The topic of whether the health insurance penalty is a monthly or one-time fee is an important aspect of understanding the financial implications of not having health coverage. Under the Affordable Care Act (ACA), individuals who do not maintain minimum essential health coverage may be subject to a penalty. This penalty is typically assessed on a monthly basis for each month that an individual is without coverage. However, the specific details of the penalty, including its amount and how it is calculated, can vary depending on factors such as income, age, and the number of months without coverage. It is essential to be aware of these details to make informed decisions about health insurance and to avoid unexpected financial burdens.

| Characteristics | Values |

|---|---|

| Type of Fee | The health insurance penalty can be either a monthly fee or a one-time fee, depending on the specific insurance plan and policy. |

| Monthly Fee Amount | Varies by insurance provider and plan, typically a fixed amount deducted from the policyholder's bank account or added to the monthly premium. |

| One-Time Fee Amount | Usually a lump sum paid upfront, which may be a percentage of the annual premium or a fixed amount set by the insurer. |

| Frequency of Payment | Monthly fees are paid every month, while one-time fees are paid annually or at the beginning of the policy term. |

| Impact on Premium | Monthly penalties may increase the overall cost of the insurance premium, while one-time fees are usually included in the total annual premium. |

| Late Payment Consequences | Failure to pay monthly fees on time may result in late fees, interest charges, or even policy cancellation. Late payment of one-time fees may also incur penalties and interest. |

| Prorated Fees | If a policyholder cancels their insurance mid-term, they may be subject to prorated fees for the remaining months of the policy term. |

| Refundability | One-time fees are generally non-refundable, while monthly fees may be refunded if the policy is cancelled before the end of the billing cycle. |

| Tax Implications | Health insurance penalties may have tax implications, depending on the jurisdiction and the specific circumstances of the policyholder. |

| Waivers and Exemptions | Some insurance plans may offer waivers or exemptions for certain policyholders, such as those experiencing financial hardship or those who qualify for subsidies. |

| Notification Requirements | Insurers are typically required to notify policyholders of any changes to fees or penalties, including the amount and effective date of the change. |

| Dispute Resolution | Policyholders may have the right to dispute fees or penalties they believe are unfair or inaccurate, through a formal appeals process. |

| Regulatory Oversight | Health insurance fees and penalties are often subject to regulatory oversight, ensuring that they are fair, transparent, and comply with applicable laws and regulations. |

| Comparison Shopping | When comparing insurance plans, it's important for policyholders to consider both the monthly and one-time fees, as well as the overall cost and benefits of the plan. |

| Financial Planning | Understanding the structure of health insurance fees and penalties can help policyholders make informed decisions about their healthcare coverage and budget accordingly. |

Explore related products

What You'll Learn

- Monthly Penalty: Discuss if the health insurance penalty is assessed monthly

- One-Time Fee: Explore if the penalty is a one-time payment

- Penalty Calculation: Explain how the penalty amount is determined

- Exemptions: List possible exemptions from paying the health insurance penalty

- Impact on Premiums: Analyze if the penalty affects future insurance premiums

![]()

Monthly Penalty: Discuss if the health insurance penalty is assessed monthly

The health insurance penalty, often a subject of confusion, is typically assessed on a monthly basis. This means that individuals who fail to maintain adequate health coverage may face a recurring charge each month. The rationale behind a monthly penalty is to encourage continuous compliance with health insurance requirements, ensuring that individuals remain covered and contributing to the overall healthcare system.

One key aspect to consider is the cumulative nature of the monthly penalty. Over time, these penalties can add up, potentially resulting in a significant financial burden for those who remain uninsured. For instance, if the monthly penalty is $100, an individual who goes without insurance for a year would accrue $1,200 in penalties. This underscores the importance of maintaining consistent health coverage to avoid substantial financial repercussions.

