Medigap insurance, also known as Medicare Supplement Insurance, is a private health insurance policy designed to cover some of the out-of-pocket costs that Original Medicare (Parts A and B) doesn’t pay, such as copayments, coinsurance, and deductibles. While Medicare provides essential coverage, it often leaves beneficiaries with significant expenses, particularly for those with chronic conditions or frequent medical needs. Medigap insurance can offer financial predictability and peace of mind by filling these gaps, but it comes with additional premiums and may not be necessary for everyone. Whether Medigap is necessary depends on individual health needs, budget, and preferences, making it important to weigh the benefits against the costs before deciding.

| Characteristics | Values |

|---|---|

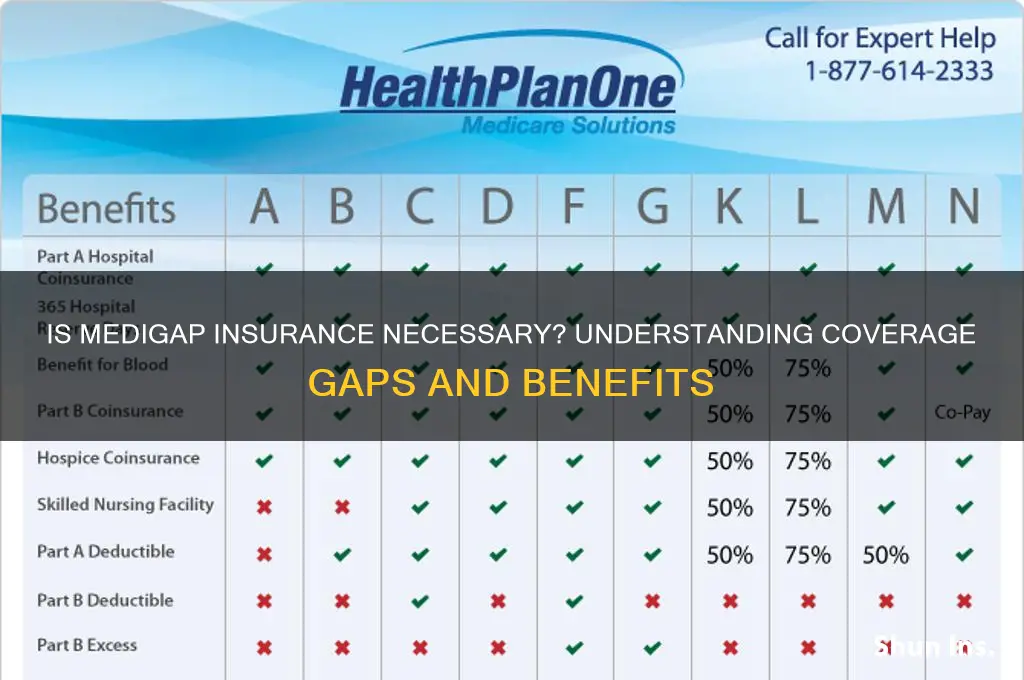

| Coverage Gaps | Medigap (Medicare Supplement Insurance) helps cover costs not paid by Original Medicare, such as copayments, coinsurance, and deductibles. |

| Financial Protection | Provides financial predictability by reducing out-of-pocket expenses, especially for frequent healthcare users. |

| Provider Flexibility | Allows access to any doctor or hospital that accepts Medicare, unlike Medicare Advantage plans with network restrictions. |

| Travel Coverage | Offers coverage for emergency care while traveling outside the U.S., depending on the plan. |

| No Referrals Needed | Does not require referrals to see specialists, unlike some Medicare Advantage plans. |

| Standardized Plans | Plans (A-N) are standardized, making it easier to compare across insurers based on price and reputation. |

| Premium Costs | Requires paying a monthly premium in addition to Medicare Part B premiums, which may be a financial burden for some. |

| No Prescription Coverage | Does not cover prescription drugs; a separate Part D plan is needed for medication coverage. |

| Enrollment Timing | Best to enroll during the 6-month Medigap Open Enrollment Period starting when you turn 65 to avoid underwriting and higher premiums. |

| Guaranteed Issue Rights | Certain situations (e.g., losing employer coverage) guarantee the right to buy a Medigap policy without medical underwriting. |

| Alternative to Medicare Advantage | A viable option for those who prefer Original Medicare over Medicare Advantage plans. |

| Long-Term Stability | Provides consistent coverage, unlike Medicare Advantage plans that may change benefits annually. |

| Cost-Benefit Analysis | Necessary if you anticipate high healthcare usage or want to minimize unexpected expenses. May be less necessary for those with low healthcare needs or sufficient savings. |

