Medicare Supplement Insurance, also known as Medigap, is extra insurance offered by private companies to help cover out-of-pocket costs not included in Original Medicare (Part A and Part B). Medigap policies are standardized and named by letters like Plan G or Plan K, with each lettered plan offering the same benefits regardless of the insurance company. Generally, individuals must have Original Medicare before purchasing Medigap, and it's important to compare policies as costs can vary. Medigap policies do not cover long-term care, vision, dental, hearing aids, private nursing, or prescription drugs, but some policies offer additional benefits and coverage for travel outside the U.S.

| Characteristics | Values |

|---|---|

| Name | Medicare Supplement Insurance (Medigap) |

| Type | Extra insurance to supplement Original Medicare |

| Provider | Private insurance companies |

| Eligibility | Must have Original Medicare Part A and Part B; must be 65 or older |

| Coverage | Covers out-of-pocket costs not covered by Original Medicare, such as copays, coinsurance, and deductibles; some plans offer coverage for travel outside the U.S. |

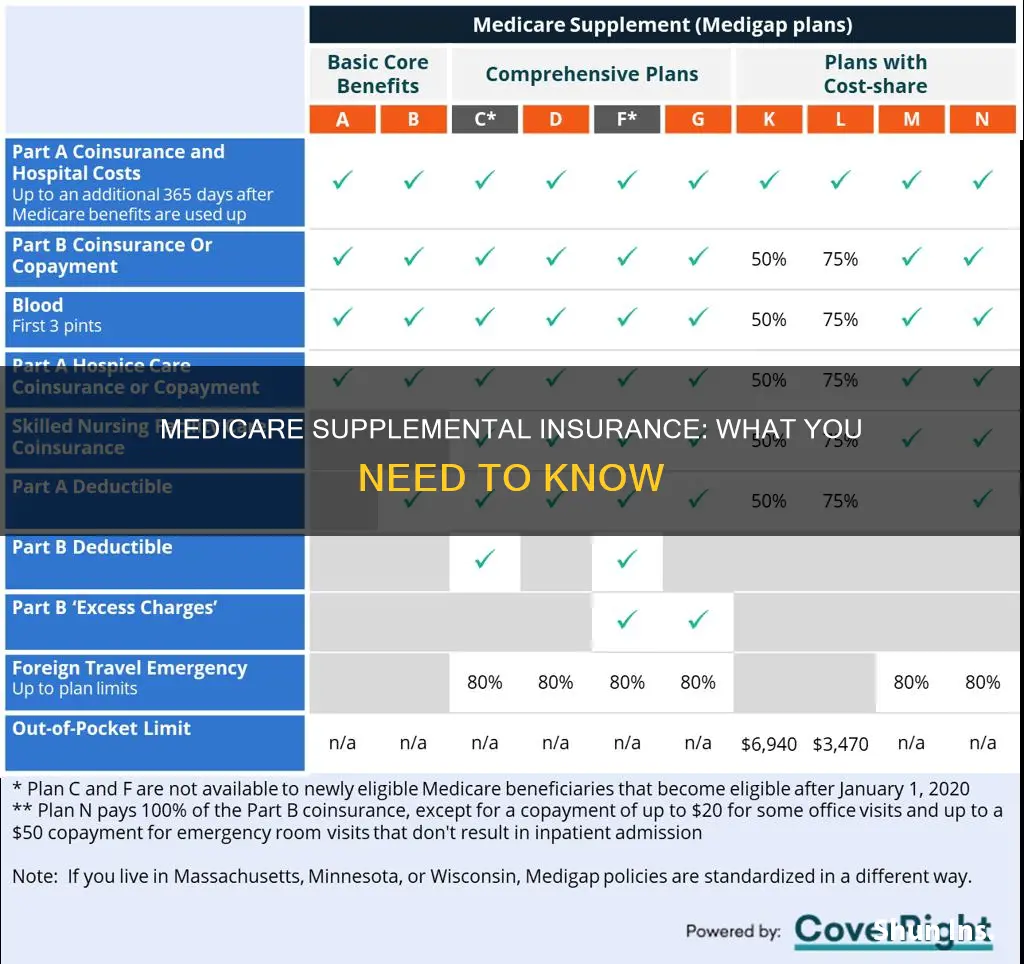

| Plans | Standardized with 10 types of plans offered in most states, named by letters: A-D, F, G, and K-N; price is the main differentiating factor between plans |

| Enrollment | Features a 6-month open enrollment period for those eligible; after this period, enrollment may be restricted or cost more |

| Cancellation | Cannot be canceled as long as premiums are paid on time and there is no material misrepresentation |

| Flexibility | Allows freedom to see any healthcare provider that accepts Medicare patients without needing referrals |

Explore related products

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help cover out-of-pocket costs in Original Medicare (Parts A and B). Medigap plans are designed to fill the coverage gaps in Original Medicare and help pay for expenses such as deductibles, copays, and coinsurance. These plans are available in all 50 states and Washington, D.C., and the cost of premiums and enrollment eligibility may vary. It is important to note that Medigap policies are not connected with or endorsed by the U.S. government or the federal Medicare program.

