Investors need to be aware of the insurance limits of their investment accounts to understand the level of protection their assets have. The Securities Investor Protection Corporation (SIPC) is a federally mandated, private nonprofit organisation that protects investors in the event of a broker-dealer failing and customers losing their securities and/or cash. SIPC insurance covers investors for up to \$500,000 in securities and \$250,000 in uninvested cash per account. However, there are circumstances where investors can be covered for more than \$500,000, for example, when investors have multiple accounts of different types.

| Characteristics | Values |

|---|---|

| Organization | Securities Investor Protection Corporation (SIPC) |

| Type | Nonprofit membership corporation |

| Coverage | Up to $500,000 in securities and up to $250,000 in uninvested cash per account |

| Protection | Against losses due to broker or dealer insolvency or bankruptcy |

| Exclusions | Investment earnings, market activity, fraud, and other causes of loss |

| Additional Coverage | "Excess SIPC" insurance through a private carrier, with limits up to $100 million per account |

Explore related products

![Regulation Q, now accounts, investment in State housing corporations: Hearings, Ninety-third Congress, first session, on H.R. 4070, H.R. 4719 [and] H.R. 4988. March 13, 14, and 15, 1973](https://m.media-amazon.com/images/I/71V4V1L-9sL._AC_UY218_.jpg)

What You'll Learn

- SIPC insurance covers investors for up to $500,000 in securities and $250,000 in uninvested cash

- SIPC steps in when a brokerage firm fails financially and assets are missing

- SIPC does not protect against regular investment losses

- SIPC insurance does not cover non-deposit investments or investment products

- SIPC coverage is limited to $500,000 total per customer

![]()

SIPC insurance covers investors for up to $500,000 in securities and $250,000 in uninvested cash

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private nonprofit organisation that provides insurance coverage for investors. The SIPC was created in 1970 as part of the Securities Investor Protection Act (SIPA) to protect investors from brokerages becoming insolvent.

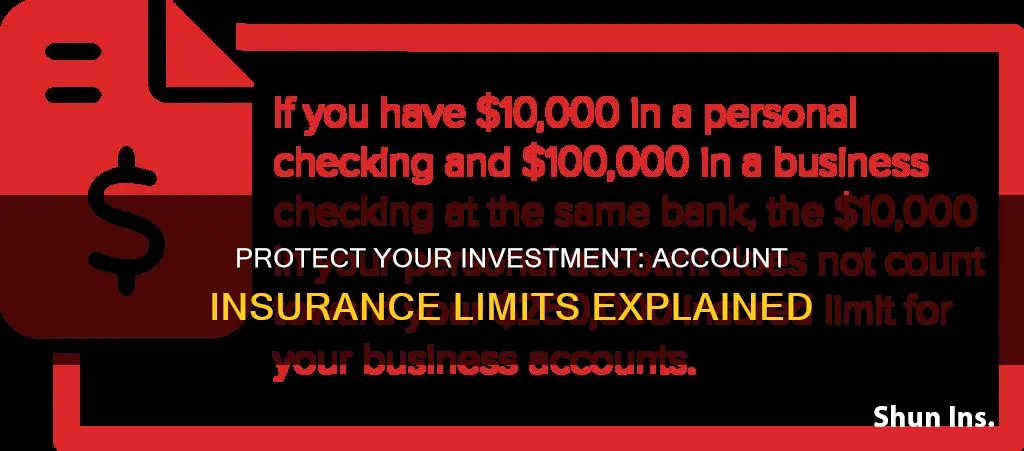

SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash per account. This means that if you have $500,000 in securities and $250,000 in cash, the entire amount may not be covered. However, if you have multiple accounts of different types, you may be covered for more than $500,000. For example, if you have an individual retirement account (IRA) and a joint account with your spouse, each account will be insured for up to $500,000, including $250,000 in cash.

