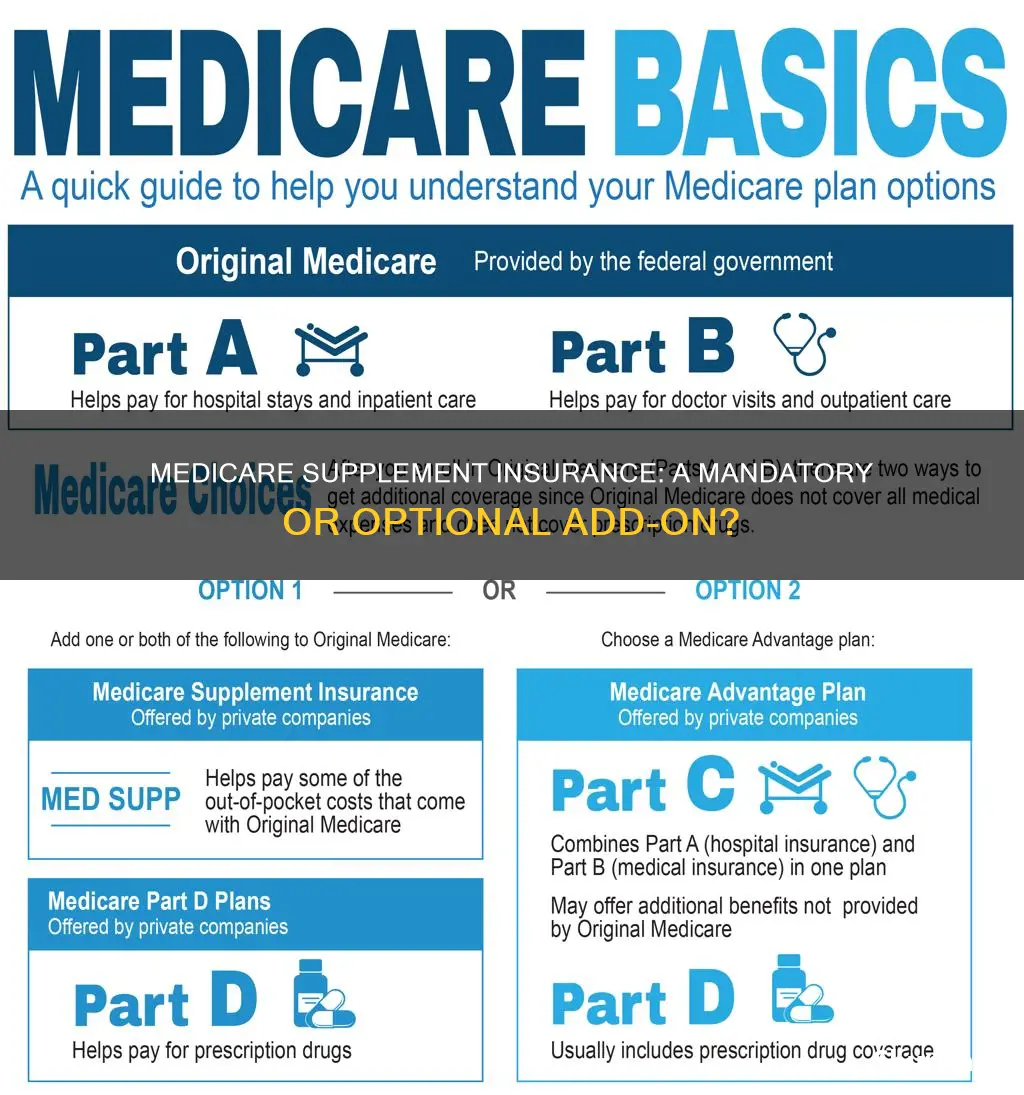

Medicare is a federal health insurance program that covers most healthcare costs for people aged 65 and over, as well as some people under 65 with disabilities. Medicare Supplement Insurance, also known as Medigap, is additional insurance that can be purchased from a private company to help cover out-of-pocket costs not covered by Original Medicare (Part A and Part B). While not everyone needs a Medicare supplement policy, it can be beneficial for those who want to fill the `gaps` in their existing coverage. Medigap policies are standardized and must follow federal and state laws, providing guaranteed renewable coverage as long as premiums are paid.

| Characteristics | Values |

|---|---|

| Name | Medicare Supplement Insurance |

| Other Names | Medigap |

| Description | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare |

| Who Can Buy | Generally, those with Medicare Part A and Part B |

| Who It Covers | Those aged 65 or older, and some people under 65 with disabilities |

| Who It Doesn't Cover | Those under 65 may not be able to buy a policy or may have to pay more |

| What It Covers | Hospital services, medical expenses, and some out-of-country travel expenses |

| What It Doesn't Cover | Long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs |

| Other Considerations | Medigap policies are standardized and named by letters (e.g., Plan G or Plan K) with the same benefits across companies |

| Buying Period | Buy within 6 months of getting Part A and Part B to avoid higher prices or unavailability |

