The question of whether pre-tax health insurance is subject to social security tax is an important one for both employers and employees. Pre-tax health insurance refers to health insurance premiums that are deducted from an employee's paycheck before taxes are applied. This can provide a significant tax advantage, as it reduces the employee's taxable income. However, the rules surrounding social security tax can be complex, and it's essential to understand how they apply to pre-tax health insurance. In general, social security tax is applied to an employee's wages, which includes most forms of compensation. However, there are some exceptions and nuances when it comes to health insurance premiums. To fully understand the implications, it's necessary to delve into the specifics of the tax code and how it defines taxable wages.

| Characteristics | Values |

|---|---|

| Type of Income | Pre-tax health insurance premiums |

| Tax Applicability | Subject to Social Security tax |

| Federal Law | Internal Revenue Code (IRC) Section 3121(a)(5) |

| Purpose | To provide health coverage to employees |

| Employer Mandate | Often required under employer-sponsored health plans |

| Employee Contribution | May be deducted from employee's gross income |

| Tax Rate | 6.2% for Social Security tax (as of 2023) |

| Cap on Taxable Amount | Subject to annual wage base limit ($147,000 in 2023) |

| State Law Variations | Some states may have additional taxes or exemptions |

| Impact on Benefits | Does not affect the benefits received under the health plan |

| Reporting Requirements | Employers must report health insurance premiums on Form W-2 |

| Compliance | Employers must comply with IRS regulations and guidelines |

| Exceptions | Certain exceptions may apply, such as for self-insured plans |

| Historical Context | Pre-tax health insurance has been a common benefit since the mid-20th century |

| Economic Impact | Can influence employee's take-home pay and employer's payroll taxes |

| Policy Debate | Ongoing discussions about the fairness and efficiency of pre-tax health insurance |

| Alternatives | Post-tax health insurance, health savings accounts (HSAs), flexible spending accounts (FSAs) |

Explore related products

What You'll Learn

![]()

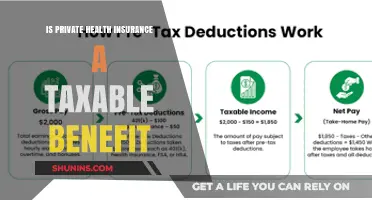

Definition of pre-tax health insurance

Pre-tax health insurance refers to health insurance premiums that are paid with pre-tax dollars, typically through a payroll deduction. This means that the money used to pay for the insurance is taken from an employee's paycheck before taxes are calculated, reducing the employee's taxable income. As a result, the employee pays less in federal income tax, and the employer also saves on payroll taxes.

One of the key benefits of pre-tax health insurance is that it can make health insurance more affordable for employees. By reducing the amount of taxable income, employees can save money on their tax bill, which can help offset the cost of health insurance premiums. Additionally, pre-tax health insurance can also benefit employers by reducing their payroll tax liability.

However, it's important to note that pre-tax health insurance is subject to certain rules and regulations. For example, the amount of pre-tax dollars that can be used for health insurance premiums is limited by the IRS. Additionally, pre-tax health insurance is only available to employees who are enrolled in a qualified health plan.

In terms of social security tax, pre-tax health insurance premiums are generally not subject to social security tax. This is because social security tax is calculated based on an employee's gross income, which is the total amount of money earned before any deductions are taken. Since pre-tax health insurance premiums are deducted from an employee's paycheck before taxes are calculated, they are not included in the employee's gross income and are therefore not subject to social security tax.

However, there are some exceptions to this rule. For example, if an employee's pre-tax health insurance premiums exceed the IRS limit, the excess amount may be subject to social security tax. Additionally, if an employee is enrolled in a health plan that is not qualified, their pre-tax health insurance premiums may also be subject to social security tax.

In conclusion, pre-tax health insurance can be a valuable benefit for both employees and employers, but it's important to understand the rules and regulations surrounding it. By taking advantage of pre-tax health insurance, employees can save money on their tax bill and make health insurance more affordable, while employers can also benefit from reduced payroll tax liability.

Does Your Health Insurance Cover Viagra? What You Need to Know

You may want to see also

Explore related products

![]()

Social Security tax applicability

In the context of employer-sponsored health insurance, the premiums paid by the employer are typically not subject to Social Security tax. This is because these premiums are considered a fringe benefit and are exempt from taxation under the Social Security Act. However, there are certain exceptions to this rule, such as when the premiums are paid for a non-employee or when the insurance plan is not a qualified plan under the Internal Revenue Code.

For individuals who are self-employed, the rules are different. Self-employed individuals are required to pay Social Security tax on their net earnings from self-employment, which includes any income earned from their business. This means that if a self-employed individual purchases health insurance premiums with pre-tax dollars, they may be subject to Social Security tax on those premiums.

It's also important to note that the Affordable Care Act (ACA) has introduced additional complexities to the tax treatment of health insurance premiums. For example, the ACA requires employers to report the value of health insurance premiums on employees' W-2 forms, which can impact the calculation of Social Security tax.

In conclusion, understanding the Social Security tax applicability of pre-tax health insurance is essential for both employers and individuals. By navigating the complex rules and regulations surrounding this topic, taxpayers can ensure compliance with the law and avoid potential penalties.

Student Medical Insurance: Is It a Must-Have?