It is important to note that SIPC protection is not the same as protection for your cash at a Federal Deposit Insurance Corporation (FDIC)-insured banking institution. SIPC does not protect the value of any security, and investments in the stock market are subject to fluctuations in market value. Instead, in a liquidation, SIPC replaces missing stocks and other securities when possible. SIPC protects cash in a brokerage firm account for the sale or purchase of securities, but cash held in connection with a commodities trade is not protected. Money market mutual funds are protected as securities by SIPC.

SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It works to restore investors' cash and securities, and has recovered billions of dollars for investors.

Gap Insurance: Money Back or Not?

You may want to see also

Explore related products

![]()

SIPC steps in when a brokerage firm fails financially and assets are missing

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organisation created by Congress as part of the Securities Investor Protection Act (SIPA) of 1970. It aims to protect investors from brokerages becoming insolvent.

SIPC steps in when a brokerage firm fails financially, and assets are missing from customer accounts. It protects customer assets when a SIPC-member brokerage firm fails financially.

SIPC protection is determined on an asset-by-asset basis and covers:

- Cash in a customer's account that is on deposit for the purchase of securities.

- "Securities," as defined under the Securities Investor Protection Act. This includes stocks, bonds, Treasury securities, certificates of deposit, mutual funds, and money market mutual funds.

- Certain futures contracts and options on such contracts, where those instruments are held in a portfolio margining account carried by a SIPC-member brokerage firm as a securities account pursuant to a portfolio margining program approved by the Securities and Exchange Commission (SEC).

It is important to note that SIPC coverage has limits. It provides up to $500,000 in total coverage per customer (or per account if the accounts are of separate capacities) for lost or missing assets of cash and/or securities. Within this total coverage, up to $250,000 can be used to protect cash within a customer's account that is not yet invested in securities.

SIPC does not protect against all types of losses and there are specific types of assets that are not covered by SIPC insurance. For example, digital asset securities that are unregistered investment contracts do not qualify as "securities" under SIPA and are therefore not protected, even if held by a SIPC-member brokerage firm. Similarly, commodity futures contracts held in an ordinary futures account are not protected by SIPC.

Death Insurance: Taxable Money or Not?

You may want to see also

Explore related products

![]()

SIPC does not protect against regular investment losses

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organization created by Congress under the Securities Investor Protection Act (SIPA) of 1970. It shields investors from brokerages becoming insolvent by recovering missing assets if a brokerage firm fails financially.

SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash per customer or per account. However, it is important to note that SIPC does not protect against regular investment losses. While SIPC insures investors for up to a certain limit, it does not protect against the risk of investments declining in value. For example, if an investor purchases stocks through a SIPC-member brokerage firm and those stocks lose value, SIPC will not cover the loss in value.

Additionally, SIPC does not protect against all types of assets. It does not cover commodity futures contracts unless they are held in a special portfolio margining account, foreign exchange trades, or investment contracts such as limited partnerships and fixed annuity contracts that are not registered with the U.S. Securities and Exchange Commission. Digital asset securities, including cryptocurrencies, are also not protected unless they are registered as investment contracts with the SEC.

Furthermore, SIPC does not cover claims against bad or inappropriate investment advice, and complaints about firms are typically handled by regulatory agencies such as the Financial Industry Regulatory Authority (FINRA) or the Securities and Exchange Commission. It is important for investors to understand the limitations of SIPC protection and seek additional insurance or protections as needed to safeguard their investments.

In summary, while SIPC provides valuable protection for investors in the event of brokerage firm failure, it does not protect against regular investment losses or declines in the value of investments. Investors should carefully review the types of assets covered and excluded by SIPC protection and consider additional measures to protect their investments.

Trip Insurance: Money-Waster or Money-Saver?

You may want to see also

Explore related products

![]()

SIPC insurance does not cover non-deposit investments or investment products

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organization created by Congress under the Securities Investor Protection Act (SIPA) in 1970. It aims to protect investors if their brokerage firm fails financially and their assets are missing or at risk.

SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of that total protecting cash within a customer's account that is not yet invested in securities. The SIPC protects stocks, bonds, Treasury securities, certificates of deposit, mutual funds, money market mutual funds, and certain other investments as "securities."

However, it is important to note that SIPC insurance does not cover all types of investments or investment products. For example, it does not protect commodity futures contracts unless they are held in a special portfolio margining account, foreign exchange trades, or investment contracts such as limited partnerships. Digital or crypto assets are also not protected unless they are registered with the U.S. Securities and Exchange Commission (SEC) as investment contracts.

Additionally, SIPC insurance does not cover non-deposit investments or investment products. This means that certain assets, such as U.S. Treasury bills, bonds, or notes, are not protected by SIPC insurance even if they were purchased at an insured bank.

It is always advisable to check with your brokerage firm for specific details regarding the types of accounts and investments covered by SIPC insurance, as there may be limitations or exclusions not mentioned here.

Strategies for Prospecting Commercial Insurance Policies

You may want to see also

![]()

SIPC coverage is limited to $500,000 total per customer

SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash, per account. The total amount of SIPC coverage is $500,000 per customer. This means that if you have $500,000 in securities and $250,000 in cash, the entire amount may not be covered. However, there are circumstances in which investors are covered for more than $500,000, such as when investors have multiple accounts of different types. For example, if you have a traditional individual retirement account (IRA) and a Roth IRA at the same brokerage, the SIPC will insure them separately, providing up to $1 million in coverage between the two accounts.

SIPC, or the Securities Investor Protection Corporation, is a federally mandated, private nonprofit organization. It was created as part of the Securities Investor Protection Act (SIPA) of 1970, which aimed to protect investors from brokerages becoming insolvent. SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It protects customer assets when a SIPC-member brokerage firm fails financially.

SIPC covers specific types of investments as securities, including stocks, bonds, Treasury securities, certificates of deposit, mutual funds, and money market mutual funds. It's important to note that SIPC does not protect all types of assets. For example, it does not cover commodity futures contracts (unless held in a special portfolio margining account), foreign exchange trades, or investment contracts (such as limited partnerships) that are not registered with the U.S. Securities and Exchange Commission.

To ensure your assets are protected, it's important to understand the specifics of SIPC coverage and the types of accounts included. While SIPC provides significant protection for investors, it is limited to $500,000 total per customer, with a breakdown of up to $250,000 for uninvested cash and $500,000 for securities per account.

Smart Ways to Spend Your Insurance Payout

You may want to see also

Frequently asked questions

SIPC insurance covers investors for up to up to $500,000 in securities and up to $250,000 in uninvested cash, for a total coverage of $500,000 per customer. However, there are circumstances in which investors are covered for more than $500,000, such as when investors have multiple accounts of different types. For example, if you have a traditional IRA and a Roth IRA, SIPC insures them separately, providing up to $1 million in coverage for the two accounts.

SIPC insurance covers securities such as stocks, bonds, Treasury securities, certificates of deposit, mutual funds, and money market mutual funds. It also covers cash held by the broker for customers in connection with the purchase or sale of securities. SIPC does not cover commodity futures contracts, foreign exchange trades, investment contracts, fixed annuity contracts that are not registered with the U.S., or regular investment losses.

The FDIC, or Federal Deposit Insurance Corporation, is an independent agency of the U.S. government that protects individuals against the loss of their deposits in an FDIC-insured bank or savings association that fails, up to a limit of $250,000 per account. SIPC, or Securities Investor Protection Corporation, on the other hand, is a federally mandated, private nonprofit organization created by Congress in 1970 to protect investors against losses due to broker bankruptcies or failures. SIPC insurance covers customers of SIPC-member broker-dealers if the firm fails financially, while FDIC insurance does not cover non-deposit investments or investment products.