It's also worth noting that the monthly penalty structure may vary depending on the specific health insurance regulations in place. Some jurisdictions might impose a flat monthly rate, while others could use a tiered system based on factors such as income or the length of time an individual has been without insurance. Understanding these nuances is crucial for individuals navigating the complexities of health insurance penalties.

In contrast to a monthly penalty, a one-time fee would be a single, lump-sum payment. This approach could potentially be less burdensome for some individuals, as it would not require ongoing financial commitment. However, the effectiveness of a one-time fee in promoting continuous health insurance coverage is debatable, as it may not provide the same level of incentive as a recurring monthly penalty.

Ultimately, the debate surrounding whether the health insurance penalty should be monthly or a one-time fee hinges on various factors, including policy goals, individual financial circumstances, and the overall healthcare landscape. As it stands, the monthly penalty remains a prevalent approach, emphasizing the importance of sustained health insurance coverage and the potential financial consequences of non-compliance.

Medical Tourism Insurance: Protecting Your Health Abroad

You may want to see also

Explore related products

![]()

One-Time Fee: Explore if the penalty is a one-time payment

The concept of a one-time fee in the context of health insurance penalties is often misunderstood. Typically, penalties for not having health insurance are assessed on a monthly basis. However, there are certain circumstances under which a one-time fee might be applicable. For instance, if an individual fails to enroll in health insurance during the open enrollment period, they may be subject to a one-time penalty. This penalty is usually calculated based on the number of months the individual was without coverage.

It's important to note that the specifics of health insurance penalties can vary significantly depending on the country and the particular health insurance system in place. In some cases, the penalty might be a flat fee, while in others, it could be a percentage of the individual's income. Understanding the nuances of these penalties is crucial for making informed decisions about health insurance coverage.

To explore whether a health insurance penalty is a one-time fee, individuals should first consult the terms and conditions of their health insurance policy. This document will outline the specific penalties for late enrollment or lapses in coverage. Additionally, individuals can reach out to their health insurance provider directly to inquire about the penalty structure. It's also advisable to stay informed about any changes to health insurance laws and regulations that could impact penalty fees.

In conclusion, while health insurance penalties are often assessed on a monthly basis, there are scenarios in which a one-time fee might be applicable. By carefully reviewing policy documents and staying informed about health insurance regulations, individuals can better understand and manage potential penalties.

Travel Medical Insurance: Europe's Best Plans

You may want to see also

Explore related products

![]()

Penalty Calculation: Explain how the penalty amount is determined

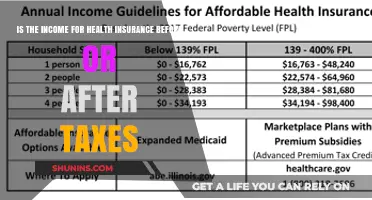

The penalty amount for health insurance is calculated based on a percentage of your annual income. This percentage is determined by the government and can vary depending on the year and your specific circumstances. For example, in 2023, the penalty was 2.5% of your annual income or $695 per adult, whichever is higher. This means that if your annual income is $50,000, your penalty would be $1,250 ($50,000 x 2.5%). However, if your annual income is $20,000, your penalty would be $695, as this is the minimum amount per adult.

It's important to note that the penalty is not a one-time fee, but rather a monthly charge that is added to your health insurance premium. This means that if you are uninsured for an entire year, you will be responsible for paying the penalty for each month of that year. For example, if your annual income is $50,000 and you are uninsured for all of 2023, you would be responsible for paying a penalty of $1,250 per month, for a total of $15,000 for the year.

There are some exceptions to the penalty, such as if you are below a certain income threshold or if you have a hardship exemption. Additionally, the penalty may be waived if you are uninsured for less than three months of the year. It's important to check with the government or a healthcare professional to determine if you are eligible for any of these exceptions.

In conclusion, the penalty amount for health insurance is determined by a percentage of your annual income and is added to your monthly premium. It's important to understand how the penalty is calculated and to explore any possible exceptions to avoid incurring unnecessary costs.