You may want to see also

Explore related products

![]()

Employer-provided health insurance

When it comes to the tax implications of employer-provided health insurance, it's important to understand that the premiums paid by the employer are generally considered a tax-deductible business expense. This means that the employer can reduce their taxable income by the amount of the premiums paid. For employees, the portion of the premiums paid by the employer is not considered taxable income, which can result in significant tax savings.

However, it's crucial to note that the tax-free status of employer-provided health insurance premiums does not extend to Social Security taxes. While the premiums are not subject to federal income tax, they are still subject to Social Security and Medicare taxes. This is because these taxes are considered separate from federal income tax and are used to fund specific government programs.

In recent years, there have been changes to the tax laws surrounding employer-provided health insurance. For example, the Affordable Care Act (ACA) introduced new requirements for employers to provide health insurance to their employees or face penalties. Additionally, the Tax Cuts and Jobs Act (TCJA) made changes to the tax deductions available for employer-provided health insurance premiums.

Overall, employer-provided health insurance can be a valuable benefit for both employers and employees. However, it's important to understand the tax implications of this type of insurance, including the fact that while premiums are not subject to federal income tax, they are still subject to Social Security and Medicare taxes. By staying informed about the latest tax laws and regulations, employers and employees can make the most of this important benefit.

No Health Insurance? How It Impacts Your Income Tax Fines

You may want to see also

Explore related products

![]()

Employee contributions and FICA

Employee contributions towards health insurance premiums are generally not subject to FICA taxes, which include Social Security and Medicare taxes. This is because these contributions are typically made on a pre-tax basis, meaning they are deducted from the employee's gross income before taxes are applied. As a result, the employee's taxable income is reduced by the amount of their health insurance contributions, providing a tax advantage.

However, there are certain circumstances where employee health insurance contributions may be subject to FICA taxes. For example, if an employer offers a health insurance plan that is not considered a qualified plan under IRS regulations, the employee's contributions may be taxable. Additionally, if an employee's health insurance contributions exceed the maximum allowable amount for tax-free treatment, the excess contributions may be subject to FICA taxes.

Employers are responsible for withholding FICA taxes from employee wages, including any taxable health insurance contributions. To determine whether employee health insurance contributions are subject to FICA taxes, employers must carefully review the terms of their health insurance plans and consult with tax professionals if necessary.

In summary, while employee contributions towards health insurance premiums are generally not subject to FICA taxes, there are exceptions to this rule. Employers must be aware of these exceptions and ensure that they are properly withholding FICA taxes from employee wages to avoid potential penalties and legal issues.

Understanding the Health Insurance Industry: Sector, Role, and Impact

You may want to see also

Explore related products

$9.95 $9.95

![Social Security Bible for Beginners: [2 in 1] Insider Tips To Maximize Benefits And Ensure A Secure Retirement | + A Workbook For Easy, Step-By-Step Guidance And Financial Planning Tools](https://m.media-amazon.com/images/I/71KiivjGQhL._AC_UY218_.jpg)

![]()

Tax implications for businesses

Businesses must carefully consider the tax implications of offering pre-tax health insurance to their employees. One key aspect to understand is that pre-tax health insurance premiums are generally not subject to Social Security tax. This can result in significant savings for both employers and employees, as Social Security tax rates are currently 6.2% for employees and 6.2% for employers, up to a certain wage base limit.

However, it's important to note that while pre-tax health insurance premiums may be exempt from Social Security tax, they are still subject to other taxes, such as federal income tax and state taxes, depending on the jurisdiction. Employers should consult with a tax professional to ensure they are properly accounting for and withholding all applicable taxes.

Additionally, businesses should be aware of the potential impact of pre-tax health insurance on their employees' overall tax liability. While pre-tax premiums can reduce an employee's taxable income, they may also affect eligibility for certain tax credits or deductions, such as the Earned Income Tax Credit or the deduction for medical expenses. Employers should consider providing resources or guidance to help employees understand the tax implications of their health insurance choices.

Another factor to consider is the potential for pre-tax health insurance to influence employee behavior. For example, employees may be more likely to opt for pre-tax premiums if they perceive it as a tax-saving opportunity, even if it may not be the best choice for their individual circumstances. Employers should carefully communicate the benefits and drawbacks of pre-tax health insurance to ensure employees are making informed decisions.

In conclusion, while pre-tax health insurance can offer tax advantages for businesses and their employees, it's crucial to carefully navigate the complex tax landscape and consider the broader implications for employee financial well-being. By doing so, businesses can make informed decisions that benefit both their organization and their workforce.

Southwest Medical Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Generally, health insurance premiums paid before taxes (pre-tax) are not subject to social security tax. However, there are specific conditions and exceptions that may apply depending on the jurisdiction and the type of health insurance plan.

Exceptions to this rule can include certain types of health insurance plans, such as those that are part of a cafeteria plan or a flexible spending arrangement (FSA). In these cases, the portion of the premium that is paid with pre-tax dollars may be subject to social security tax.

The Affordable Care Act (ACA) introduced several changes to the taxation of health insurance premiums. For example, it imposed a tax on high-value health insurance plans, which is often referred to as the "Cadillac tax." This tax applies to both employer-sponsored and individual health insurance plans with premiums that exceed certain thresholds.

Pre-tax health insurance premiums are paid with dollars that have not yet been taxed, while post-tax health insurance premiums are paid with dollars that have already been taxed. Pre-tax premiums are generally more advantageous from a tax perspective, as they can reduce the amount of income that is subject to taxation. However, there are limits and conditions that apply to pre-tax premiums, and it's important to consult with a tax professional to understand the specific rules and implications.