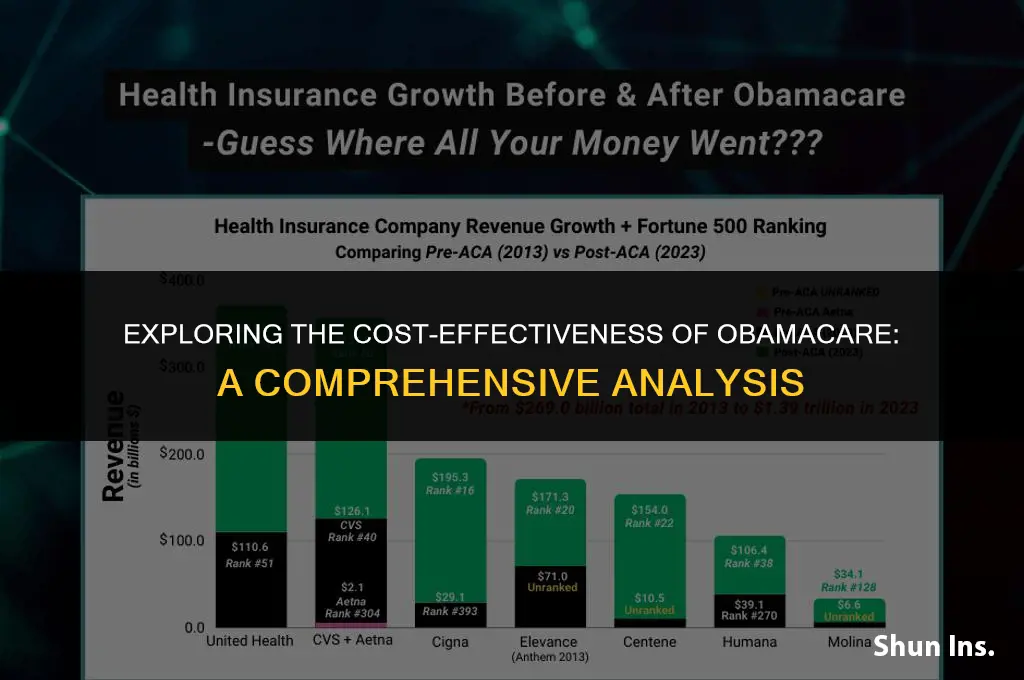

The Affordable Care Act (ACA), commonly known as Obamacare, was a landmark healthcare reform aimed at providing more Americans with access to affordable health insurance. One of the central debates surrounding the ACA has been its impact on healthcare costs. Proponents argue that the ACA introduced several cost-saving measures, such as preventive care coverage and the establishment of health insurance exchanges, which were designed to increase competition and drive down premiums. However, critics contend that the ACA led to higher premiums for some individuals, particularly those who do not qualify for subsidies. The complexity of the healthcare system and the varying experiences of individuals across different states and demographic groups make it challenging to provide a definitive answer to whether Obamacare is less expensive health insurance. A nuanced analysis of the ACA's provisions, its implementation, and its effects on different populations is necessary to understand its overall impact on healthcare affordability.

Explore related products

What You'll Learn

- Premium Costs: Comparing monthly premiums of Obamacare plans to other insurance options

- Out-of-Pocket Expenses: Analyzing deductibles, copays, and coinsurance under Obamacare vs. traditional plans

- Coverage Benefits: Evaluating the comprehensiveness of Obamacare's essential health benefits

- Subsidy Eligibility: Explaining how subsidies can reduce Obamacare costs for low-income individuals

- Long-Term Affordability: Discussing the sustainability of Obamacare's cost structure over time

![]()

Premium Costs: Comparing monthly premiums of Obamacare plans to other insurance options

The Affordable Care Act (ACA), commonly known as Obamacare, has been a subject of debate regarding its cost-effectiveness compared to other health insurance options. A key aspect of this discussion revolves around premium costs. Monthly premiums for ACA plans can vary significantly based on factors such as age, location, and the level of coverage chosen. For instance, a 27-year-old individual in New York City might pay around $300 per month for a mid-level ACA plan, while a similar plan in rural Texas could cost closer to $500.

When comparing these costs to other insurance options, it's essential to consider the differences in coverage and benefits. Employer-sponsored health insurance, for example, often has lower premiums due to the employer's contribution, but may have higher out-of-pocket costs or less comprehensive coverage. Short-term health insurance plans, which are not ACA-compliant, might offer lower premiums but lack essential health benefits and protections, such as coverage for pre-existing conditions.

Another critical factor in the cost comparison is the availability of subsidies. Individuals purchasing ACA plans through the health insurance marketplace may be eligible for premium tax credits, which can significantly reduce the monthly cost. In contrast, other types of health insurance, such as private plans purchased directly from an insurer, do not offer these subsidies.

Furthermore, the ACA's emphasis on preventive care and its prohibition against denying coverage based on pre-existing conditions can lead to long-term cost savings for policyholders. While the initial premiums might be higher, the comprehensive coverage and preventive benefits can result in lower overall healthcare expenses.