Explore related products

What You'll Learn

![]()

Cost vs. Coverage Benefits

Medigap insurance, also known as Medicare Supplement Insurance, is designed to cover the gaps in Original Medicare, such as copayments, coinsurance, and deductibles. When evaluating whether Medigap is necessary, the cost versus coverage benefits becomes a pivotal consideration. Premiums for Medigap plans can range from $100 to $300 per month, depending on factors like age, location, and the specific plan chosen. While this additional cost may seem burdensome, it’s essential to weigh it against the potential out-of-pocket expenses without such coverage. For instance, Medicare Part A has a $1,600 deductible per benefit period for hospital stays, and Part B covers only 80% of approved medical costs, leaving beneficiaries responsible for the remaining 20%. Medigap plans can eliminate or significantly reduce these costs, providing financial predictability.

Consider a 65-year-old retiree in Texas who opts for Medigap Plan G, one of the most comprehensive options. With a monthly premium of approximately $150, this plan covers the Part A deductible, Part B excess charges, and foreign travel emergency care. Without this plan, a single hospital stay could result in thousands of dollars in out-of-pocket costs. For someone on a fixed income, the predictable monthly premium offers peace of mind compared to the uncertainty of unexpected medical bills. However, for healthier individuals with minimal healthcare needs, the cost of Medigap might outweigh the immediate benefits, making it a less attractive option.

A comparative analysis reveals that Medigap plans differ significantly in coverage and cost. For example, Plan G and Plan N are popular choices, but Plan N has lower premiums (around $100–$120 monthly) because it requires beneficiaries to pay small copayments for doctor visits and emergency room trips. In contrast, Plan G covers these costs entirely. The decision here hinges on personal health risk tolerance and budget. Someone with chronic conditions might prefer the higher premium of Plan G for comprehensive coverage, while a healthier individual might opt for Plan N to save on monthly costs.

From a practical standpoint, it’s crucial to assess your healthcare utilization patterns before committing to Medigap. If you rarely visit the doctor and have no pre-existing conditions, the added expense might not be justified. However, if you anticipate frequent medical services or have a history of hospitalizations, the coverage benefits could far outweigh the cost. Additionally, Medigap policies are standardized, meaning Plan G in one state offers the same benefits as Plan G in another, though premiums vary. Shopping around for the best rates and understanding enrollment periods (such as the six-month open enrollment starting when you turn 65) can maximize value.

Ultimately, the decision to purchase Medigap insurance rests on balancing financial stability against potential healthcare expenses. While the cost of premiums may seem high, the coverage benefits can prevent catastrophic financial strain in the event of serious illness or injury. For those prioritizing predictability and comprehensive coverage, Medigap is a worthwhile investment. Conversely, individuals comfortable with higher risk and lower monthly costs might explore alternatives like Medicare Advantage plans. The key is to evaluate your unique health needs, budget, and risk tolerance to make an informed choice.

Calculate Building Insurance: A Step-by-Step Guide to Accurate Coverage

You may want to see also

Explore related products

![]()

Medicare Gaps and Limitations

Medicare, while a vital safety net for millions of Americans, is not all-encompassing. One of its most significant limitations lies in the coverage gaps that can leave beneficiaries with unexpected out-of-pocket expenses. For instance, Original Medicare (Parts A and B) does not cover long-term care, most dental care, vision care, hearing aids, or prescription drugs beyond a limited hospital setting. These omissions can be particularly burdensome for seniors, who often require ongoing medical attention and specialized care. Consider a scenario where a 70-year-old retiree needs a hearing aid, which can cost upwards of $2,500 per device. Without supplemental coverage, this expense falls entirely on the individual.

