise of telemedicine and urgent care centers, some may find alternative healthcare options more cost-effective

The proliferation of telemedicine and urgent care centers has revolutionized the healthcare landscape, offering viable alternatives to traditional health insurance. These options can be significantly more cost-effective, especially for individuals who do not require comprehensive coverage. Telemedicine, for instance, allows patients to consult with healthcare professionals remotely, reducing the need for costly office visits. This is particularly beneficial for those with minor ailments or chronic conditions that require regular monitoring but not necessarily in-person care.

Urgent care centers, on the other hand, provide immediate medical attention for non-life-threatening conditions at a fraction of the cost of emergency room visits. They are ideal for treating illnesses such as colds, flu, sprains, and minor injuries. The convenience and affordability of these centers make them an attractive option for those without insurance or with high deductibles.

Moreover, the rise of health savings accounts (HSAs) and flexible spending accounts (FSAs) has further enhanced the appeal of alternative healthcare options. These accounts allow individuals to set aside pre-tax dollars for medical expenses, providing a financial cushion for out-of-pocket costs. By combining these savings tools with alternative care options, many people can effectively manage their healthcare costs without relying on traditional insurance.

However, it is crucial to note that while these alternatives can be cost-effective, they may not be suitable for everyone. Individuals with complex medical conditions or those who require extensive care should carefully consider their options before foregoing traditional health insurance. Additionally, it is essential to research and compare the costs and services of different alternative providers to ensure that one is receiving quality care at a reasonable price.

In conclusion, the emergence of telemedicine and urgent care centers, coupled with the availability of health savings tools, has created a new paradigm in healthcare. For many, these alternatives offer a more affordable and convenient way to manage their health needs. However, it is important to weigh the pros and cons carefully and make an informed decision based on individual circumstances.

Understanding Ultimate Losses: Key to Insurance Company Financial Stability

You may want to see also

Frequently asked questions

Health insurance is still generally worth it, as it provides financial protection against unexpected medical expenses. Without insurance, a single major health issue could lead to significant out-of-pocket costs. While premiums are increasing, the benefits of coverage often outweigh the costs, especially for those with chronic conditions or who require regular medical care.

Alternatives to traditional health insurance plans include Health Savings Accounts (HSAs), which allow you to save money tax-free for medical expenses; short-term health insurance, which provides temporary coverage for a limited period; and catastrophic health insurance, which covers only major medical expenses. Additionally, some people opt for telemedicine services or direct primary care models, which can offer more affordable access to healthcare.

To determine if your current health insurance plan is still the best option, review your plan's coverage, premiums, deductibles, and out-of-pocket costs. Compare these with other available plans during open enrollment periods. Consider your current health needs, anticipated medical expenses, and the network of providers available under each plan. If your needs have changed or you can find a more cost-effective plan with similar coverage, it may be worth switching.