In conclusion, while the monthly premiums of Obamacare plans might appear higher than some other options, a detailed comparison reveals that the ACA offers unique benefits and protections that can lead to cost savings in the long run. The availability of subsidies and the comprehensive nature of ACA plans make them a competitive choice for many individuals seeking affordable health insurance.

Depression's Impact: How Mental Health Affects Health Insurance Premiums

You may want to see also

Explore related products

$14.99 $14.99

![]()

Out-of-Pocket Expenses: Analyzing deductibles, copays, and coinsurance under Obamacare vs. traditional plans

Under the Affordable Care Act (ACA), commonly known as Obamacare, out-of-pocket expenses for health insurance have been a subject of significant debate. One of the key aspects of the ACA is its attempt to make healthcare more affordable by reducing the financial burden on individuals. This is achieved through various mechanisms, including subsidies, Medicaid expansion, and the establishment of health insurance exchanges. However, when it comes to out-of-pocket costs such as deductibles, copays, and coinsurance, the picture is more complex.

Deductibles under Obamacare plans can vary widely depending on the specific plan chosen and the individual's income level. In general, ACA plans tend to have lower deductibles compared to traditional health insurance plans, especially for lower-income individuals who qualify for cost-sharing reductions. These reductions can significantly lower the deductible amount, making healthcare more accessible for those who need it most. However, for middle-income individuals, the deductibles under Obamacare can be higher than those under traditional plans, leading to increased out-of-pocket expenses before the insurance coverage kicks in.

Copays and coinsurance also differ between Obamacare and traditional health insurance plans. Under the ACA, copays for primary care visits and generic medications are typically lower, as the law requires insurance companies to cover these services at a lower cost to the consumer. However, for specialty care and brand-name medications, copays can be higher under Obamacare compared to traditional plans. Coinsurance, which is the percentage of the cost of a service that the insured person must pay after meeting the deductible, can also vary. In some cases, Obamacare plans may have lower coinsurance rates, while in others, they may be higher.

When analyzing the out-of-pocket expenses under Obamacare versus traditional plans, it is essential to consider the individual's specific healthcare needs and income level. For those with lower incomes and higher healthcare utilization, Obamacare plans may offer significant savings in terms of out-of-pocket costs. However, for middle-income individuals with lower healthcare needs, traditional plans may be more cost-effective. Ultimately, the affordability of health insurance under the ACA depends on various factors, and a careful comparison of plan options is necessary to determine the most suitable choice.

Removing Yourself from Your Husband's Medical Insurance

You may want to see also

Explore related products

$12.99 $12.99

![]()

Coverage Benefits: Evaluating the comprehensiveness of Obamacare's essential health benefits

The Affordable Care Act (ACA), commonly known as Obamacare, mandates that health insurance plans cover essential health benefits (EHBs). These EHBs are a set of 10 categories of services, including ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder services, prescription drugs, rehabilitative and habilitative services, laboratory services, preventive care, and pediatric services. Evaluating the comprehensiveness of these benefits is crucial in understanding the value and effectiveness of Obamacare.

One unique angle to consider is the impact of EHBs on preventive care. Preventive care services, such as vaccinations, screenings, and check-ups, are fully covered under Obamacare without cost-sharing. This emphasis on prevention can lead to earlier detection of health issues, reducing the need for more expensive treatments down the line. For example, regular mammograms can detect breast cancer in its early stages, when treatment is more effective and less costly than if the cancer is detected later.

Another aspect to analyze is the coverage of mental health and substance use disorder services. Prior to the ACA, many insurance plans did not cover these services or had significant limitations. Obamacare requires that mental health services be covered at parity with physical health services, meaning that the cost-sharing for mental health care cannot be higher than for physical health care. This has increased access to mental health services for millions of Americans, potentially reducing the overall cost of care by addressing mental health issues before they lead to more severe and expensive physical health problems.

The prescription drug coverage under Obamacare is also a critical component. The ACA requires that plans cover a minimum formulary of drugs, which has helped to ensure that patients have access to necessary medications. Additionally, the law has begun to close the Medicare Part D coverage gap, known as the "donut hole," which will further reduce the cost of prescription drugs for seniors.

In conclusion, the essential health benefits mandated by Obamacare provide a comprehensive set of services that can improve health outcomes and potentially reduce overall healthcare costs. By focusing on preventive care, mental health services, and prescription drug coverage, the ACA aims to address health issues early and effectively, leading to better health and lower costs for Americans.

Understanding Health Net Insurance: Benefits, Coverage, and Enrollment Guide

You may want to see also

Explore related products

![]()

Subsidy Eligibility: Explaining how subsidies can reduce Obamacare costs for low-income individuals

Subsidies play a crucial role in making health insurance under the Affordable Care Act (ACA), commonly known as Obamacare, more affordable for low-income individuals. These subsidies come in two primary forms: premium tax credits and cost-sharing reductions. Premium tax credits help lower the monthly cost of insurance premiums, while cost-sharing reductions decrease the amount policyholders pay out-of-pocket for deductibles, copayments, and coinsurance.