To be eligible for Medicare Supplement Insurance, individuals must generally be enrolled in Original Medicare (Part A and Part B) and be aged 65 or older. In some states, those under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease may also purchase Medigap plans. Additionally, Medigap enrollees must continue paying their Part B premium in addition to the premium for their Medigap coverage.

Medigap plans are standardized, but the specific benefits and coverage may vary. Plans A through G typically offer higher benefits at higher premiums, while Plans K through N are cost-sharing plans with lower premiums and higher out-of-pocket costs. It is important to carefully review the details of each plan, as some may not be available in certain areas. Additionally, Medigap plans may cover foreign travel emergency services, and some offer high-deductible options.

If you already have Medigap insurance, you have the flexibility to switch plans. The "Birthday Rule" allows a 60-day window of open enrollment following your birthday each year, during which you can purchase a new Medigap policy with the same or lesser benefits without undergoing a medical screening or waiting period. To make informed decisions about Medigap plans, it is recommended to consult licensed insurance agents or official government resources, such as the U.S. Government Site for People with Medicare.

Supplement Insurance: Enhancing Your Medicare Coverage

You may want to see also

Explore related products

![]()

Eligibility

Medicare Supplement Insurance, also known as Medigap, is an additional insurance policy that can be purchased to help cover out-of-pocket costs in Original Medicare (Parts A and B). To be eligible for Medigap, you must already have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance).

Part A:

- Age-based eligibility: Individuals aged 65 or older may be eligible for premium-free Part A if they, or their spouse, parent, or child, have earned a specified number of quarters of coverage (QCs) through payroll taxes under the Federal Insurance Contributions Act (FICA) during their working years.

- Disability or End-Stage Renal Disease (ESRD): Individuals under 65 may be eligible for premium-free Part A if they have a qualifying disability or ESRD, and they, or their spouse, parent, or child, have earned the required number of QCs.

- Volunteer service exception: Individuals who did not enroll in Part A when first eligible due to performing volunteer service outside the US for at least 12 months for a tax-exempt organization and had health insurance coverage during that period may be eligible for a Special Enrollment Period (SEP).

Part B:

- Age-based eligibility: Similar to Part A, individuals aged 65 or older who are receiving monthly Social Security or Railroad Retirement Board (RRB) benefits at least four months before turning 65 will automatically receive Part B. Those not receiving these benefits must enrol separately.

- Disability or ESRD: Similar to Part A, individuals under 65 with a qualifying disability or ESRD may be eligible for Part B.

- TRICARE enrollees: Individuals who enrol in Part A based on disability or ESRD and are eligible for TRICARE Standard or TRICARE Prime may enrol in Part B during the SEP.

Once enrolled in Original Medicare (Parts A and B), you are eligible to purchase a Medigap policy. It is important to note that Medigap policies are standardized, and the benefits offered are the same across insurance companies. The main difference between policies is the price. Additionally, individuals under 65 may face challenges in purchasing a Medigap policy or may have to pay higher premiums.

FICA Hospital Insurance: Does It Cover Bonuses?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

![]()

Costs

The cost of Medicare supplemental insurance plans, or Medigap, varies depending on location, insurance provider, and the type of plan chosen. Medigap plans cover certain copays, coinsurance, and deductibles that the policyholder would otherwise be responsible for after Medicare pays its share of covered services.

Medigap plans are lettered A to N, excluding E, H, I, and J. Plans with the same letter must offer the same level of coverage, even if the cost is different. The premium amount is the only difference between policies with the same plan letter sold by different companies. The average monthly premium among all Medicare supplement policyholders was $217. The monthly premium is the only factor that will differ between policies with the same letter. For example, Medigap Plan M offers the same benefits and coverage regardless of which company sells it, but one insurer may sell Plan M for $100 more monthly.

Medigap policies are purchased from private insurance companies, meaning that costs may vary according to state regulations, insurer choice, and personal circumstances, such as age. On the lower end, Medigap plans can cost $30-$40 per month. On the higher end, monthly premiums can get up into the hundreds of dollars. Generally, you’ll pay the lowest premiums for high-deductible plans or plans with less coverage, like Plan K or Plan L. Conversely, a plan that covers more, such as Plan G, tends to have a higher premium.

