Medicare Part B is an insurance plan that covers medically necessary services and preventive services. While Part B can be helpful, it does not have a maximum out-of-pocket cap, which means there is no limit to what you could owe in copays and coinsurance. To avoid the potential financial risk, you can purchase Medicare Supplement Insurance, also known as Medigap, which is extra insurance that can be bought to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies can help fill in the gaps in Medicare Part A and Part B, which could save you thousands of dollars per year. However, Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

| Characteristics | Values |

|---|---|

| What is Medicare Part B? | Medical Insurance that helps cover 2 types of services: medically necessary services and preventive services. |

| What is Medicare Supplement Insurance (Medigap)? | Extra insurance that can be purchased from a private company to help pay your share of out-of-pocket costs in Original Medicare (Part A and Part B). |

| Is Medigap worth it? | Medigap is optional but can help fill "gaps" in Medicare Part A and Part B, which could otherwise be costly. About 41% of Original Medicare beneficiaries had Medigap in 2022. Medigap can put a cap on your yearly costs by paying more upfront for premiums. |

| When to buy Medigap? | Your six-month Medigap open enrollment period starts when you turn 65 and enroll in Medicare Part B. After this period, it may be more expensive or challenging to obtain a Medigap policy. |

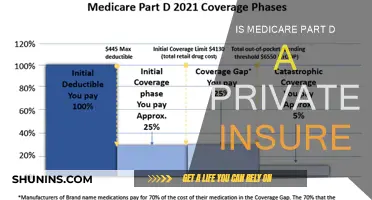

| Cost of Medicare | The cost of Medicare varies based on coverage, services, and providers. Generally, you pay a monthly premium and a portion of the costs each time you use a covered service. Medicare Part A had a deductible of $1,632 in 2024. |

Explore related products

What You'll Learn

- Medicare Part B covers medically necessary and preventive services

- Medicare Supplement Insurance (Medigap) is extra insurance to cover out-of-pocket costs

- Medigap policies do not cover long-term care, vision, dental, or prescription drugs

- You must have Part A and Part B to buy a Medigap policy

- Medigap policies can help limit yearly out-of-pocket costs

![]()

Medicare Part B covers medically necessary and preventive services

Medicare Part B is the part of Medicare that covers medically necessary and preventive services. This includes services or supplies that meet accepted standards of medical practice to diagnose or treat a medical condition, such as an illness or injury. It also covers preventive care, such as flu shots or other vaccinations, and early illness detection services.

Medicare Part B is considered "medical insurance" and is one of two parts of "original Medicare," the other being Part A, which is "hospital insurance." Together, Parts A and B make up the core of Medicare, and you need to have both to join a Medicare Advantage Plan. Once you have signed up for both Part A and Part B, you can choose between Original Medicare and Medicare Advantage.

Medicare Part B covers a range of services and supplies that are considered medically necessary to diagnose or treat a medical condition. This includes doctor's services, outpatient care, durable medical equipment, home health services, and some preventive services. For example, if you use an insulin pump that is covered under Part B's durable medical equipment benefit, your cost for a month's supply of Part B-covered insulin for your pump cannot be more than $35.

Medicare Part B also covers some preventive services, which are designed to prevent illness or detect it in its early stages when treatment is most likely to be successful. Most preventive services are free if you get them from a healthcare provider who accepts Medicare assignments. Examples of covered preventive services include flu shots, other common vaccinations, and some screening tests, such as mammograms and colonoscopies.

While Medicare Part B covers a wide range of medically necessary and preventive services, it does not cover everything. In particular, it does not cover most dental, vision, or hearing services, and it does not cover prescription drugs. This is where Medicare Supplement Insurance, also known as Medigap, comes in. Medigap is extra insurance that you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare. It can fill in some of the "gaps" in Medicare Part A and Part B, which could otherwise cost thousands of dollars per year.

Tail Coverage: Medical Malpractice Insurance Explained

You may want to see also

Explore related products

![]()

Medicare Supplement Insurance (Medigap) is extra insurance to cover out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is additional insurance that you can purchase from a private insurance company. It helps cover your share of out-of-pocket costs in Original Medicare (Part A and Part B). Medigap policies are designed to fill the gaps in coverage provided by Original Medicare, and they offer a range of benefits to meet different needs.

Generally, to be eligible for Medigap, you must have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medigap is not available to those under 65, and even if you are eligible, it is important to be aware of potential issues with insurance companies and to protect yourself when shopping for a Medigap policy.

There are two important timing considerations for purchasing Medigap. Firstly, you have a 6-month Medigap Open Enrollment period, which starts in the first month you have Medicare Part B and you are 65 or older. During this time, you are guaranteed the right to buy any Medigap policy, regardless of pre-existing health conditions. Secondly, if you do not purchase a Medigap policy within this 6-month window, you may find it difficult or expensive to purchase a policy later.

Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits, regardless of the insurance company. The price is usually the only difference between policies with the same letter sold by different companies. There are 10 different types of Medigap plans offered in most states, named by letters A-D, F, G, and K-N. Some Medigap policies even offer coverage for emergency medical care when travelling outside the U.S. However, it is important to note that Medigap generally does not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Affordable Thyroid Medication: Clinics for the Uninsured

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

![]()

Medigap policies do not cover long-term care, vision, dental, or prescription drugs

Medicare Supplement Insurance, or Medigap, is an additional insurance policy that can be purchased from a private company to help cover out-of-pocket costs in Original Medicare. Medigap policies typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Long-term care, such as nursing home stays, is not covered by Medigap policies. If you require long-term care, you may need to explore alternative options, such as long-term care insurance or other specialised programmes.

Vision care is also generally excluded from Medigap coverage. This means that routine eye exams, eyeglasses, and other vision-related services may not be covered. However, it is important to note that Medicare Part B does cover specific vision-related services, such as cataract surgery, vision correction after surgery, and glaucoma screenings for high-risk individuals.

Similarly, Medigap policies typically do not include dental coverage for routine dental care, such as dental cleanings, exams, and fillings. However, Medicare Part B will cover dental costs associated with another covered service, such as jaw surgery in a hospital.

Medigap plans also generally exclude coverage for prescription drugs. If you require prescription drug coverage, you may need to enrol in a separate Medicare drug plan (Part D).

While Medigap policies do not typically cover these areas, some insurers have introduced ways to include them. For example, some companies offer "`stand-alone`" dental and vision insurance plans that can be purchased alongside a Medigap policy. Additionally, some Medigap plans may offer dental or vision benefits as a rider or "add-on" to the standard policy. These benefits may provide coverage for routine dental and vision care. However, it is important to carefully consider the specific details of any Medigap policy and its associated costs before making a decision.

Understanding Medicare B and Private Insurance Coordination

You may want to see also

Explore related products

![]()

You must have Part A and Part B to buy a Medigap policy

Medicare Part A and Part B have no maximum out-of-pocket caps, meaning there is no limit to how much you could owe as copays and coinsurance add up. This is where Medicare Supplement Insurance, or Medigap, comes in. Medigap is extra insurance that you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare. Generally, you must have Original Medicare – Part A (Hospital Insurance) and Part B (Medical Insurance) – to buy a Medigap policy. In other words, you need to be enrolled in both Part A and Part B to be eligible to buy a Medigap policy.

Medigap policies fill in the "gaps" in Medicare Part A and Part B. For example, Medicare Part A has a deductible of $1,632 in 2024, which you owe before Medicare starts to pay for inpatient hospital care. Without Medigap, you would be responsible for paying this deductible yourself. Medigap policies can also help with other out-of-pocket costs, such as copays and coinsurance, which can add up quickly without a cap on how much you can owe.

It is important to note that Medigap is not mandatory, and you can choose to rely solely on Original Medicare (Part A and Part B) for your health coverage. However, if you decide you want to purchase a Medigap policy, it is generally recommended to do so within six months of enrolling in Part B. This is because insurance companies cannot use medical underwriting to charge you more or deny coverage during this initial six-month period. After this open enrollment period ends, it can be more expensive or even impossible to get a Medigap policy.

In addition, there are some limitations to what Medigap covers. For example, Medigap policies typically do not cover long-term care (such as care in a nursing home), vision, dental, hearing aids, private-duty nursing, or prescription drugs. If you require coverage for these services, you may need to explore other options, such as separate Medicare drug plans or Medicare Advantage Plans.

Calculating Pre-Tax Medical Insurance: Understanding the Process

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medigap policies can help limit yearly out-of-pocket costs

Medigap, or Medicare Supplement Insurance, is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. It is important to note that Medigap policies generally require you to have both Medicare Part A and Part B. Medigap policies work alongside your Original Medicare coverage to reduce your out-of-pocket expenses. This means that Medicare will pay for its share of Medicare-approved costs that Original Medicare typically does not cover.

Medigap Out-of-Pocket Maximums act as a safety net, setting a limit on the total amount a policyholder must pay for covered services within a year. Once the policyholder reaches this maximum amount, the Medigap plan typically covers all additional Medicare-approved expenses. This feature ensures that individuals with Medigap plans do not face unlimited out-of-pocket costs for Medicare-covered services. It is worth noting that not all Medigap plans have an out-of-pocket maximum, and the limits can vary among those that do.

Understanding the out-of-pocket maximums is crucial for evaluating different Medicare Supplement Plans, such as Plans F, G, and N, which offer varying levels of coverage. Plans with broader coverage tend to have higher out-of-pocket maximums but provide better financial protection against unexpected medical costs. When choosing a Medigap plan, it is essential to consider your typical annual healthcare expenses, including doctor visits, hospital stays, and other covered medical services. By focusing on the out-of-pocket maximum cost, you can make more informed decisions about your healthcare needs and budget preferences.

Additionally, Medigap policies can make healthcare costs more predictable by spreading expenses over the year through monthly premium payments, reducing the burden of large, unexpected medical bills. However, it is important to remember that Medigap plans generally do not include prescription drug coverage, and you may need to enroll in a separate Medicare Part D plan if you require medication.

Medical Insurance Companies: Giants of the Industry

You may want to see also

Frequently asked questions

Medicare Part B is Medical Insurance that helps cover medically necessary services and preventive services.

Medicare Supplement Insurance, or Medigap, is extra insurance you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare (Part A and Part B).

Medicare Supplement Insurance is not mandatory, but it can help fill "gaps" in Medicare Part A and Part B coverage, which could save you money in the long run.

Your six-month Medigap open enrollment period starts when you turn 65 and enroll in Medicare Part B. During this period, you cannot be denied coverage or charged more based on your health or medical history. After this period, it may be more difficult and expensive to obtain a Medigap policy.

The cost of a Medigap policy depends on the plan type, age, location, and health status. You can expect to pay $100-$150 per month or more for the most popular Medigap plan, Plan G, when you sign up at age 65.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)