To be eligible for these subsidies, individuals must meet certain income criteria. Generally, premium tax credits are available to those with incomes between 100% and 400% of the federal poverty level (FPL). Cost-sharing reductions are typically offered to those with incomes up to 250% of the FPL. These income limits can vary slightly by state and are adjusted annually based on inflation.

The amount of subsidy an individual receives depends on their income and the cost of insurance in their area. For example, someone with an income at 150% of the FPL may receive a larger premium tax credit than someone with an income at 350% of the FPL. Similarly, cost-sharing reductions are more substantial for those with lower incomes.

Applying for subsidies involves filling out an application through the health insurance marketplace, either online, by phone, or in person. Applicants will need to provide proof of income and other personal information to determine their eligibility. Once approved, the subsidies are applied directly to the insurance plan, reducing the overall cost for the policyholder.

It's important to note that subsidies are not automatic and must be applied for each year during the open enrollment period. Additionally, changes in income or other circumstances can affect subsidy eligibility, so it's crucial for policyholders to update their information annually to ensure they receive the correct amount of assistance.

In conclusion, subsidies are a key component of the ACA, helping to make health insurance more accessible and affordable for low-income individuals. By understanding the eligibility criteria and application process, those who qualify can take advantage of these financial aids to reduce their healthcare costs.

Do Health Insurances Earn Profit? Uncovering the Financial Dynamics

You may want to see also

Explore related products

$47.51

![]()

Long-Term Affordability: Discussing the sustainability of Obamacare's cost structure over time

The long-term affordability of Obamacare is a critical aspect of its sustainability. While the initial rollout of the Affordable Care Act (ACA) focused on expanding coverage and controlling costs in the short term, the question remains whether these measures can be maintained over the long haul. One key factor in assessing the ACA's long-term affordability is its ability to balance the competing demands of providing comprehensive coverage while keeping premiums and out-of-pocket costs manageable for consumers.

To achieve this balance, the ACA implemented several cost-containment measures, such as the establishment of health insurance exchanges, the introduction of value-based care models, and the imposition of caps on out-of-pocket expenses. However, the effectiveness of these measures in controlling costs over the long term is still a subject of debate. Critics argue that the ACA's cost structure is unsustainable, citing rising premiums and the potential for increased government spending as evidence. Proponents, on the other hand, point to the ACA's success in reducing the uninsured rate and argue that the law's cost-containment measures will ultimately lead to long-term savings.

One potential challenge to the ACA's long-term affordability is the aging population. As the number of older Americans increases, so too will the demand for healthcare services, which could drive up costs. Additionally, the ACA's reliance on younger, healthier individuals to subsidize the costs of older, sicker individuals may become increasingly untenable as the population ages. To address these challenges, policymakers may need to consider additional cost-containment measures, such as increasing the age at which individuals are eligible for Medicare or implementing more stringent cost-sharing requirements.

Another factor that could impact the ACA's long-term affordability is the ongoing debate over the role of government in healthcare. While the ACA represents a significant expansion of government involvement in the healthcare market, there are those who argue that a more market-based approach would be more sustainable in the long run. This debate is likely to continue, with potential implications for the ACA's cost structure and overall affordability.

In conclusion, the long-term affordability of Obamacare is a complex issue that depends on a variety of factors, including the effectiveness of cost-containment measures, the aging population, and the ongoing debate over the role of government in healthcare. While the ACA has made significant strides in expanding coverage and controlling costs in the short term, the question of whether these gains can be sustained over the long haul remains open.

Does Health Insurance Cover Hepatitis B Vaccines? What You Need to Know

You may want to see also

Frequently asked questions

Obamacare, officially known as the Affordable Care Act (ACA), is a healthcare reform law that aims to provide more Americans with access to affordable health insurance. It includes provisions such as subsidies for lower-income individuals, the ability for young adults to stay on their parents' plans until age 26, and the prohibition of insurance companies denying coverage based on pre-existing conditions. These measures are designed to make health insurance more accessible and potentially less expensive for many people.

Obamacare provides financial assistance in the form of premium tax credits to help lower-income individuals and families afford health insurance. These subsidies can significantly reduce the monthly premium costs for those who qualify. For middle-income individuals, the impact on costs can vary depending on factors such as age, location, and the specific plan chosen. Some may find that their premiums increase, while others may benefit from the subsidies or other ACA provisions. Higher-income individuals may not receive subsidies and could potentially face higher premiums due to the redistribution of costs to support the ACA's goals.

Yes, Obamacare has several other provisions that can influence health insurance expenses. For example, the law requires insurance plans to cover essential health benefits, which may increase the cost of premiums for some plans. Additionally, the ACA imposes fees on insurance companies and healthcare providers, which could be passed on to consumers in the form of higher premiums. However, the law also promotes preventive care and wellness programs, which can help reduce overall healthcare costs in the long run. The impact of these various provisions on individual health insurance expenses can vary widely based on personal circumstances and the specific plan chosen.