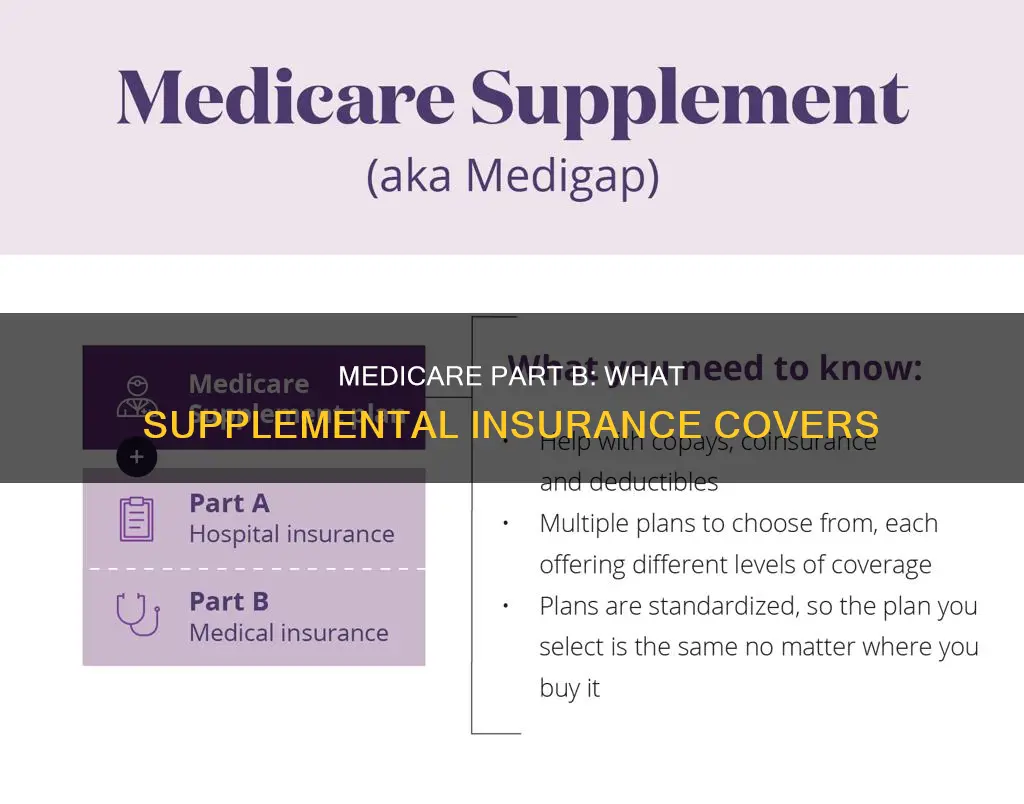

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased to help cover expenses that Original Medicare (Part A and Part B) does not. Medigap Plan B, specifically, helps cover out-of-pocket expenses such as deductibles, copayments, and coinsurance associated with Original Medicare. It is important to note that Medigap Plan B is different from Medicare Part B, which is part of Original Medicare, and that Plan B does not cover prescription drugs or skilled nursing facility stays. The best time to enroll in Medigap Plan B is during the six-month Medicare Supplement Open Enrollment Period, which begins when an individual turns 65 and enrolls in Medicare Part B.

| Characteristics | Values |

|---|---|

| What is Medicare Part B Supplemental Insurance? | Medicare Supplement Insurance (also known as Medigap) is extra insurance to help cover expenses that Original Medicare (Part A and Part B) may leave you with. |

| Who can apply? | Anyone eligible for Medicare can apply for a Medicare Supplement Insurance plan all year round. |

| When is the best time to apply? | The best time to enroll is during the Medicare Supplement Open Enrollment period, which is a six-month period that starts on the first day of the month when you turn 65 or older and are enrolled in Medicare Part B. |

| What does Plan B cover? | Medicare Supplement Plan B covers Part A and Part B coinsurance and copayments, the first three pints of transfused blood, Part A hospice care coinsurance or copayment, and the Part A deductible. |

| What isn't covered by Plan B? | Plan B does not cover the Part B annual deductible, Part B excess charges, skilled nursing facility stays, or emergency healthcare during foreign travel. |

| How is Plan B different from other plans? | Plan B is one of the most cost-conscious plans but provides minimal coverage. More comprehensive plans include Plans F and C, while Plans G and D are similar but do not cover the Part B deductible. |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is additional insurance that can be purchased from a private health insurance company. This insurance helps to cover out-of-pocket costs that arise with Original Medicare, which consists of Part A (Hospital Insurance) and Part B (Medical Insurance). It is important to note that Medigap is not the same as Medicare Part B. While Medicare Part B is a component of Original Medicare, Medigap Plan B is a type of supplemental insurance that fills the gaps in coverage left by Original Medicare.