Another critical gap in Medicare is the lack of an out-of-pocket maximum for Parts A and B. While Part A (hospital insurance) covers inpatient care after a deductible ($1,632 per benefit period in 2023), it does not cap additional costs for extended stays. Similarly, Part B (medical insurance) requires beneficiaries to pay 20% of the Medicare-approved amount for most doctor services, outpatient therapy, and durable medical equipment. For someone undergoing chemotherapy, which can cost thousands of dollars per session, this coinsurance can quickly escalate. For example, a patient receiving a $10,000 treatment would be responsible for $2,000 out-of-pocket, plus any unpaid deductible.

Medicare’s limitations also extend to international travel. Original Medicare provides little to no coverage outside the United States, except in rare circumstances, such as a medical emergency in Canada when the closest hospital is across the border. For retirees planning to travel abroad, this gap can be a significant concern. A sudden illness or injury while vacationing in Europe could result in exorbitant medical bills, as Medicare would not cover the expenses. Travelers must either purchase separate travel insurance or consider supplemental coverage that includes foreign emergency care.

To address these gaps, beneficiaries often turn to Medigap policies, which are designed to cover costs like copayments, coinsurance, and deductibles. However, Medigap plans themselves have limitations. For example, they do not cover prescription drugs, necessitating a separate Part D plan. Additionally, Medigap policies are not standardized across states, and premiums can vary widely based on factors like age, location, and insurer. For instance, a 65-year-old in Texas might pay $120 monthly for Plan G, while a peer in New York could pay $180 for the same coverage. Understanding these nuances is crucial for making informed decisions about supplemental insurance.

In conclusion, Medicare’s gaps and limitations highlight the need for careful planning and supplemental coverage. Whether it’s the lack of long-term care coverage, unlimited out-of-pocket costs, or insufficient international protection, these shortcomings can lead to financial strain. By evaluating individual health needs, travel plans, and budget constraints, beneficiaries can determine if Medigap insurance is necessary to bridge these gaps and ensure comprehensive protection.

Do Part-Time Jobs Offer Health Insurance Benefits? What to Know

You may want to see also

Explore related products

![]()

Age and Health Factors

As individuals age, their healthcare needs evolve, often requiring more frequent medical attention and specialized treatments. This shift in health dynamics raises the question: Is Medigap insurance a prudent investment for seniors? The answer lies in understanding the intricate relationship between age, health, and the limitations of original Medicare.

The Aging Body's Unique Demands

For those over 65, the body's natural aging process can lead to a higher prevalence of chronic conditions. According to the CDC, 85% of older adults have at least one chronic health condition, with 60% having two or more. These may include arthritis, diabetes, or heart disease, which often necessitate regular doctor visits, prescription medications, and occasional hospital stays. Original Medicare, while comprehensive, may not cover all these expenses, leaving beneficiaries with significant out-of-pocket costs. This is where Medigap steps in, offering supplementary coverage for copayments, coinsurance, and deductibles.

A Preventive Approach to Healthcare

A strategic approach to healthcare in later years involves anticipating needs and planning accordingly. Medigap policies can be particularly advantageous for individuals with a family history of age-related illnesses or those already managing chronic conditions. For instance, someone with a family history of Alzheimer's disease might consider the potential long-term care needs and the associated costs, which could be partially mitigated by certain Medigap plans. By enrolling in a suitable Medigap policy during the initial enrollment period, individuals can secure coverage without undergoing medical underwriting, ensuring acceptance regardless of pre-existing conditions.

Weighing the Costs and Benefits

The decision to purchase Medigap insurance requires a careful analysis of personal health and financial circumstances. Premiums for these policies vary widely, depending on the plan type, location, and age at the time of purchase. On average, premiums can range from $100 to $300 per month, with Plan G (a popular comprehensive option) costing around $150 monthly for a 65-year-old. While this may seem like an additional burden, it's essential to compare these costs against potential out-of-pocket expenses without Medigap. For instance, a hospital stay without supplementary insurance could result in thousands of dollars in coinsurance and deductible payments.

