The Affordable Care Act (ACA), commonly known as Obamacare, has been a subject of intense debate since its inception. One of the key arguments against the ACA is the claim that it has led to increased health insurance premiums. Proponents of the ACA argue that it has expanded coverage to millions of Americans and implemented important consumer protections. However, critics contend that the law's mandates and regulations have driven up costs for insurers, which are then passed on to policyholders in the form of higher premiums. The impact of the ACA on health insurance costs is a complex issue that depends on various factors, including the specific provisions of the law, the dynamics of the insurance market, and the overall healthcare system.

Explore related products

What You'll Learn

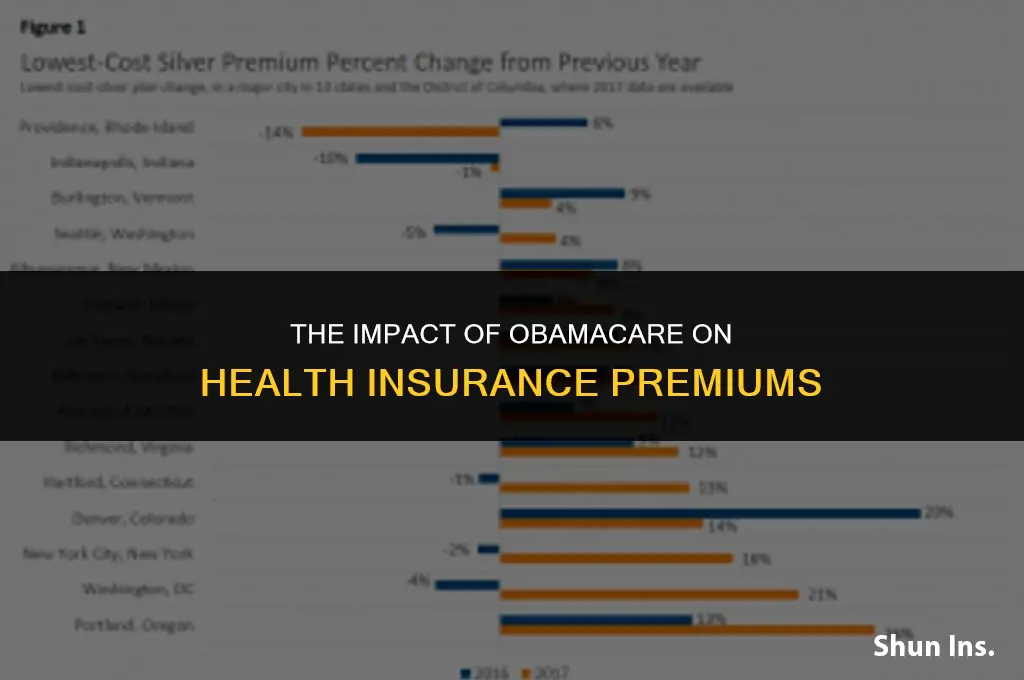

- Premium increases: Many Americans face higher monthly premiums under the Affordable Care Act

- Reduced competition: Some areas have fewer insurance providers, leading to increased costs

- Mandate penalties: Individuals without coverage may face fines, indirectly raising insurance expenses

- Subsidy reductions: Decreases in federal subsidies have made insurance less affordable for some

- Increased deductibles: Higher out-of-pocket costs for consumers before coverage kicks in

![]()

Premium increases: Many Americans face higher monthly premiums under the Affordable Care Act

Under the Affordable Care Act (ACA), many Americans have experienced an increase in their monthly health insurance premiums. This phenomenon can be attributed to several factors, including changes in the insurance market dynamics, the introduction of new regulations, and the overall rising cost of healthcare services. For instance, the ACA's requirement for insurers to cover individuals with pre-existing conditions has led to a higher risk pool, which in turn has resulted in increased premiums for all policyholders.

Moreover, the ACA's implementation has coincided with a shift towards higher-deductible health plans, which, while potentially reducing monthly premiums, can lead to increased out-of-pocket expenses for consumers. This trade-off has been a subject of debate, with some arguing that the ACA has made health insurance more affordable for those who need it most, while others contend that it has simply shifted the cost burden from premiums to deductibles and copays.

Another contributing factor to premium increases has been the ACA's establishment of health insurance exchanges, which were intended to foster competition among insurers and drive down costs. However, in some cases, these exchanges have resulted in a lack of competition, with only a few insurers participating in certain markets. This limited competition can lead to higher premiums, as insurers may not feel pressured to keep their prices low.

Furthermore, the ACA's subsidies for low-income individuals have inadvertently contributed to premium increases. While these subsidies help make health insurance more affordable for those who qualify, they also create a perverse incentive for insurers to raise their premiums, as they know that the government will cover a portion of the cost for eligible policyholders.

In conclusion, the premium increases experienced by many Americans under the ACA are a complex issue with multiple contributing factors. While the law has undoubtedly made health insurance more accessible for some, it has also led to higher costs for others. As policymakers continue to debate the merits and drawbacks of the ACA, it is essential to consider the nuanced impact of premium increases on individuals and families across the country.

