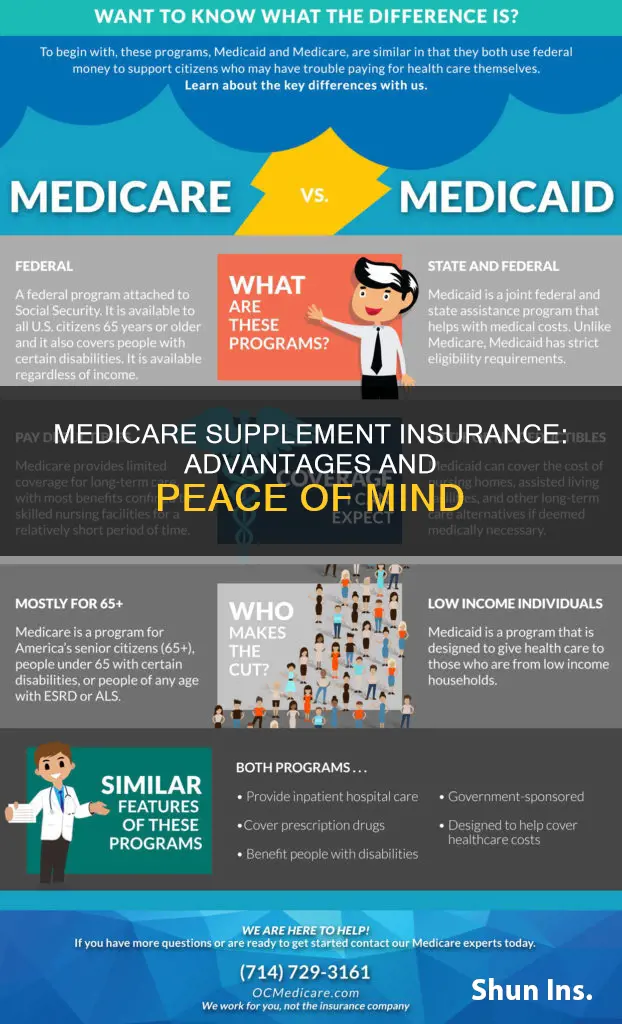

Medicare Supplement Insurance, also known as Medigap, is an additional insurance plan that covers the costs that Original Medicare (Part A and Part B) does not. Medigap covers copayments, coinsurance, and deductibles, and is available to those over 65 and those under 65 who are eligible for Medicare due to disability. There are up to 10 different Medigap plans available, with different monthly premiums, and it is recommended that you compare the prices of the same plan from different insurance companies to get the best price.

Explore related products

What You'll Learn

![]()

Fills gaps in Original Medicare

Medicare Supplement Insurance, also known as Medigap, is extra insurance that fills the gaps in Original Medicare. It helps pay for healthcare costs that Original Medicare doesn't cover, such as copays, coinsurance, and deductibles. These costs can include Part A inpatient hospital copayments and coinsurance, Part B coinsurance, hospice care, and preventive care.

Medigap policies are sold by private insurance companies and are standardized, offering the same benefits no matter which company sells them. The only difference between policies sold by different companies is the cost. Generally, to buy a Medigap policy, you must already have Original Medicare Part A (Hospital Insurance) and Part B (Medical Insurance).

Some Medigap policies also offer coverage for extra benefits that Original Medicare doesn't cover, such as certain vision, hearing, and dental services. Additionally, some Medigap policies provide coverage when travelling outside the U.S. However, it's important to note that Medigap generally doesn't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Medigap policies can give peace of mind, knowing that your benefits are guaranteed as long as you pay your premiums. The right Medigap plan depends on your specific needs and budget. It's important to compare policies from different companies to find the one that best suits your requirements.

Getting Medical Insurance for Your Parents: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Covers copays, coinsurance, and deductibles

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help cover out-of-pocket costs not covered by Original Medicare (Parts A and B). One of the key benefits of Medicare Supplement Insurance is that it covers copays, coinsurance, and deductibles, helping to reduce the financial burden on individuals.

Copays, or copayments, are the fees that individuals pay when they receive medical services, such as a doctor's visit or a hospital stay. Coinsurance, on the other hand, refers to the percentage of the total cost of a covered healthcare service that the individual is responsible for paying. Deductibles are the amounts individuals must pay out of pocket before their insurance coverage kicks in.