Tailoring Coverage to Individual Needs

The beauty of Medigap lies in its ability to cater to diverse health profiles. With multiple plan options, individuals can choose coverage that aligns with their specific needs. For instance, Plan N offers lower premiums by requiring small copayments for doctor visits and emergency room trips, making it suitable for relatively healthy individuals who want basic coverage. In contrast, Plan F, the most comprehensive option, covers all Medicare-approved expenses, providing peace of mind for those with complex health needs. Understanding these nuances is crucial for making an informed decision, ensuring that the chosen Medigap policy complements one's health and financial situation.

In the context of aging and health, Medigap insurance emerges as a strategic tool for managing healthcare expenses. By addressing the gaps in original Medicare, it provides a safety net for seniors, allowing them to focus on their well-being without the constant worry of unforeseen medical costs. The key lies in recognizing the unique health challenges that come with age and proactively selecting a Medigap plan that offers the necessary support.

Does Post Office Cash Insurance Cover Your Needs? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Alternative Insurance Options

Medicare Advantage plans, also known as Part C, offer an alternative to traditional Medicare and Medigap insurance. These plans are provided by private insurance companies approved by Medicare and often include additional benefits like vision, dental, and prescription drug coverage. For instance, a 65-year-old retiree might find a Medicare Advantage plan that covers routine eye exams and eyeglasses, which are not typically covered by Original Medicare. This option can be particularly appealing for those seeking comprehensive coverage without the need for separate Medigap policies. However, it’s crucial to review the plan’s network restrictions and out-of-pocket costs, as these can vary significantly.

Employer-sponsored health insurance can serve as a viable alternative to Medigap for individuals who are still working or have access to a spouse’s plan. For example, a 60-year-old employee might retain their employer’s health insurance after turning 65, delaying the need for Medigap. This approach can be cost-effective, as employer plans often cover services that Medicare doesn’t, such as certain preventive care or specialized treatments. However, it’s essential to coordinate benefits between the employer plan and Medicare to avoid gaps in coverage. Consulting with a benefits administrator or insurance advisor can help clarify which plan should be primary.

Health Savings Accounts (HSAs) paired with high-deductible health plans (HDHPs) offer another alternative for those who prefer flexibility and control over their healthcare spending. Individuals under 65 can contribute to an HSA, which can be used to pay for medical expenses tax-free. Once enrolled in Medicare, contributions to an HSA must stop, but the funds can still be used to cover out-of-pocket costs, effectively reducing the need for Medigap. For example, a 55-year-old with an HSA might use accumulated savings to cover deductibles or copayments after transitioning to Medicare. This strategy requires careful planning, as HDHPs typically have higher out-of-pocket limits.

For low-income individuals, Medicaid can supplement Medicare and eliminate the need for Medigap. Known as dual eligibility, this option provides additional coverage for services like long-term care, which Medicare doesn’t fully cover. For instance, a 70-year-old with limited income might qualify for Medicaid to help pay Medicare premiums, deductibles, and other costs. Eligibility criteria vary by state, so checking with the local Medicaid office is essential. This dual coverage ensures comprehensive protection without the added expense of Medigap.

Retiree health plans, offered by some former employers or unions, can also serve as an alternative to Medigap. These plans often cover costs that Medicare doesn’t, such as certain prescription drugs or specialized treatments. For example, a retired teacher might have access to a retiree health plan that covers physical therapy sessions not fully paid by Medicare. However, these plans are becoming less common, and their benefits can vary widely. It’s important to compare the plan’s coverage to Medigap options to ensure it meets individual healthcare needs.

Life Insurance Proceeds: When to Report and Why

You may want to see also

Explore related products

![]()

Long-Term Financial Planning

Medigap insurance, also known as Medicare Supplement Insurance, is a critical component of long-term financial planning for individuals aged 65 and older. While Original Medicare (Parts A and B) covers a significant portion of healthcare costs, it leaves beneficiaries responsible for deductibles, copayments, and coinsurance. These out-of-pocket expenses can accumulate rapidly, particularly for those with chronic conditions or frequent medical needs. Medigap policies are designed to fill these gaps, offering predictable costs and peace of mind. However, determining whether Medigap is necessary requires a careful analysis of your health status, financial situation, and long-term goals.