Some Medigap plans have additional costs beyond their premiums. For example, Medigap Plan N has copays for certain office visits and some emergency room visits, while Plan K and Plan L require you to pay for a percentage of most covered services. With Plan K, you pay 50% out of pocket, and with Plan L, you pay 25%. High-deductible plans require you to meet a deductible of $2,870 in 2025 before the Medigap policy pays for anything.

Your Medicare out-of-pocket costs can change yearly based on inflation, so it pays to research the best Medicare supplement insurance plans annually. The timing of enrollment can also make crucial differences to a person’s level of coverage and monthly cost. Some companies might exclude preexisting health problems or charge a higher premium for those without a guaranteed issue right or who apply outside the Medigap open enrollment period.

HealthPartners Medicaid: Abortion Coverage Explained

You may want to see also

Explore related products

![]()

Coverage

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can buy from a private health insurance company. It helps pay for your share of out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are designed to assist with costs such as deductibles, copays, and coinsurance that are not covered by Parts A and B. These policies are available across the United States and Washington, D.C., with some variation in premiums and enrollment eligibility.

To be eligible for a Medigap policy, you generally must have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Once you have signed up for Part A and Part B, you can choose between Original Medicare and Medicare Advantage. It's important to note that Medigap policies do not cover long-term care, such as nursing home stays, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, if you are under 65, there may be restrictions or higher costs for Medigap policies.

Medigap policies are standardized, and each policy must be clearly identified as "Medicare Supplement Insurance." The benefits offered in each plan are the same across different insurance companies, with the price being the only differentiating factor. Some Medigap policies offer additional coverage, such as when travelling outside the United States. You will need to continue paying your Part B premium and a separate premium for your Medigap coverage.

You can find out more about Medigap policies and their coverage by contacting your local State Health Insurance Assistance Program (SHIP), which provides free and personalized health insurance counselling. Additionally, you can explore Medicare coverage options offered by private insurance companies, such as Blue Cross and Blue Shield, by visiting their websites or entering your ZIP Code to find plans available in your area.

Vision Insurance: Is VSP Necessary with Medicare?

You may want to see also

Explore related products

$4.99 $19.99

$9.98 $10.99

![]()

Medicare Advantage

One of the key advantages of Medicare Advantage plans is that they often include benefits not covered by original Medicare, such as dental, vision, and prescription drug coverage. Some plans may also offer fitness program memberships, transportation to medical appointments, and even coverage for over-the-counter medications. These additional benefits can vary depending on the specific plan and the insurance company offering it, so it's important to carefully review the details of each plan before enrolling.

Another important feature of Medicare Advantage plans is their out-of-pocket cost structure. These plans usually have a set maximum for out-of-pocket expenses, which can provide peace of mind and help individuals budget for healthcare costs. Once the maximum is reached, the plan typically covers all additional expenses. Original Medicare does not have this feature, and out-of-pocket costs can accumulate indefinitely.

Enrolling in a Medicare Advantage plan is generally done during specific enrollment periods. The initial enrollment period is usually aligned with an individual's initial eligibility for Medicare. There are also annual enrollment periods, such as the Annual Election Period (AEP) from October 15 to December 7 each year, during which individuals can switch between Medicare Advantage plans or drop their current plan and return to original Medicare.

It is always advisable to thoroughly research the available Medicare Advantage plans in your area and compare their benefits, provider networks, and costs before enrolling. This ensures that you select a plan that best meets your specific healthcare needs and preferences. Additionally, reviewing your plan choices annually during the appropriate enrollment periods allows you to make any necessary adjustments to ensure you have the most suitable coverage.

Aflac Accident Insurance: Are Your Benefits Taxable?

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare.

Each Medicare Supplement Insurance plan has a different monthly premium. The monthly premium depends on the plan chosen and the benefits covered. Some plans have higher monthly premiums but cover most out-of-pocket costs, while others have lower monthly premiums and cover fewer out-of-pocket costs.

Medicare Supplemental Insurance helps cover some of the out-of-pocket healthcare costs that Original Medicare doesn't pay for. Most plans provide coverage for your Medicare Part A hospital deductible, but you are usually responsible for your Medicare Part B deductible and expenses.

You can choose and enroll in a Medicare Supplement Insurance plan online. You must have Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance), to buy a Medigap policy. In some states, plans may be available to persons under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease.

You are guaranteed the right to buy a Medigap policy under certain circumstances. For more information, you can call 1-800-633-4227 and ask for a free copy of the publication "Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare."