Medigap and supplemental insurance are terms often used interchangeably, but they refer to the same type of coverage designed to fill the gaps in Original Medicare. Specifically, Medigap policies, also known as Medicare Supplement Insurance, are private insurance plans that help pay for out-of-pocket costs such as copayments, coinsurance, and deductibles that Medicare Part A and Part B do not cover. While both terms essentially describe the same product, supplemental insurance is a broader term that can apply to various types of additional coverage beyond Medicare, whereas Medigap is exclusively tied to Medicare-related supplemental plans. Understanding this distinction is crucial for individuals looking to enhance their healthcare coverage and manage expenses effectively.

| Characteristics | Values |

|---|---|

| Definition | Medigap and supplemental insurance are often used interchangeably, but they are not exactly the same. Medigap specifically refers to private insurance policies that supplement Original Medicare (Part A and Part B) by covering costs like copayments, coinsurance, and deductibles. Supplemental insurance is a broader term that can include various types of policies, including Medigap, which cover gaps in primary insurance plans. |

| Purpose | Both aim to cover out-of-pocket expenses not covered by primary insurance. Medigap is exclusively for Medicare beneficiaries, while supplemental insurance can apply to other types of primary insurance, such as employer-sponsored plans. |

| Regulation | Medigap plans are standardized by the federal government and labeled with letters (e.g., Plan G, Plan N). Supplemental insurance policies vary widely and are not federally standardized. |

| Eligibility | Medigap is available only to individuals enrolled in Original Medicare. Supplemental insurance can be purchased by anyone with a primary insurance plan, regardless of whether it’s Medicare, private insurance, or another type. |

| Coverage | Medigap plans offer specific, standardized benefits based on the plan type. Supplemental insurance coverage varies depending on the policy and provider, often including benefits like vision, dental, or critical illness coverage. |

| Cost | Premiums for Medigap plans are generally higher due to their comprehensive coverage of Medicare gaps. Supplemental insurance costs vary widely based on the type and extent of coverage. |

| Enrollment Period | Medigap has a guaranteed issue period (6 months after turning 65 and enrolling in Medicare Part B). Supplemental insurance typically does not have a specific enrollment period and can be purchased at any time. |

| Provider Network | Medigap works with any healthcare provider that accepts Medicare. Supplemental insurance may have specific provider networks depending on the policy. |

| Portability | Medigap policies are portable across states, but premiums may vary. Supplemental insurance portability depends on the specific policy and provider. |

| Examples | Medigap: Plan G, Plan N. Supplemental Insurance: Accident insurance, hospital indemnity insurance, cancer insurance. |

Explore related products

What You'll Learn

- Medigap Definition: Medigap is private insurance covering gaps in Original Medicare, like copays and deductibles

- Supplemental Insurance Overview: Supplemental insurance broadly covers extra costs not included in primary health plans

- Key Differences: Medigap is Medicare-specific, while supplemental insurance can apply to any health plan

- Coverage Comparison: Medigap focuses on Medicare gaps; supplemental insurance varies by policy and provider

- Eligibility Criteria: Medigap requires Medicare enrollment; supplemental insurance has no such requirement

![]()

Medigap Definition: Medigap is private insurance covering gaps in Original Medicare, like copays and deductibles

Medigap, by definition, is a private insurance policy designed to fill the gaps in Original Medicare coverage. These gaps include out-of-pocket costs like copays, coinsurance, and deductibles, which can quickly add up for beneficiaries. For instance, Medicare Part A has a deductible of $1,632 per benefit period in 2023, and Part B requires a $226 annual deductible. Medigap policies, labeled Plan A through Plan N, offer standardized benefits to cover these expenses, ensuring predictability in healthcare costs. This specificity makes Medigap a targeted solution rather than a broad supplemental insurance option.

Consider the practical implications: a 65-year-old Medicare beneficiary without Medigap could face thousands in unexpected costs during a hospital stay. Medigap Plan G, one of the most popular options, covers the Part A deductible and excess charges not covered by Medicare. However, it’s crucial to enroll during the six-month Medigap Open Enrollment Period starting when you turn 65 and have Part B, as insurers may deny coverage or charge higher premiums later. This timing underscores the strategic nature of Medigap as a supplemental tool, not a standalone insurance product.

From a comparative standpoint, Medigap differs from other supplemental insurance in its exclusivity to Medicare beneficiaries. While supplemental insurance broadly refers to any policy that complements primary coverage, Medigap is strictly tied to Original Medicare. For example, a cancer insurance policy might pay a lump sum upon diagnosis, but it’s not tied to Medicare’s structure. Medigap, however, works only with Medicare, covering specific costs like the 20% coinsurance for Part B services. This narrow focus makes it a specialized form of supplemental insurance, not a general add-on.

Persuasively, Medigap’s value lies in its ability to provide peace of mind. For beneficiaries with chronic conditions or those anticipating frequent medical services, the predictable costs of Medigap can be a financial lifeline. Take the example of a beneficiary needing multiple outpatient procedures: without Medigap, the 20% Part B coinsurance could become burdensome. With Medigap, these costs are capped, allowing for better budgeting. However, it’s essential to weigh the monthly premium against potential out-of-pocket savings, as Medigap plans can range from $100 to $300 monthly, depending on location and plan type.

Finally, a descriptive analysis reveals Medigap’s role as a bridge between Medicare’s limitations and beneficiaries’ financial stability. Unlike Medicare Advantage plans, which replace Original Medicare with managed care, Medigap enhances it by covering gaps. For example, if a beneficiary travels frequently, Medigap Plan G or N includes emergency coverage abroad, a benefit Original Medicare lacks. This tailored approach highlights why Medigap is not just supplemental insurance but a specific, Medicare-centric solution. Understanding this distinction ensures beneficiaries choose the right coverage for their needs.

Do You Need Canoe Insurance? Exploring Coverage Options for Paddlers

You may want to see also

Explore related products

![]()

Supplemental Insurance Overview: Supplemental insurance broadly covers extra costs not included in primary health plans

Supplemental insurance steps in where primary health plans leave off, covering costs like copays, deductibles, and even non-medical expenses such as travel or lodging during treatment. For instance, a Medicare beneficiary might face a $1,600 hospital deductible; a Medigap plan (a type of supplemental insurance) could cover this entirely, depending on the policy. This targeted coverage is particularly valuable for individuals with chronic conditions or those anticipating high out-of-pocket costs.

Consider a 65-year-old retiree on Medicare who needs chemotherapy. While Medicare Part A and B cover much of the treatment, they don’t account for daily transportation to the hospital or meals during extended stays. A supplemental cancer insurance policy could provide a lump-sum cash benefit—say, $5,000—to offset these incidental costs. This example illustrates how supplemental insurance complements primary coverage by addressing gaps in both medical and non-medical expenses.

When evaluating supplemental insurance, focus on the specific gaps in your primary plan. For instance, critical illness insurance pays a lump sum upon diagnosis of conditions like heart attack or stroke, while accident insurance covers costs related to injuries. Compare policies carefully: some offer fixed cash benefits, while others reimburse based on actual expenses. For example, a $10,000 critical illness payout could be used for lost wages, experimental treatments, or even mortgage payments, providing flexibility beyond traditional health coverage.

A common misconception is that Medigap and supplemental insurance are interchangeable terms. While Medigap is a type of supplemental insurance designed specifically to fill gaps in Medicare, supplemental insurance as a category is broader. For instance, a 40-year-old with employer-sponsored health insurance might purchase supplemental dental or vision coverage, which are not included in Medigap policies. Understanding this distinction ensures you select the right type of coverage for your needs.

To maximize the benefits of supplemental insurance, assess your health risks and financial vulnerabilities. For example, a family with a history of cancer might prioritize critical illness coverage, while frequent travelers could benefit from policies covering emergency medical evacuations. Pairing supplemental insurance with a high-deductible health plan can also reduce overall costs. Always review policy exclusions and waiting periods—some plans require 30 days before coverage begins—to avoid surprises when filing claims.

Understanding the Texas Department of Insurance: Roles, Responsibilities, and Services

You may want to see also

Explore related products

![]()

Key Differences: Medigap is Medicare-specific, while supplemental insurance can apply to any health plan

Medigap and supplemental insurance often get lumped together, but they serve distinct purposes in the healthcare landscape. The key differentiator lies in their scope: Medigap is exclusively designed to fill the gaps in Medicare coverage, while supplemental insurance can be paired with any health plan, whether it’s employer-sponsored, individual, or government-funded. This specificity makes Medigap a niche product, tailored to Medicare beneficiaries aged 65 and older or those under 65 with certain disabilities. Supplemental insurance, on the other hand, is a broader tool, offering additional benefits like vision, dental, or critical illness coverage, regardless of the primary plan’s source.

Consider a 67-year-old retiree on Medicare Part A and B. They might choose Medigap Plan G to cover copayments, coinsurance, and the Part A deductible, which Medicare alone doesn’t fully address. In contrast, a 45-year-old with an employer-sponsored PPO plan might opt for a supplemental insurance policy to cover high-deductible expenses or provide cash benefits for a serious illness. The former is Medicare-specific, while the latter is adaptable to any health plan structure. This distinction is crucial for consumers to understand, as it directly impacts the type of coverage they can—and should—purchase.

