Medicare Advantage refers to a situation where an individual has multiple sources of insurance coverage, such as employer-sponsored health insurance, worker's compensation, or liability insurance, and Medicare serves as the secondary payer. In such cases, Medicare provides coverage for healthcare costs only after the primary payer has paid up to the limits of its coverage. The primary payer is typically the insurance or coverage that pays first for an individual's healthcare services, such as employer-based insurance or group health plans. The determination of whether Medicare is the primary or secondary payer depends on factors such as the nature of one's healthcare coverage, employment status, and the specific circumstances of the medical services received.

| Characteristics | Values |

|---|---|

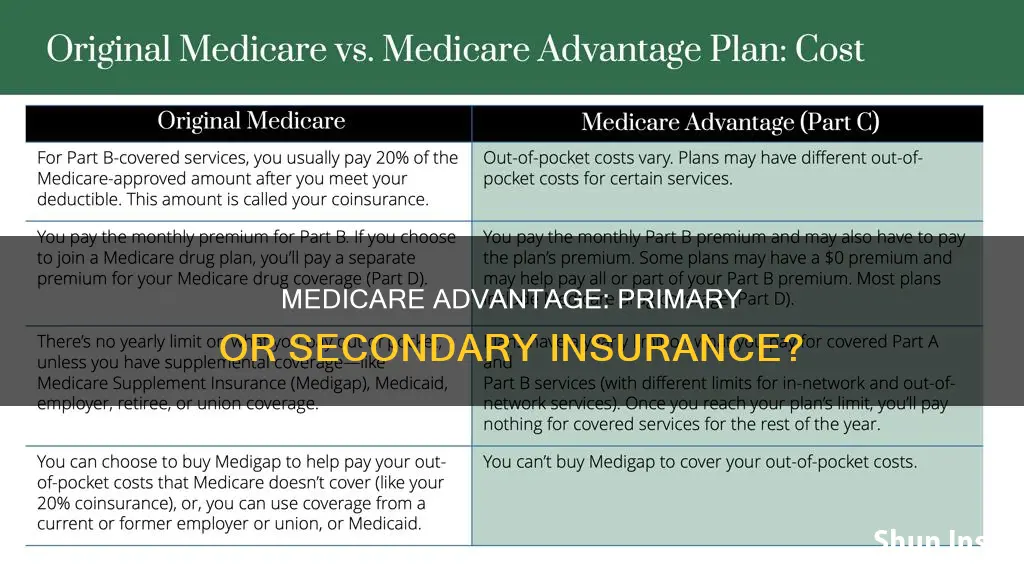

| Nature of Medicare Advantage | Medicare Advantage is a type of Medicare coverage that combines Part A (Hospital Insurance) and Part B (Medical Insurance) and is offered by private companies. |

| Primary vs. Secondary Payer | The determination of whether Medicare Advantage is primary or secondary insurance depends on various factors, including the nature of your healthcare coverage, your employment status, and the specific circumstances of the medical services received. |

| Primary Payer | The primary payer is the insurance or coverage that pays first for your healthcare services. This could be employer-based insurance, group health plans, or other sources of coverage. |

| Secondary Payer | Medicare Advantage becomes the secondary payer when there is another insurance source that is the primary payer. It pays for eligible healthcare services only after the primary payer has covered its share. |

| Coordination of Benefits | When Medicare Advantage is the secondary payer, it coordinates with the primary payer to ensure that claims are paid correctly. If the primary payer does not cover the full cost, Medicare Advantage may cover the remaining balance, reducing out-of-pocket expenses. |

| Role as a Secondary Payer | Medicare Advantage can act as a secondary payer in cases where an individual has multiple sources of insurance coverage, such as employer-sponsored health insurance, worker's compensation, or liability insurance. |

| Conditional Payments | In certain situations, Medicare Advantage may make a conditional payment, covering costs that the primary payer should have paid. However, these conditional payments must be repaid to Medicare Advantage when a settlement, judgment, or other payment is made. |

Explore related products

What You'll Learn

![]()

Medicare Advantage as a secondary payer

The determination of whether Medicare Advantage serves as the primary or secondary payer depends on various factors, including the nature of your healthcare coverage, your employment status, and the specific circumstances of the medical services you receive.

For example, if you have non-tribal group health plan coverage through an employer who has 20 or more employees, the non-tribal group health plan pays first, and Medicare pays second. On the other hand, if your employer has fewer than 20 employees, Medicare pays first, and the non-tribal group health plan pays second.

It is important to inform your doctor and other healthcare providers if you have coverage in addition to Medicare Advantage so that they can send your bills to the correct payer and avoid delays.

Prolotherapy: Is This Treatment Covered by Insurance?

You may want to see also

Explore related products

![]()

Primary payer vs. secondary payer

Medicare Advantage is a type of Medicare plan offered by private companies that contract with Medicare. It is an alternative to Original Medicare, which is the traditional fee-for-service health insurance program offered directly by the federal government. When it comes to Medicare and other types of insurance, the concept of "primary payer" and "secondary payer" comes into play.

The primary payer is the insurance that pays first for your medical bills. It pays up to the limits of its coverage. The secondary payer comes into play if there are any remaining costs that the primary insurance didn't cover. The secondary payer will pay some or all of the remaining costs, such as deductibles, copayments, or coinsurance.