Medigap Plan B specifically covers out-of-pocket expenses related to Medicare Part B, such as copayments and coinsurance. It is designed to alleviate the financial burden that may result from these additional costs. The coverage provided by Medigap Plan B ensures that individuals can access the medical services they need without worrying about the associated deductibles, copayments, or coinsurance.

Eligibility and enrollment for Medigap plans may vary. Generally, individuals must already have Original Medicare, including Part A and Part B, to purchase a Medigap policy. The best time to enroll in Medigap Plan B is often during the Medicare Supplement Open Enrollment Period, which starts when an individual turns 65 and enrolls in Medicare Part B. This period lasts for six months, and it guarantees acceptance into a Medigap plan without considering pre-existing health conditions.

It is important to be mindful of the specific Medigap plans available in your area, as they may differ. Additionally, enrollment periods and contract renewals may impact when you can sign up for a Medigap plan. If you miss the open enrollment period, you may still apply for Medigap Plan B or other Medigap plans at any time during the year, but there is a risk of coverage denial or higher premiums.

Medical Insurance: A Necessary Investment for Your Health?

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

![]()

Medigap Plan B coverage

Medicare Supplement Plan B, also known as Medigap Plan B, provides basic benefits and covers the Medicare Part A deductible. Medigap plans help pay for the out-of-pocket costs associated with Original Medicare, including copays, coinsurance, and deductibles. Medigap Plan B covers:

- Part A coinsurance and hospital costs for up to an additional 365 days after Medicare benefits are used up.

- Part B coinsurance or copayment.

- The first three pints of transfused blood.

- Part A hospice care coinsurance or copayment.

- Part A deductible.

Medigap Plan B does not cover the Part B annual deductible, Part B excess charges, skilled nursing facility stays, or emergency healthcare during foreign travel. It's important to note that Medigap Plan B policies cover the same expenses regardless of the company's plan chosen. The best time to buy a Medigap Plan B policy is during the six-month open enrollment period that begins when you turn 65 and enroll in Medicare Part B. During this period, insurance companies cannot reject enrollment for health reasons or charge higher premiums based on pre-existing conditions. After this period, you may be denied coverage or face higher premiums due to your health status or medical history.

Medigap Plan B is not available in all states. Massachusetts, Minnesota, and Wisconsin have their own standardized Medigap plans, so it's important to check the specific rules and offerings in your state. Additionally, if you have a Medicare Advantage plan, you cannot purchase a Medigap plan.

Crystal Run Medical: Understanding Their Accepted Insurance Plans

You may want to see also

Explore related products

![]()

Medigap vs Medicare Part B

Medicare is federal health insurance for anyone aged 65 and over and some people under 65 with certain disabilities or conditions. Medicare Part B is one of the two parts of Original Medicare, the other being Part A.

Medigap, or Medicare Supplement Insurance, is extra insurance provided by private health insurance companies to help pay your share of out-of-pocket costs in Original Medicare. Generally, you must have Original Medicare (Parts A and B) to buy a Medigap policy. A Medigap policy only covers one person, so spouses would each have to buy their own policy.

Medigap policies can be purchased in addition to Original Medicare, but not alongside a Medicare Advantage Plan (Part C). Medicare Advantage is a bundled plan that includes Parts A, B, and usually Part D (prescription drug coverage). Medicare Advantage is offered by private companies as an alternative to Original Medicare, and often has different out-of-pocket costs and extra benefits.

Medigap policies are automatically renewed annually as long as you pay your premiums, and you can keep your policy even if your health deteriorates. If you drop a Medigap policy to join a Medicare Advantage Plan, you have a 12-month trial period during which you can switch back to Medigap. Medigap policies purchased after 2005 do not include prescription drug coverage, but you can join a separate Medicare drug plan (Part D) to cover prescription drugs.

