Health Maintenance Organizations (HMOs) are a type of health insurance plan that aims to reduce unnecessary healthcare costs through various mechanisms, including economic incentives for physicians and patients to select less costly forms of care, programs for reviewing the medical necessity of specific services, increased beneficiary cost-sharing, and controlling inpatient admissions and lengths of stay, among other methods. HMOs typically require members to choose a primary care physician (PCP) who acts as a gatekeeper to more specialized care. This model is designed to promote preventive care and manage chronic conditions more effectively, potentially leading to better health outcomes and lower overall healthcare expenditures.

Explore related products

![]()

What is an HMO?

An HMO, or Health Maintenance Organization, is a type of health insurance plan that provides coverage through a network of healthcare providers. Unlike traditional fee-for-service plans, HMOs require members to use in-network providers for most medical services. This means that if you're enrolled in an HMO plan, you'll typically need to choose a primary care physician (PCP) who is part of the HMO's network. Your PCP will then coordinate your care and refer you to specialists within the network when necessary.

One of the key features of HMOs is their focus on preventive care. HMO plans often emphasize wellness programs, routine check-ups, and screenings to help members stay healthy and avoid costly medical procedures. This approach can lead to lower overall healthcare costs for both the insurer and the insured. Additionally, HMOs may offer prescription drug coverage, dental care, and vision care as part of their plans, although the specifics can vary depending on the provider.

When considering an HMO plan, it's important to understand the potential limitations. For instance, you may face higher out-of-pocket costs if you choose to see a provider outside of the HMO's network. Furthermore, some HMO plans require members to obtain prior authorization before undergoing certain medical procedures or treatments. This can sometimes lead to delays in receiving care, although it's intended to ensure that only medically necessary services are covered.

Despite these limitations, HMOs can be an attractive option for many individuals and families. They often offer lower premiums compared to other types of health insurance plans, and the emphasis on preventive care can lead to better overall health outcomes. If you're considering enrolling in an HMO plan, it's essential to carefully review the plan's details, including the network of providers, the coverage options, and the associated costs. By doing so, you can determine whether an HMO is the right choice for your healthcare needs.

Get Medical Insurance Before It's Too Late

You may want to see also

Explore related products

![]()

How does HMO work?

Health Maintenance Organizations (HMOs) operate on a prepaid health care system where members pay a fixed monthly fee for a range of health services. This fee typically covers all or most medical expenses, with some plans requiring copayments for certain services. HMOs focus on preventive care and managing health risks to reduce overall healthcare costs. They often provide wellness programs, screenings, and health education to encourage members to maintain a healthy lifestyle.

One of the key aspects of how HMOs work is their emphasis on primary care physicians (PCPs). Members are usually required to choose a PCP who serves as their main point of contact for medical care. This PCP coordinates all healthcare services, including referrals to specialists, hospitalizations, and diagnostic tests. The HMO model aims to streamline care and ensure that members receive appropriate and cost-effective treatments.

HMOs also employ utilization review processes to monitor and control the use of healthcare services. This involves reviewing medical claims to ensure that treatments are necessary, appropriate, and within the scope of the member's plan. By doing so, HMOs can prevent unnecessary procedures and reduce healthcare costs. Additionally, HMOs often negotiate rates with healthcare providers, which can result in lower costs for members compared to traditional fee-for-service insurance plans.

In summary, HMOs work by providing prepaid health care services with a focus on preventive care, primary care coordination, utilization review, and cost control measures. This model aims to deliver comprehensive healthcare while managing costs effectively.

Why Insurance Companies Advertise: Unlocking the Secrets Behind Their Marketing Strategies

You may want to see also

Explore related products

![]()

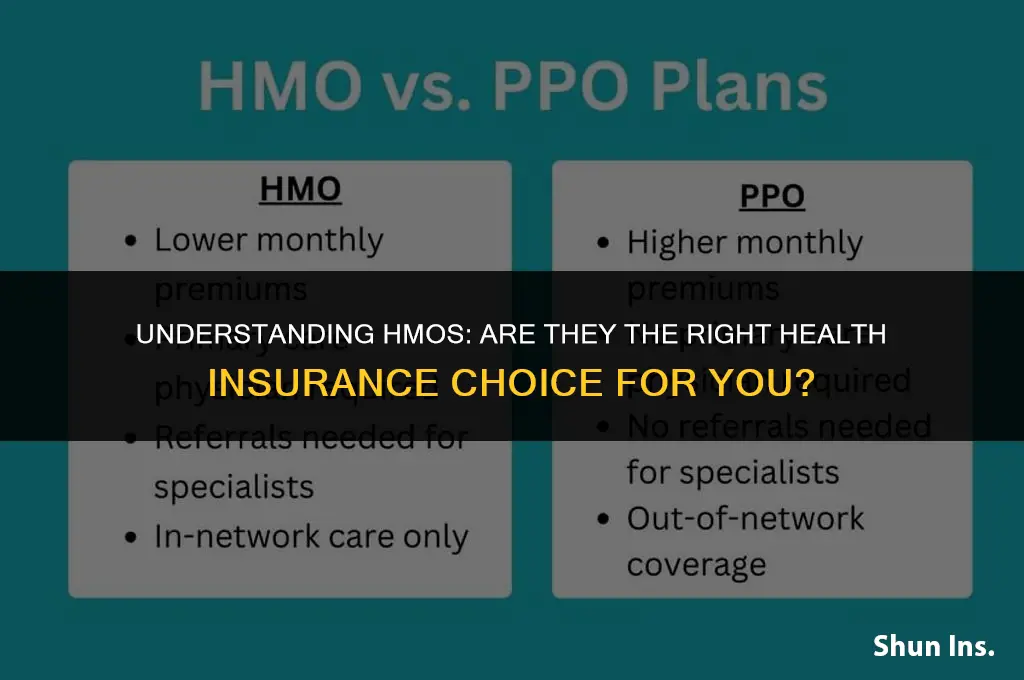

HMO vs. PPO

Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) are two common types of health insurance plans, each with its own set of benefits and drawbacks. Understanding the differences between these two options is crucial for individuals and families looking to choose the best health coverage for their needs.

HMOs typically require members to choose a primary care physician (PCP) who acts as a gatekeeper for all medical services. This means that before seeing a specialist, an HMO member must first consult with their PCP, who will then refer them to an in-network specialist if necessary. HMOs generally have lower premiums and out-of-pocket costs compared to PPOs, making them an attractive option for those looking to save money on healthcare. However, the trade-off is that HMOs often have more restrictive networks and may not cover out-of-network care, which can limit members' choices when it comes to healthcare providers.

On the other hand, PPOs offer more flexibility in terms of provider choice and do not require members to choose a PCP. PPO members can see any in-network provider without a referral and are also covered for out-of-network care, albeit at a higher cost. PPOs tend to have higher premiums than HMOs, but they also offer more comprehensive coverage and greater peace of mind for those who value the ability to choose their own healthcare providers.

When deciding between an HMO and a PPO, it's important to consider factors such as cost, provider choice, and the need for referrals. Individuals who are looking to save money on healthcare and are comfortable with having a PCP manage their care may find an HMO to be a good fit. Conversely, those who value the ability to choose their own providers and are willing to pay more for that flexibility may prefer a PPO.

In conclusion, the choice between an HMO and a PPO ultimately depends on individual preferences and healthcare needs. By carefully weighing the pros and cons of each option, individuals can make an informed decision about which type of health insurance plan is best suited for them.

Honolulu: Finding Medical Help Without Insurance

You may want to see also

Explore related products

![]()

HMO coverage

Health Maintenance Organizations (HMOs) are a type of health insurance plan that provides coverage for medical services through a network of healthcare providers. Unlike traditional indemnity plans, HMOs require members to use in-network providers for most medical services, with the exception of emergencies. This network approach allows HMOs to negotiate lower rates with providers, which can result in lower premiums and out-of-pocket costs for members.

One of the key features of HMO coverage is the emphasis on preventive care. HMOs often cover routine check-ups, vaccinations, and screenings at little or no cost to the member. This focus on prevention can help to reduce the overall cost of healthcare by catching and treating conditions early, before they become more serious and expensive to treat.

Another important aspect of HMO coverage is the coordination of care. Because members are required to use in-network providers, their medical records and treatment plans are more likely to be shared and coordinated among their healthcare team. This can lead to better overall care, as providers are aware of the member's medical history and can work together to develop a comprehensive treatment plan.

However, HMO coverage also has some limitations. Members may have less flexibility in choosing their healthcare providers, and may need to obtain referrals from their primary care physician in order to see a specialist. Additionally, HMOs may not cover out-of-network services, except in certain circumstances, such as emergencies.

Overall, HMO coverage can be a cost-effective and comprehensive option for individuals and families looking for health insurance. By understanding the unique features and limitations of HMO plans, members can make informed decisions about their healthcare coverage and get the most out of their insurance benefits.

Understanding the Three Main Types of Health Insurance Plans

You may want to see also

Explore related products

![]()

HMO drawbacks

One significant drawback of Health Maintenance Organizations (HMOs) is the restriction on choosing healthcare providers. Unlike other insurance plans, HMOs typically require members to select a primary care physician (PCP) from within the network, and referrals to specialists are often necessary. This can limit access to preferred doctors or specialists, potentially leading to delays in care or dissatisfaction with the quality of care received.

Another drawback is the potential for higher out-of-pocket costs. While HMOs generally offer lower premiums compared to other types of health insurance, members may face higher copayments or coinsurance for certain services. Additionally, HMOs often have strict coverage guidelines, which may result in denials for certain treatments or procedures that are deemed experimental or not medically necessary.

HMOs also have a reputation for being less flexible when it comes to out-of-network care. In most cases, HMO members are responsible for the full cost of care received from providers outside the network, except in emergency situations. This lack of flexibility can be particularly problematic for individuals who travel frequently or live in areas with limited healthcare options.

Furthermore, the quality of care provided through HMOs can vary significantly depending on the network and the specific plan. Some HMOs may prioritize cost-cutting measures over patient care, leading to concerns about the overall quality of care received. It's essential for individuals considering an HMO to research the network's reputation and read reviews from current members to get a sense of the quality of care they can expect.

In conclusion, while HMOs can offer lower premiums and a simplified approach to healthcare, they also come with several drawbacks, including restrictions on provider choice, potential for higher out-of-pocket costs, limited flexibility for out-of-network care, and varying quality of care. It's crucial for individuals to weigh these drawbacks against the benefits when deciding whether an HMO is the right choice for their healthcare needs.

Medical Billing: Insurance Claims and Provider Requirements

You may want to see also

Frequently asked questions

HMO stands for Health Maintenance Organization.

Yes, HMO is a type of health insurance plan that provides coverage for medical services through a network of healthcare providers.

An HMO plan requires members to choose a primary care physician (PCP) who coordinates their care. Members must use in-network providers for most services, and referrals from the PCP are often required to see specialists.

HMO plans often have lower premiums and out-of-pocket costs compared to other types of health insurance. They also typically cover preventive care and wellness services at no additional cost.

HMO plans may have more restrictions on choosing healthcare providers and may require members to use in-network providers for most services. Additionally, members may need to get referrals from their PCP to see specialists, which can sometimes delay care.