If you have Medicare and another form of health insurance, such as group health coverage, retiree coverage, or Medicaid, each type of coverage is considered a payer. The primary payer will pay up to its coverage limits and then send the remaining balance to the secondary payer. If the secondary payer doesn't cover the entire remaining balance, you may be responsible for any leftover costs.

In some cases, Medicare may make a conditional payment if the primary payer does not pay promptly. However, Medicare will then recover any payments that the primary payer should have made. This order of payment is called "coordination of benefits."

It's important to note that the distinction between primary and secondary payers depends on the specific insurance plans involved and the circumstances of the individual's coverage. To understand how your insurance plans coordinate benefits, it's recommended to contact your insurance provider or Medicare's Benefits Coordination & Recovery Center (BCRC).

Vasectomy Coverage: Understanding Your Medical Insurance Options

You may want to see also

Explore related products

![]()

Medicare's role as a secondary payer

The concept of primary and secondary payers comes into play when determining the order of payment. The primary payer, which could be another insurance plan or Medicare itself, pays up to the limits of its coverage. If there is any remaining balance, the secondary payer, in this case, Medicare, covers the remaining costs. However, it is important to note that the secondary payer may not always cover all the remaining costs, and the individual might be responsible for any unpaid portions.

Medicare Secondary Payer (MSP) is a term used when Medicare does not have primary payment responsibility. This situation arises when another entity, such as other insurance coverage, is responsible for paying before Medicare. For example, when Medicare began in 1966, it was the primary payer for all claims except those covered by specific programs like Workers' Compensation and Veteran's Administration (VA) benefits.

In 1980, Congress passed legislation designating Medicare as the secondary payer to certain primary plans. This shift aimed to transfer costs from Medicare to appropriate private payment sources, protecting the Medicare Trust Funds. As a secondary payer, Medicare helps reduce out-of-pocket expenses by covering expenses that primary insurance might not fully cover.

Maximizing Tax Returns: Claiming Medical Insurance Premiums

You may want to see also

Explore related products

![]()

Medicare as a primary payer

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limit of its coverage and then sends the remaining balance to the "secondary payer". If the "secondary payer" doesn't cover the remaining balance, the beneficiary may be responsible for the rest of the costs. This order of payment is called "coordination of benefits". Medicare may be the primary payer, and your employer the secondary payer, in which case you'll need to join Medicare Part B before your employer insurance will pay for Part B.

Medicare doesn't automatically know if you have other coverage. However, your insurers must report to Medicare when they're the primary payer on your medical claims. In some situations, your healthcare provider, employer, or insurer may ask questions about your current coverage and report that information to Medicare. You may also be asked about other coverage at the time of enrolment.

If you have additional questions about who pays your Medicare bills first, contact your insurance provider or call Medicare's Benefits Coordination & Recovery Center (BCRC) at 855-798-2627 (TTY: 855-797-2627). Licensed Humana sales agents are available Monday–Friday, 8 a.m.–8 p.m.

It's important to tell your doctor and other healthcare providers if you have coverage in addition to Medicare. This will help them send your bills to the correct payer and avoid delays.

Strategies for Selling Medical Insurance: Tips and Tricks

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare's coordination with primary insurance

Medicare is a federal program that provides health insurance coverage for individuals aged 65 and older, as well as some younger people with disabilities or end-stage renal disease (ESRD). When an individual has Medicare and another form of health insurance, such as employer coverage, retiree coverage, or Medicaid, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the remaining balance to the "secondary payer".

The determination of which insurance is the primary payer and which is the secondary payer depends on several factors, including the type of other insurance coverage and the specific situation. For example, if an individual has a non-tribal group health plan through an employer with 20 or more employees, the non-tribal group health plan pays first, and Medicare pays second. On the other hand, if the employer has fewer than 20 employees, Medicare pays first, and the non-tribal group health plan pays second.

In some cases, Medicare may make a conditional payment if the primary payer does not pay the claim promptly or if there is an issue with the claim. For instance, if an individual has a workers' compensation claim, Medicare may make a conditional payment pending the insurance company's review of the claim. However, Medicare will then recover any payments that the primary payer should have made.

It is important to note that Medicare Advantage, also known as Part C, is an alternative way to receive Medicare coverage through a private company. Medicare Advantage plans often include Part D prescription drug coverage, and individuals with Medicare Advantage may not be able to join a separate Medicare drug plan.

If individuals have questions about the coordination of benefits or who pays first in their specific situation, they can contact their insurance provider or Medicare's Benefits Coordination & Recovery Center (BCRC) for assistance. Licensed sales agents are available to help individuals understand their coverage options and how Medicare coordinates with other insurance.

Pittsburgh: Get Medical Help Without Insurance

You may want to see also

Frequently asked questions

The primary payer is the insurance or coverage that pays first for your healthcare services. This could be employer-based insurance, group health plans, or other sources of coverage.

The insurance that pays second (secondary payer) only pays if there are costs the primary insurance didn't cover.

Medicare is the primary payer for beneficiaries who are not covered by other types of health insurance or coverage. For example, if you have non-tribal group health plan coverage through an employer who has fewer than 20 employees, Medicare pays first, and the non-tribal group health plan pays second.

Medicare becomes the secondary payer when there is another insurance source that is the primary payer. For example, if you have non-tribal group health plan coverage through an employer who has 20 or more employees, the non-tribal group health plan pays first, and Medicare pays second.

The Benefits Coordination & Recovery Center (BCRC) investigates claims and requests repayment from you or your plan.