Explore related products

What You'll Learn

- Medicare Supplement Insurance (Medigap) is extra insurance to help pay out-of-pocket costs

- Medigap policies are generally only available to those with Medicare Part A and Part B

- Medigap policies do not cover long-term care, vision, dental, hearing aids, or prescription drugs

- If you're under 65, you may not be able to buy a Medigap policy or may pay more

- Medigap policies are standardised and named by letters, e.g. Plan G or Plan K

![]()

Medicare Supplement Insurance (Medigap) is extra insurance to help pay out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is additional insurance that you can purchase from a private health insurance company. It helps cover your share of out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are designed to supplement the coverage provided by Original Medicare, filling in some of the gaps in coverage that exist in the original plan. These policies are standardized, meaning that each lettered plan offers the same basic benefits regardless of the insurance company. The price is usually the only differentiating factor between policies with the same letter sold by different companies.

It is important to note that Medigap is not mandatory, and you must have Original Medicare (Parts A and B) to be eligible for a Medigap policy. If you are under 65, you may face challenges in purchasing a Medigap policy or may have to pay higher premiums. There is a six-month Medigap Open Enrollment period that begins when you first get Part A and Part B and turn 65. During this period, you are guaranteed the right to buy any Medigap policy, regardless of pre-existing health conditions. However, after this period, you may encounter difficulties in purchasing a policy, or the cost may increase.

Medigap policies typically do not cover long-term care, such as nursing home stays, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap plans offer coverage for services that Original Medicare does not, such as emergency medical care when travelling outside the United States. It is essential to carefully review the coverage provided by each Medigap plan and compare them to ensure you select the one that best meets your specific needs.

Additionally, be cautious of illegal practices by insurance companies when shopping for a Medigap policy. Understand what Medigap covers, how it works with other Medicare coverage, and the associated costs. You can also seek free personalized health insurance counselling from your local State Health Insurance Assistance Program (SHIP) to make informed decisions about your coverage options.

Understanding In-Network Medical Insurance and Its Moop Meaning

You may want to see also

Explore related products

![]()

Medigap policies are generally only available to those with Medicare Part A and Part B

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private health insurance company. It helps cover costs that Original Medicare does not, such as certain vision, hearing, and dental services, as well as costs incurred while travelling outside the US. Medigap policies generally do not cover long-term care, prescription drugs, or private-duty nursing.

Medigap policies are typically only available to individuals with Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). If you have a spouse and you both require Medigap coverage, you will each need to purchase separate policies. It is important to note that Medigap policies are not available to those enrolled in a Medicare Advantage Plan (Part C). If you are considering switching to Original Medicare from a Medicare Advantage Plan, you will have a 12-month trial period during which you can get your Medigap policy back or choose a new one.

When purchasing a Medigap policy, it is important to do so within 6 months of enrolling in Part A and Part B. If you wait longer than 6 months, you may face higher costs or be unable to purchase a policy at all. Additionally, if you are under 65, you may have difficulty purchasing a Medigap policy or may be subject to higher premiums.

Medigap policies are standardized and named by letters, such as Plan G or Plan K. The benefits offered by each lettered plan are consistent across insurance companies, with the price being the only differentiating factor. It is worth noting that Medigap policies do not typically include prescription drug coverage. If prescription drug coverage is desired, a separate Medicare drug plan (Part D) must be purchased.

Travel Insurance: Comprehensive Medical Coverage Explained

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medigap policies do not cover long-term care, vision, dental, hearing aids, or prescription drugs

Medicare Supplement Insurance, also known as Medigap, is an additional insurance option that can be purchased from a private health insurance company. It is designed to help cover out-of-pocket costs associated with Original Medicare (Parts A and B). While Medigap can provide valuable coverage, it is important to note that it does not cover all types of expenses. Specifically, Medigap policies typically do not include coverage for long-term care, vision, dental, hearing aids, or prescription drugs.

Long-term care, such as nursing home stays, is not typically covered by Medigap policies. If an individual requires extended care in a nursing home or similar facility, they may need to explore alternative coverage options or payment methods. Medigap is designed to supplement Original Medicare, but it does not encompass all possible healthcare needs, and long-term care is often considered a separate category of healthcare service.

Vision and dental care are also generally excluded from Medigap coverage. Routine eye exams, vision correction needs (such as glasses or contact lenses), and dental check-ups, cleanings, and procedures are typically not covered under Medigap policies. These services are typically considered supplemental or optional by insurance providers and are, therefore, not included in the coverage. However, it is worth noting that some Medicare Advantage plans may offer coverage for certain vision and dental services, providing an alternative option for those seeking this type of coverage.