From a practical standpoint, Medigap policies are standardized by the federal government, meaning Plan G in Texas offers the same benefits as Plan G in New York. Supplemental insurance, however, varies widely by provider and policy. For instance, one supplemental plan might offer a $5,000 payout upon cancer diagnosis, while another might cover 80% of out-of-network dental costs. This variability requires careful comparison, whereas Medigap’s uniformity simplifies the decision-making process for Medicare beneficiaries.

A persuasive argument for choosing Medigap over general supplemental insurance for Medicare users is its predictability. Since Medigap is designed exclusively for Medicare, it seamlessly integrates with Parts A and B, ensuring there are no overlaps or gaps in coverage. Supplemental insurance, while flexible, may not align as neatly with Medicare’s structure, potentially leaving beneficiaries with unused benefits or uncovered expenses. For example, a supplemental policy might cover alternative therapies not included in Medicare, but it won’t help with Medicare’s Part B excess charges—a gap Medigap is specifically built to address.

In conclusion, while both Medigap and supplemental insurance aim to enhance health coverage, their applications differ significantly. Medigap’s Medicare-specific design offers clarity and precision for beneficiaries navigating the complexities of federal healthcare programs. Supplemental insurance, with its broader applicability, provides flexibility but demands more scrutiny to ensure it complements the primary plan effectively. Understanding this distinction empowers consumers to make informed choices tailored to their unique healthcare needs.

Tobacco Users: Life Insurance Considerations and Costs

You may want to see also

Explore related products

![]()

Coverage Comparison: Medigap focuses on Medicare gaps; supplemental insurance varies by policy and provider

Medigap and supplemental insurance are often used interchangeably, but their coverage scopes differ significantly. Medigap, also known as Medicare Supplement Insurance, is specifically designed to fill the gaps in Original Medicare (Parts A and B). These gaps include copayments, coinsurance, and deductibles, which can add up quickly for beneficiaries. For instance, Medicare Part A has a $1,600 deductible per benefit period for hospital stays, and Part B covers only 80% of outpatient services, leaving beneficiaries responsible for the remaining 20%. Medigap policies, standardized by the federal government, offer up to 10 plans (A through N) with varying levels of coverage, ensuring predictability in out-of-pocket costs.

Supplemental insurance, on the other hand, is a broader term that encompasses a wide range of policies not limited to Medicare. These plans can cover anything from dental and vision care to critical illness and accident benefits. Unlike Medigap, supplemental insurance policies are not standardized and vary widely by provider and policy type. For example, a critical illness policy might pay a lump sum upon diagnosis of a covered condition, while a hospital indemnity plan provides a fixed daily amount for each day spent in the hospital. This variability means consumers must carefully review policy details to understand what is and isn’t covered.

A key distinction lies in the target audience and purpose. Medigap is exclusively for individuals aged 65 and older or those under 65 with certain disabilities who are enrolled in Medicare. Its primary function is to reduce financial uncertainty by covering costs Medicare doesn’t. Supplemental insurance, however, caters to a broader demographic, including those with employer-sponsored health plans, Medicaid, or even no primary insurance. For example, a 40-year-old with employer-sponsored health insurance might purchase a supplemental accident policy to cover high deductibles in case of injury.

When comparing the two, Medigap offers uniformity and predictability, making it easier for Medicare beneficiaries to budget for healthcare expenses. Supplemental insurance, while more flexible, requires careful scrutiny to avoid gaps or overlaps in coverage. For instance, someone with both Medigap and a supplemental hospital indemnity plan might receive duplicate benefits for hospital stays, leading to unnecessary costs. Practical tips include reviewing the Summary of Benefits for both types of policies and consulting a licensed insurance agent to ensure coverage aligns with individual health needs and financial goals.

In conclusion, while both Medigap and supplemental insurance aim to enhance existing coverage, their structures and applications differ markedly. Medigap’s focus on Medicare gaps provides a clear, standardized solution for seniors, whereas supplemental insurance offers diverse options tailored to a wider audience. Understanding these differences is crucial for making informed decisions and maximizing the value of insurance investments.

Complete Guide to Insuring Your Trailer: Tips and Coverage Options

You may want to see also

Explore related products

![]()

Eligibility Criteria: Medigap requires Medicare enrollment; supplemental insurance has no such requirement

Medigap and supplemental insurance may sound interchangeable, but their eligibility criteria reveal a fundamental difference. Medigap, short for Medicare Supplement Insurance, is exclusively available to individuals already enrolled in Medicare Parts A and B. This means you must be 65 or older, or under 65 with certain disabilities, to qualify for Medigap. Supplemental insurance, on the other hand, operates independently of Medicare. It can be purchased by anyone, regardless of age or Medicare status, making it a more flexible option for those seeking additional coverage outside the Medicare framework.

Consider a 55-year-old individual with a high-deductible health plan through their employer. They’re ineligible for Medigap due to their age and lack of Medicare enrollment. However, they can purchase a supplemental insurance policy to offset out-of-pocket costs like copays, deductibles, or even services not covered by their primary plan, such as dental or vision care. This example highlights how supplemental insurance fills gaps in coverage for those who don’t yet qualify for Medicare or choose not to enroll in it.

The Medicare enrollment requirement for Medigap also limits its use as a standalone solution. For instance, if you’re 67 and enrolled in Medicare, Medigap can help cover costs like Part A deductibles (up to $1,600 per benefit period in 2023) or Part B excess charges. However, if you’re under 65 and rely on an ACA-compliant plan, supplemental insurance might be your only option to enhance coverage, as Medigap isn’t available to you. This distinction underscores the importance of understanding your eligibility before choosing between the two.

A practical tip for those approaching Medicare eligibility: enroll in Medicare Part B during your Initial Enrollment Period (the seven-month window around your 65th birthday) to avoid late penalties and ensure Medigap availability. Once enrolled, you have a six-month Medigap Open Enrollment Period, during which insurers cannot deny you coverage or charge higher premiums based on pre-existing conditions. Missing this window could limit your Medigap options, making supplemental insurance a more viable alternative for gap coverage.

In summary, while both Medigap and supplemental insurance aim to enhance existing coverage, their eligibility criteria set them apart. Medigap’s Medicare dependency restricts it to a specific demographic, whereas supplemental insurance offers broader accessibility. Understanding this distinction ensures you choose the right option based on your age, health plan, and coverage needs.

Equitable National Life: A Good Medicare Supplement Insurance Option?

You may want to see also

Frequently asked questions

Yes, Medigap and supplemental insurance refer to the same type of policy. Medigap is a specific term for supplemental insurance plans designed to cover gaps in Original Medicare (Parts A and B).

Medigap/supplemental insurance covers costs that Original Medicare doesn’t fully pay, such as copayments, coinsurance, deductibles, and in some cases, foreign travel emergency care.

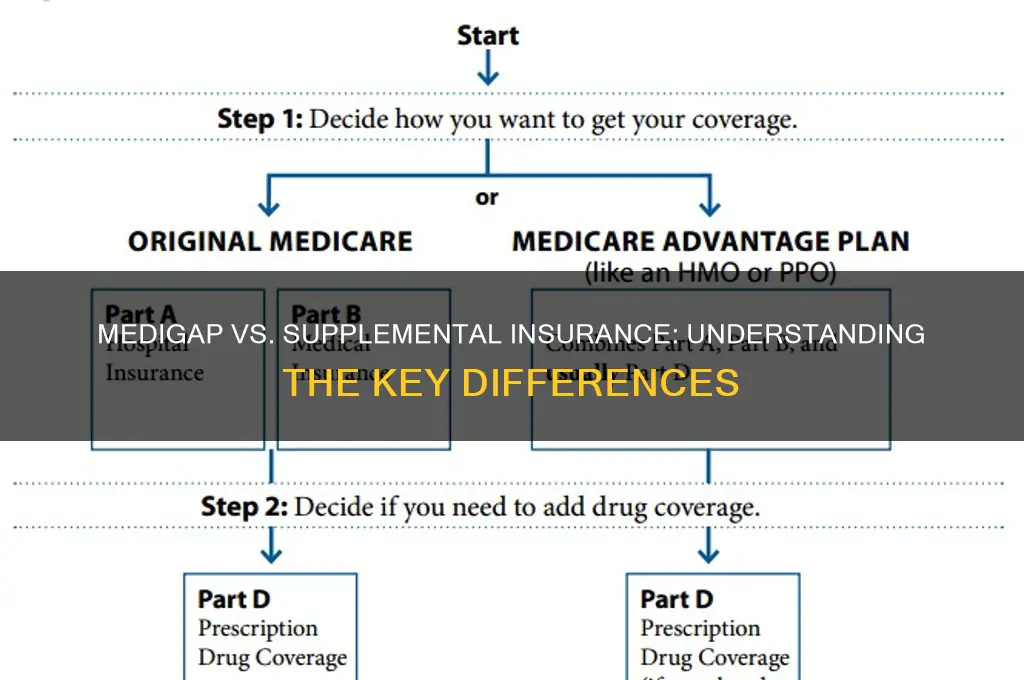

No, you cannot have both Medigap and Medicare Advantage at the same time. Medigap is only compatible with Original Medicare, while Medicare Advantage is an alternative to Original Medicare.

No, Medigap plans are standardized into different lettered plans (e.g., Plan G, Plan N), each offering different levels of coverage. However, the benefits for each plan type are the same across insurers, though costs may vary.