Medicare is a federal program that helps retired people with their healthcare costs. It is available to people from the age of 65, although there are some exceptions for those with disabilities. If you are still working at 65, you may be able to delay enrolling in Medicare without penalty. However, if you retire before 65, you may need to purchase health insurance from a private insurer or the government's Health Insurance Marketplace. If you have retiree coverage, it's important to understand how it works with Medicare, as you may need to enroll in both Medicare Part A and Part B to get full benefits.

| Characteristics | Values |

|---|---|

| Medicare eligibility age | 65 years |

| Medicare enrollment | Automatic |

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part D | Drug coverage |

| Medicare Advantage | Medicare Part C |

| Medicare Supplement Insurance | Medigap |

| Medicare costs | Monthly fee and other out-of-pocket costs |

| Medicare and retiree coverage | Medicare pays first |

| Losing job-based coverage | Special Enrollment Period |

| Medicare and employer coverage | May continue with employer coverage |

| Medicare and spouse | Spouse not covered unless eligible |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

Medicare eligibility and age

Medicare is health insurance for people aged 65 or older. You can sign up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) starting three months before you turn 65 and ending three months after you turn 65. If you don't sign up when you're first eligible, you may have to pay a monthly penalty for as long as you have Part B, and this penalty increases the longer you wait to sign up.

There are some exceptions to the age requirement. You may be eligible for Medicare before you turn 65 if you have a disability, End-Stage Renal Disease (ESRD), or Amyotrophic Lateral Sclerosis (ALS), also called Lou Gehrig's disease. If you have End-Stage Renal Disease, you may qualify for premium-free Part A if you receive regular dialysis treatments or a kidney transplant, have filed an application for Medicare, and meet certain conditions. If your disability is ALS, you are entitled to Part A the first month you are entitled to Social Security or Railroad Retirement Board (RRB) disability cash benefits. If you are a disabled federal, state, or local government employee who is not eligible for monthly Social Security or RRB benefits, you may be automatically entitled to Part A after being disabled for 29 months.

If you retire before you turn 65 and lose your job-based health plan, you can use the Health Insurance Marketplace to buy a plan. If you have retiree health coverage, you may be able to keep it, but it's important to check whether you will lose this coverage if you get Medicare. If you have both Medicare and retiree coverage, Medicare typically pays for your healthcare first. Your job may offer health coverage when you retire, so it's a good idea to talk to your job's benefits administrator to find out.

Medicare Replacement Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare and retiree coverage

Medicare is a federal program that helps you pay for healthcare once you turn 65. If you retire before the age of 65, you may be able to continue to get health insurance through your employer, or you can purchase coverage from a private insurance company in the meantime. If you have retiree health coverage, you have different options to consider. For example, if you have retiree coverage from a previous job, it may not pay for your health services if you don't also have Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). If you have both Medicare and retiree coverage, Medicare typically pays first for your healthcare bills.

If you have a Health Savings Account (HSA), you and your employer should stop contributing to your HSA six months before you retire or apply for Social Security benefits. After you sign up for Part A and Part B, you can choose how you get your coverage. Once you're eligible for Medicare and enroll, you can no longer contribute to an HSA, but you can draw on your HSA funds to pay certain Medicare premiums and out-of-pocket medical expenses.

If you retire early, you will be responsible for the full cost of your premiums until you become eligible for Medicare at 65. You may be able to get other types of health insurance coverage, such as through the Affordable Care Act Marketplace, or a private company. If you have retiree insurance, you may want to contact your State Health Insurance Assistance Program (SHIP) for free advice about whether to buy a Medigap policy.

If you continue working after age 65, different rules apply. How and when you sign up will depend on what kind of insurance coverage you have through your employer. If you're currently working, you can get Medicare within an 8-month period after retirement or after opting out of your employer's group health insurance plan and still avoid penalties.

Life Insurance Medical Exams: What They Test For

You may want to see also

Explore related products

$6.89 $14.99

![]()

Medicare and private insurance

Medicare is a public health insurance program provided by the government. When you retire, Medicare can be your primary or secondary insurance. If you have both Medicare and private insurance, a process called "coordination of benefits" determines which insurance provider pays first. This provider is called the "primary payer". The primary payer pays for any covered services until the coverage limit has been reached. The "secondary payer" pays for the costs that the primary payer doesn't cover.

If you have private insurance through your employer, you can keep it as your primary insurance and enrol in Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) to get full benefits from your retiree coverage. You can also choose to join a Medicare drug plan when you sign up for Medicare Part A and/or Part B. If you don't join a Medicare drug plan, you'll need to have creditable drug coverage to avoid paying a Part D late enrolment penalty.

If you don't have retiree insurance or Medicare, you can use the Health Insurance Marketplace to buy an insurance plan. Losing job-based coverage qualifies you for a Special Enrollment Period, which means you can enrol in a health plan outside of the yearly period when people can enrol in a Marketplace health insurance plan. You can also get a Marketplace plan to cover you before your Medicare begins. You can then cancel the Marketplace plan once your Medicare coverage starts.

If you retire early, you may want to consider enrolling in a new employer-sponsored plan by taking on a part-time job that offers healthcare benefits. You can also ask your employer's HR department if you're entitled to continue your existing coverage under COBRA. COBRA coverage typically lasts for up to 18 months after you leave your job, but your coverage will likely end once you get Medicare.

Dubai Medical Insurance: Understanding Individual Premium Costs

You may want to see also

Explore related products

![]()

Medicare and employer-sponsored plans

If you have both Medicare and retiree coverage from an employer, Medicare typically pays first for your healthcare bills, and your retiree plan pays second. This is called the "coordination of benefits". If you have a high-deductible health plan with a Health Savings Account (HSA) and want to continue contributing to it, you should not enrol in Medicare Part A. However, you can still withdraw money from your HSA after your Medicare coverage starts and use it to pay for qualified medical expenses.

If you retire before you are 65 and lose your job-based health plan, you can use the Health Insurance Marketplace to buy a plan. Losing health coverage qualifies you for a Special Enrollment Period, meaning you can enrol in a health plan outside of the yearly period (November 1-January 15). You can then cancel the Marketplace plan once your Medicare coverage starts.

It is important to do your research to decide on the most cost-effective coverage option and avoid any Medicare late enrolment penalties. You should also consider the size of your employer when coordinating your Medicare benefits with large employer coverage. If you are still actively working for a large employer, their group insurance pays primary, and Medicare pays secondary. However, if you are on COBRA, Medicare pays first, and COBRA pays second.

Switching Insurance: When Can You Change Medicaid Providers?

You may want to see also

Explore related products

![]()

Medicare and out-of-pocket costs

When it comes to Medicare and out-of-pocket costs, there are a few key things to keep in mind. Firstly, it's important to understand what is meant by "out-of-pocket" costs. These are the expenses that you are responsible for paying beyond what Medicare covers. Out-of-pocket costs can include deductibles, copayments, and coinsurance. For example, Medicare Part B, which covers medical insurance, has a standard monthly premium of $185 as of 2025, with a deductible of $257 per year. The Part B coinsurance is 20% of the cost for each Medicare-approved service or item, which can make up a significant portion of your out-of-pocket expenses.

Medicare Advantage (Part C) plans offer additional benefits such as dental, hearing, and vision care. While the average monthly premium for these plans is projected to range from $0 to over $240 in 2025, they typically have a fixed copayment for doctor visits instead of the 20% coinsurance of Part B. It's worth noting that some Medicare Advantage plans have no deductible, but they may cost more in monthly premiums.

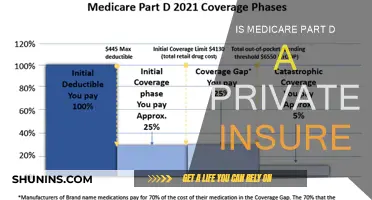

Medicare Part D covers prescription drugs, and the annual premiums for these plans vary, with an average of about $46.50 per month for standard coverage in 2025. The Part D deductible cannot exceed $590 per year, and there is an out-of-pocket maximum of $2,000. After reaching this limit, you won't have to pay anything for covered drugs for the rest of the year.

Additionally, Medigap (Supplemental Insurance) policies can be purchased from private carriers to cover costs associated with Medicare Parts A and B. The premium prices for Medigap policies are set by the insurance carriers, and these prices determine your out-of-pocket costs.

It's important to note that Medicare costs can change annually, and there are different plans available with varying levels of coverage and out-of-pocket expenses. Therefore, it's recommended to carefully review the available plans and choose the one that best suits your needs and budget.

Get Covered: Aetna Medical Insurance Application Process

You may want to see also

Frequently asked questions

The minimum age to be eligible for Medicare is 65. However, if you have a disability, you may be able to get Medicare before turning 65.

If you retire before turning 65, you may not be eligible for Medicare. In this case, you can explore other options such as continuing your employer's insurance plan, purchasing private insurance, or enrolling in a new employer-sponsored plan by taking on a part-time job that offers healthcare benefits.

If you have both Medicare and retiree coverage, Medicare typically pays first for your healthcare expenses. Any remaining amount not covered by Medicare will then be submitted to your retiree plan.