Hearing aids, which can be crucial for individuals with hearing impairments, are also generally not covered by Medigap policies. The cost of hearing aids and related services can vary widely and may not be affordable for everyone without insurance coverage. This exclusion highlights the need for individuals to carefully consider their specific healthcare needs when evaluating insurance options and exploring additional coverage plans to ensure their unique requirements are met.

Additionally, Medigap policies do not typically include coverage for prescription drugs. For individuals who require regular medication, this can be a significant expense. To address this, individuals can enrol in a separate Medicare drug plan, known as Part D, which provides prescription drug coverage. This option allows people to supplement their Medigap policy with the specific coverage they need for their prescription medications.

While Medigap policies do not cover these specific areas, they can still provide valuable coverage for other out-of-pocket expenses associated with Original Medicare. It is important for individuals to carefully review the benefits and exclusions of any insurance plan before making a decision, ensuring that their chosen coverage aligns with their unique healthcare needs and financial situation.

Understanding Your Medical Insurance Deductible: What Counts?

You may want to see also

Explore related products

![]()

If you're under 65, you may not be able to buy a Medigap policy or may pay more

Medicare Supplement Insurance, also known as Medigap, is an additional insurance option that individuals on Original Medicare can purchase to help cover out-of-pocket costs. While Medigap is a valuable option for many, there are some restrictions on who can purchase it and when.

One important factor to consider when thinking about purchasing Medigap is age. If you are under 65, you may encounter challenges in buying a Medigap policy or may have to pay higher premiums. This is because federal law does not require insurance companies to sell Medigap policies to individuals under 65. Thus, if you are in this age group, insurance companies have the discretion to deny you a policy if you do not meet their medical underwriting requirements.

There are some exceptions to this rule. For instance, if you are under 65 and have Medicare due to a disability or ESRD, some states may allow you to purchase a Medigap policy. However, even in these cases, you may have to wait until you turn 65 to buy the specific Medigap policy you want.

The best time to purchase a Medigap policy is during your Medigap Open Enrollment Period. This is a one-time, 6-month period that starts when you turn 65 and enroll in Medicare Part B. During this time, you can enroll in any Medigap policy available in your state, and insurance companies cannot deny you coverage due to pre-existing health conditions. If you wait until after this enrollment period ends, you may face limited options and higher costs for Medigap policies.

In conclusion, while Medigap can be a valuable supplement to Original Medicare, it may be difficult to obtain if you are under 65. If you are considering Medigap, it is important to understand your rights and options under federal and state law to make the best decision for your healthcare needs.

Renewing Insurance Medicaid: A Step-by-Step Guide for Quick Approval

You may want to see also

Explore related products

![]()

Medigap policies are standardised and named by letters, e.g. Plan G or Plan K

Medicare Supplement Insurance, also known as Medigap insurance, is an extra insurance policy that can be purchased from a private insurance company. It helps to pay for costs that Original Medicare does not cover. Medigap policies are standardised and named by letters, like Plan G or Plan K, with each lettered plan offering the same benefits regardless of the insurance company. The basic or "core" benefits are included in Policy A, while the other policies include additional benefits on top of the core offering.

Standardisation of Medigap policies means that insurance companies must offer the same benefits for each plan. The only difference between policies with the same letter sold by different companies is the price. This mandatory standardisation was a result of the Omnibus Budget Reconciliation Act of 1990, with Congress passing legislation to ensure uniformity across the United States.

In most states, Medigap policies are named by letters, providing clear and consistent labels for each plan. It is important to note that individuals must buy separate Medigap policies for themselves and their spouses, as the policy will not cover a spouse's healthcare costs. Additionally, some Medigap policies offer coverage when travelling outside the US, but it is essential to compare policies as costs can vary.

While Medigap policies are standardised, individuals covered by older, non-standardised plans are allowed to keep them. However, due to the risk of duplicate coverage and unnecessary costs, it is recommended that those with access to older policies consider switching to a new standardised plan. This decision should be made by comparing the benefits and costs of the available policies to ensure an informed choice.

Dental Care and Hypercalcemia: Insurance Coverage Explained

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare.

No, it is not mandatory to have Medicare Supplement Insurance. Medicare Supplement Insurance is optional and is meant to help cover some of the "gaps" in Medicare coverage. If you have other health coverage, you may not need Medicare Supplement Insurance.

Generally, you must have Original Medicare (Part A and Part B) to buy a Medigap policy. If you're under 65, you may not be able to buy a Medigap policy or you may have to pay more.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)