Renewing Your NYS Health Insurance: A Step-by-Step Guide to Stay Covered

You may want to see also

Explore related products

![]()

Exemptions: List possible exemptions from paying the health insurance penalty

Certain individuals may be exempt from paying the health insurance penalty under specific circumstances. One such exemption is for those who have a hardship exemption approved by the marketplace or their state. This could include situations where an individual has experienced a serious personal or financial hardship that prevented them from obtaining health insurance.

Another exemption is for individuals who are not required to file a tax return because their income is below the filing threshold. In this case, they would not be subject to the penalty for not having health insurance. Additionally, individuals who are eligible for Medicaid or the Children's Health Insurance Program (CHIP) but have not yet enrolled may also be exempt from the penalty.

Individuals who are members of certain religious groups, such as the Amish or Mennonite communities, may also be exempt from the health insurance penalty. These groups often have their own health care systems and do not participate in the mainstream health insurance market.

Furthermore, individuals who are not U.S. citizens or permanent residents may be exempt from the penalty if they are not required to have health insurance under the Affordable Care Act. This could include individuals who are in the country on a temporary visa or those who are undocumented immigrants.

It's important to note that these exemptions are subject to change and may vary depending on the specific circumstances of each individual. It's always best to consult with a tax professional or health insurance expert to determine if you are eligible for an exemption from the health insurance penalty.

UTI Without Insurance: Affordable Treatment Options and Home Remedies

You may want to see also

Explore related products

![]()

Impact on Premiums: Analyze if the penalty affects future insurance premiums

The impact of the health insurance penalty on future premiums is a critical aspect to consider when evaluating the overall cost of health coverage. While the penalty itself may be a one-time fee or a monthly charge, its implications on insurance premiums can be far-reaching. Insurance companies often view individuals who have incurred penalties as higher-risk clients, which can lead to increased premium rates. This is because the penalty is typically associated with a lack of continuous coverage, which may indicate to insurers that the individual is more likely to file claims or require more expensive medical treatments in the future.

To analyze the specific impact on premiums, it's essential to understand the factors that influence insurance rates. These factors include age, health status, location, and the type of coverage selected. Additionally, the duration and severity of any lapses in coverage can significantly affect premium costs. For instance, a brief lapse in coverage due to a one-time penalty may result in a minor increase in premiums, whereas a prolonged period without insurance could lead to a substantial hike in rates.

It's also important to note that the health insurance market is highly competitive, and different insurers may have varying policies regarding penalties and premium increases. Some insurers may offer more lenient terms for individuals who have incurred penalties, while others may take a stricter approach. Therefore, it's crucial for individuals to shop around and compare quotes from multiple insurers to find the most affordable coverage options.

In conclusion, the health insurance penalty can have a significant impact on future premiums, as insurers may view penalized individuals as higher-risk clients. To mitigate this impact, it's essential to maintain continuous coverage, compare quotes from different insurers, and consider factors such as age, health status, and location when selecting a health insurance plan. By taking these steps, individuals can minimize the financial consequences of the penalty and ensure they have access to affordable health coverage.

Medicare Supplemental Insurance: AARP's Popularity Explained

You may want to see also

Frequently asked questions

The health insurance penalty, also known as the individual mandate, was typically assessed as a monthly fee. However, it's important to note that the penalty was eliminated starting with the 2019 tax year.

The penalty was calculated based on the number of months you were without health insurance. For each month, the penalty was either a flat fee or a percentage of your income, whichever was higher.

The purpose of the penalty was to encourage individuals to maintain health insurance coverage. It was part of the Affordable Care Act (ACA), which aimed to increase access to healthcare and reduce the number of uninsured people.

As of now, there is no federal penalty for not having health insurance. However, some states have implemented their own individual mandates and penalties. Additionally, being uninsured can lead to significant financial risks in the event of a medical emergency or illness.