UCDavis Medical Group: What Insurance Plans Are Accepted?

You may want to see also

Explore related products

![]()

Medicare Supplement Plan A

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can purchase from a private health insurance company to help cover your share of out-of-pocket costs in Original Medicare (Parts A and B). Medicare Supplement Plan A is a baseline Medigap plan with no extras, covering only the basics. It is important to note that Plan A does not cover the Part B deductible, prescription drugs, long-term care, dental or vision care, or private-duty nursing.

Medigap Plan A covers certain out-of-pocket expenses associated with Medicare Parts A and B, including copays and coinsurance. It provides basic, minimum coverage for costs not paid by Medicare Parts A and B, such as hospitalisation coinsurance and coverage for 365 additional days after Medicare benefits end. It also pays for the first 3 pints of blood each year and Medicare Part B coinsurance, which is generally 20% of Medicare-approved expenses or copayments for hospital outpatient services.

Plan A may be a good choice for individuals who only need limited assistance with copays and coinsurance. It sometimes offers lower premiums than higher-coverage options, but this is not always the case. The premium rates can vary depending on factors such as age, location, gender, and overall health. It is worth noting that Plan G and Plan N are more popular choices among new members.

If you are considering enrolling in Medicare Supplement Plan A, it is important to review the specific coverage details offered by different insurance companies. You can also explore potential discounts, such as online application discounts or healthy rewards programs, to save up to 25% on premiums. Additionally, keep in mind that Plan A may not be suitable if you require more comprehensive coverage, as switching to a different plan with more benefits may require passing medical underwriting.

In conclusion, Medicare Supplement Plan A is a basic option for those seeking to fill the gaps in their Original Medicare coverage. While it covers essential out-of-pocket expenses, it lacks the additional benefits offered by other Medigap plans. Therefore, it is important to carefully consider your personal needs and compare Plan A with other available options before making a decision.

Medical Coverage at The Good Feet Store: What's Covered?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare Advantage plans

Most Medicare Advantage Plans include drug coverage (Part D). There are several types of Medicare Advantage Plans, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Special Needs Plans (SNPs), Medicare Medical Savings Accounts (MSAs), and Private Fee-for-Service Plans (PFFS).

It is important to note that you can be disenrolled from a Medicare Advantage Plan for various reasons, such as moving outside the plan's service area, losing Medicare or Medicaid eligibility, joining a drug plan (in some cases), or if the plan's contract with Medicare ends. Before enrolling in a Medicare Advantage Plan, it is recommended to consult your employer, union, or benefits administrator to understand the potential impact on your existing coverage.

Medigap, or Medicare Supplement Insurance, is an additional type of insurance that can be purchased from a private health insurance company. It helps cover the out-of-pocket costs associated with Original Medicare, including deductibles, copayments, and coinsurance. Medigap Plan B specifically covers Medicare Part B out-of-pocket expenses and is designed to fill the gaps in coverage left by Original Medicare (Part A and Part B).

The enrollment period for Medigap Plan B begins when an individual turns 65 and enrolls in Medicare Part B, lasting for six months. During this period, beneficiaries cannot be denied coverage or charged higher premiums based on pre-existing health conditions. However, missing the open enrollment period may result in coverage denial or higher premiums.

Navigating Medical Insurance Coverage for LASIK Surgery

You may want to see also

Frequently asked questions

Medicare Part B Supplemental Insurance, also known as Medigap Plan B, is an insurance plan that covers the gaps in Original Medicare (Part A and Part B) coverage.

Medicare Part B Supplemental Insurance covers Part A and Part B coinsurance, copayments, the first three pints of transfused blood, Part A hospice care coinsurance or copayment, and the Part A deductible.

Medicare Part B Supplemental Insurance does not cover the Part B annual deductible, Part B excess charges, skilled nursing facility stays, or emergency healthcare during foreign travel.

You can enrol in Medicare Part B Supplemental Insurance during your Open Enrollment Period, which is a six-month period starting the first day of the month in which you turn 65 or older and are enrolled in Medicare Part B. You can also apply for the insurance plan any time during the year, but you may be subject to coverage denial or higher premiums.

Yes, Medicare Part B Supplemental Insurance is also known as Medigap. Medigap is extra insurance purchased from a private health insurance company to cover out-of-pocket costs in Original Medicare.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)