Consider this scenario: A 67-year-old retiree with a fixed income faces a sudden hospitalization, resulting in a $1,600 Part A deductible and 20% coinsurance for outpatient services. Without Medigap, these costs could deplete savings or force reliance on credit. Medigap Plan G, one of the most popular options, covers the Part A deductible and coinsurance, ensuring the retiree pays only the monthly premium. This example highlights how Medigap can stabilize long-term finances by capping healthcare expenses. To maximize its value, enroll during the six-month Medigap Open Enrollment Period, which begins when you turn 65 and enroll in Medicare Part B. During this time, insurers cannot deny coverage or charge higher premiums based on pre-existing conditions.

A comparative analysis of Medigap versus Medicare Advantage (Part C) reveals distinct advantages for long-term planners. Medicare Advantage plans often have lower monthly premiums and include prescription drug coverage (Part D), but they typically feature provider networks and annual out-of-pocket maximums ranging from $4,000 to $7,550 in 2023. Medigap, on the other hand, allows you to see any Medicare-approved provider and eliminates most out-of-pocket costs. For those prioritizing flexibility and predictable expenses, Medigap is often the better choice. However, if you’re in good health and prefer lower upfront costs, Medicare Advantage might suffice—though it carries greater financial risk in the event of serious illness.

Instructively, integrating Medigap into your long-term financial plan involves three key steps. First, assess your healthcare utilization over the past five years. If you’ve had frequent hospitalizations or specialist visits, Medigap is likely a wise investment. Second, compare premiums across insurers, as prices for the same plan (e.g., Plan G) can vary widely. Use tools like the Medicare Plan Finder to identify affordable options in your area. Third, align Medigap with other retirement accounts, such as Health Savings Accounts (HSAs). Note that if you have an HSA-qualified high-deductible health plan, enrolling in Medigap will disqualify you from contributing to the HSA, though you can still use existing funds tax-free for medical expenses.

Persuasively, the necessity of Medigap hinges on its role as a safeguard against catastrophic healthcare costs. A 2022 study by the Kaiser Family Foundation found that 50% of Medicare beneficiaries spent over $5,000 annually on healthcare, with 10% exceeding $10,000. Without Medigap, these expenses could derail retirement plans, forcing individuals to delay travel, downsize homes, or reduce support for dependents. By contrast, Medigap ensures that healthcare costs remain manageable, preserving financial stability and quality of life. For those with limited savings or a family history of chronic illness, the long-term benefits of Medigap far outweigh the monthly premium.

Descriptively, envision a future where healthcare expenses are predictable, and retirement funds are allocated to experiences rather than medical bills. Medigap transforms this vision into reality by eliminating the uncertainty of out-of-pocket costs. For instance, a couple in their late 60s with Medigap Plan G can budget confidently for a European vacation, knowing their healthcare is covered. Conversely, without Medigap, a single unexpected procedure could force them to cancel plans or dip into emergency funds. In long-term financial planning, Medigap is not just an insurance policy—it’s a tool for securing the retirement lifestyle you’ve worked decades to achieve.

Hail Damage Impact: Will Your Insurance Premiums Increase?

You may want to see also

Frequently asked questions

Medigap insurance is not necessary, but it can help cover costs that Original Medicare doesn’t, such as copayments, coinsurance, and deductibles. It’s optional and depends on your healthcare needs and budget.

If you’re in good health and don’t anticipate frequent medical expenses, you might not need Medigap immediately. However, it’s important to consider potential future costs, as Medigap is easier to obtain during your initial enrollment period.

No, Medigap insurance cannot be used with Medicare Advantage plans. If you have a Medicare Advantage plan, Medigap is not necessary or allowed, as these plans already provide additional coverage beyond Original Medicare.