Does Health Insurance Cover Marital Counseling? What You Need to Know

You may want to see also

Explore related products

![]()

Reduced competition: Some areas have fewer insurance providers, leading to increased costs

In the wake of the Affordable Care Act (ACA), commonly known as Obamacare, one of the unintended consequences has been the reduction of competition among health insurance providers in certain areas. This phenomenon has led to increased costs for consumers, as fewer options often result in higher premiums. The ACA aimed to increase access to healthcare and promote competition, but in some regions, the opposite effect has occurred.

One of the primary reasons for reduced competition is the consolidation of insurance companies. Since the ACA's implementation, several major insurers have merged or acquired smaller competitors, leading to a more concentrated market. This consolidation can limit consumer choice, as fewer companies are available to provide coverage. Additionally, the ACA's regulations and requirements may have created barriers to entry for new insurance providers, further stifling competition.

Another factor contributing to reduced competition is the withdrawal of some insurers from certain markets. Due to financial losses or regulatory challenges, several companies have decided to exit specific states or regions, leaving fewer options for consumers. This withdrawal can be particularly problematic in rural or less populated areas, where the market may already be limited.

The impact of reduced competition on health insurance costs cannot be overstated. When fewer companies are vying for customers, they have less incentive to keep premiums low. As a result, consumers may face higher costs for coverage, which can be particularly burdensome for those who do not qualify for subsidies or financial assistance. Furthermore, reduced competition can lead to a lack of innovation and improvement in the quality of care, as insurers may not feel pressured to offer better services or more affordable plans.

To address the issue of reduced competition and rising costs, policymakers and regulators may need to consider new strategies. These could include measures to encourage more companies to enter the market, such as reducing regulatory barriers or offering incentives for new providers. Additionally, efforts to promote transparency and accountability in the insurance industry could help to ensure that consumers are getting the best possible value for their healthcare dollars.

In conclusion, while the ACA has made significant strides in increasing access to healthcare, the unintended consequence of reduced competition in some areas has led to increased costs for consumers. Addressing this issue will require a thoughtful and multifaceted approach, but it is crucial for ensuring that the benefits of the ACA are realized by all Americans.

Understanding Washington State's Health Insurance Requirements: A 2023 Update

You may want to see also

Explore related products

![Life and Health Insurance License Study Cards: Life Health Insurance Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Mandate penalties: Individuals without coverage may face fines, indirectly raising insurance expenses

The Affordable Care Act (ACA), commonly known as Obamacare, introduced a mandate that requires most individuals to have health insurance coverage or pay a penalty. This mandate was designed to increase the number of insured individuals, thereby spreading the cost of healthcare across a larger population and potentially reducing overall healthcare expenses. However, the implementation of this mandate has had unintended consequences, including indirectly raising insurance expenses for some individuals.

One of the primary ways the mandate has led to increased insurance costs is through the individual mandate penalty. Those who do not have qualifying health coverage may be subject to a fine, which can be substantial depending on their income and the number of people in their household. In 2019, the penalty for an individual was $695 or 2.5% of their gross income, whichever is greater. For families, the penalty is $2,085 or 2.5% of their gross income. These penalties can add up over time, effectively increasing the cost of health insurance for those who choose not to purchase it.

Furthermore, the mandate has led to an increase in the number of individuals purchasing health insurance, which can drive up demand and, consequently, prices. Insurers may also factor in the cost of covering individuals who are only purchasing insurance to avoid the penalty, potentially leading to higher premiums for all policyholders. Additionally, some insurers may choose to limit their offerings in certain markets or increase their prices in response to the mandate, further contributing to rising insurance costs.

Critics of the mandate argue that it disproportionately affects younger, healthier individuals who may not see the value in purchasing health insurance. These individuals may be more likely to opt for the penalty, which can lead to a skewed risk pool and higher costs for insurers. Supporters of the mandate, on the other hand, argue that it is necessary to ensure that everyone has access to affordable healthcare and that the benefits of increased coverage outweigh the potential costs.

In conclusion, while the ACA's individual mandate was intended to increase health insurance coverage and reduce overall healthcare costs, it has also had the unintended consequence of indirectly raising insurance expenses for some individuals. The mandate penalty, increased demand for insurance, and changes in insurer behavior have all contributed to this phenomenon. As policymakers continue to debate the merits of the ACA, it is important to consider the complex interplay between these factors and their impact on the cost of health insurance.

Do Insurance Companies Keep Records of Past Incidents? Find Out Here

You may want to see also

Explore related products

![]()

Subsidy reductions: Decreases in federal subsidies have made insurance less affordable for some

The reduction in federal subsidies has had a profound impact on the affordability of health insurance for many Americans. These subsidies, which were a crucial component of the Affordable Care Act (ACA), were designed to help lower-income individuals and families purchase health insurance by reducing their monthly premiums. However, with the decrease in these subsidies, many have found it increasingly difficult to afford health coverage.

One of the primary reasons for the subsidy reductions was the Republican-led Congress's efforts to dismantle the ACA. In 2017, the Tax Cuts and Jobs Act eliminated the individual mandate, which required most Americans to have health insurance or pay a penalty. This move led to a significant decrease in the number of people enrolling in ACA plans, as the penalty for not having insurance was no longer a deterrent. As a result, the federal government reduced the subsidies provided to insurers, which in turn led to higher premiums for consumers.

The impact of these subsidy reductions has been particularly felt by those in the middle class. Prior to the reductions, many middle-class Americans were able to afford health insurance with the help of subsidies. However, with the decrease in subsidies, many have found it challenging to make ends meet. This has led to a significant increase in the number of uninsured Americans, with many opting to go without health coverage due to the high costs.

Furthermore, the subsidy reductions have also had a negative impact on the health insurance market as a whole. With fewer people enrolling in ACA plans, insurers have been forced to increase premiums to cover their costs. This has led to a vicious cycle, where higher premiums lead to fewer enrollees, which in turn leads to even higher premiums. As a result, the health insurance market has become increasingly unstable, with many insurers opting to exit the market altogether.

In conclusion, the reduction in federal subsidies has had a significant impact on the affordability of health insurance for many Americans. This has led to a decrease in the number of insured individuals, an increase in premiums, and a destabilization of the health insurance market. As the debate over the future of the ACA continues, it is clear that the subsidy reductions have had far-reaching consequences for the American healthcare system.

Single Coverage Medical Insurance: What Does It Mean?

You may want to see also

Explore related products

$19.99 $8.99

$0.99 $6.98

![]()

Increased deductibles: Higher out-of-pocket costs for consumers before coverage kicks in

Under the Affordable Care Act (ACA), commonly known as Obamacare, one significant change to health insurance plans has been the increase in deductibles. A deductible is the amount of money a policyholder must pay out of pocket for healthcare services before their insurance coverage begins to pay. This shift towards higher deductibles has been a notable trend in the post-ACA health insurance landscape.

The rise in deductibles can be attributed to several factors. Insurers have argued that higher deductibles help to reduce overall healthcare costs by encouraging consumers to be more mindful of their healthcare spending. The theory is that when individuals are responsible for a larger portion of their healthcare expenses, they are more likely to seek out cost-effective care and avoid unnecessary medical procedures. However, this approach has also led to increased financial burdens for many consumers, particularly those with lower incomes or chronic health conditions.

For many Americans, the higher deductibles have resulted in a significant increase in out-of-pocket healthcare costs. According to a study by the Kaiser Family Foundation, the average deductible for a single person in 2019 was $1,644, up from $991 in 2009. For families, the average deductible rose to $3,282 in 2019, compared to $1,771 a decade earlier. These increases have outpaced wage growth, making healthcare less affordable for a substantial portion of the population.

The impact of higher deductibles has been particularly pronounced for individuals with chronic illnesses or those requiring ongoing medical treatment. For these patients, the increased out-of-pocket costs can be prohibitive, leading to difficulties in accessing necessary care. Additionally, higher deductibles can create a disincentive for preventive care, as individuals may be reluctant to seek out routine check-ups or screenings due to the upfront costs involved.

Critics of the ACA argue that the increase in deductibles is a direct result of the law's provisions, which they claim have driven up healthcare costs overall. Proponents of the ACA, on the other hand, point out that the law has also led to significant improvements in healthcare access and affordability, particularly for low-income individuals and those with pre-existing conditions. They argue that the higher deductibles are a necessary trade-off to achieve these broader goals.

In conclusion, the increase in deductibles under the ACA has been a contentious issue, with both supporters and opponents of the law debating its merits and drawbacks. While higher deductibles may have contributed to a reduction in overall healthcare costs, they have also placed a greater financial burden on many consumers, particularly those who are most in need of healthcare services. As the healthcare landscape continues to evolve, it will be important to consider the impact of deductibles on access to care and overall health outcomes.

Best NE Medicaid Insurance: Top Plans for You

You may want to see also

Frequently asked questions

The impact of Obamacare on health insurance premiums varies widely among individuals. Some people have seen their premiums increase, while others have experienced decreases or remained relatively stable. Factors such as age, health status, location, and the specific insurance plan chosen can significantly influence premium costs.

There are several reasons why some individuals may experience higher insurance rates under Obamacare. These include the law's requirement for insurers to cover people with pre-existing conditions, the inclusion of essential health benefits in all plans, and the overall changes in the health insurance market dynamics. Additionally, some states have seen significant premium increases due to factors such as the lack of competition among insurers or state-specific regulations.

Yes, Obamacare includes several provisions designed to control and reduce health insurance costs over time. These include the establishment of health insurance exchanges to increase competition among insurers, the implementation of cost-sharing reductions for low-income individuals, and the introduction of value-based care models that reward quality and efficiency in healthcare delivery. Additionally, the law aims to reduce overall healthcare spending through measures such as improved preventive care and better coordination of care for patients with chronic conditions.