By covering copays, coinsurance, and deductibles, Medicare Supplement Insurance plans help individuals manage their healthcare expenses and reduce their financial risk in the event of unexpected medical costs. This additional coverage can provide peace of mind and help ensure that individuals can access the healthcare services they need without worrying about high out-of-pocket costs.

It's important to note that Medicare Supplement Insurance plans are standardized and offer guaranteed benefits as long as premiums are paid. However, the specific benefits and costs can vary across plans, so it's essential to carefully review and compare different plans before selecting one that best suits your needs and budget.

Medicare Supplement Insurance is a valuable option for individuals enrolled in Original Medicare, helping to fill the gaps in coverage and providing financial protection against unexpected medical expenses.

Accident Insurance: Critical Protection for the Unexpected

You may want to see also

Explore related products

![]()

Offers coverage when travelling outside the U.S

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps fill the "gaps" in Original Medicare. Medigap is sold by private insurance companies and generally requires Original Medicare Parts A and B to be eligible. While Medigap policies do not typically cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs, some policies offer additional benefits not included in Original Medicare, such as coverage when travelling outside the U.S.

Medigap policies offering coverage for travel outside the U.S. ensure that individuals are protected in case of unexpected medical needs during their international travels. This coverage can provide peace of mind and financial protection in the event of an emergency. The specific benefits and extent of coverage may vary among insurance providers, so it is essential to carefully review the policy details before purchasing.

International travel coverage under Medigap typically includes emergency medical services and supplies deemed necessary by a physician. This can include hospital stays, emergency room visits, ambulance services, and medical evacuation back to the United States if necessary. It is important to note that Medigap policies generally do not cover routine or elective medical services received outside the U.S.

The duration of coverage for travel outside the U.S. may vary depending on the Medigap policy. Some policies may offer coverage for a limited period, such as a set number of days or weeks per trip, while others may provide continuous coverage as long as the individual maintains their Medigap plan. Additionally, there may be specific requirements or limitations regarding the frequency or purpose of travel for coverage to apply.

When considering a Medigap policy with international travel coverage, it is crucial to understand any exclusions or limitations. For example, some policies may exclude coverage for pre-existing conditions or specific types of medical emergencies that occur during travel. Certain countries or regions may also be excluded from coverage due to political instability, natural disasters, or other factors. Reading the fine print and understanding the terms and conditions of the policy is essential to make an informed decision.

Understanding Guarantor Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Standardized policies with guaranteed benefits

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can purchase from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Generally, you must have Original Medicare – Part A (Hospital Insurance) and Part B (Medical Insurance) – before buying a Medigap policy.

Medigap policies are standardized and must follow federal and state laws. These laws are in place to protect you. The benefits in each lettered plan are the same, no matter which insurance company sells it. The price is usually the only difference between policies with the same letter sold by different companies. For instance, Plan A may differ in price from one insurer to another, but the benefits it offers remain unchanged.

The front of a Medigap policy must clearly identify it as “Medicare Supplement Insurance.” This standardization makes it easier for consumers to compare Medigap policies offered by different insurance companies. It also ensures that consumers are aware of the specific benefits associated with each plan, regardless of the insurer.

Some Medigap policies offer additional benefits not covered by Original Medicare, such as coverage when you travel outside the U.S. However, Medigap policies typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. It is important to note that if you are under 65, you may not be able to purchase a Medigap policy, or you may have to pay a higher price.

Consequences of Lying on Your Medical Insurance Forms

You may want to see also

Explore related products

![]()

Available from private insurance companies

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from private health insurance companies. It helps to pay for out-of-pocket costs in Original Medicare, such as copays, coinsurance, and deductibles. Generally, you must have Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance), to buy a Medigap policy.

Medigap policies are standardized and offer guaranteed benefits as long as you pay your premiums. The benefits in each plan are the same across different insurance companies, with the price being the only differentiating factor. Some Medigap policies also offer coverage for additional benefits that Original Medicare does not cover, such as certain vision, hearing, and dental services. These policies may also provide coverage when travelling outside the U.S.

It is important to note that Medigap policies typically do not cover long-term care, such as nursing home stays, private-duty nursing, or prescription drugs. Additionally, if you are under 65, purchasing a Medigap policy may be more challenging or expensive.

When considering a Medigap policy, it is recommended to compare plans from different private insurance companies to find the most competitive pricing, as the benefits offered are standardized across the industry.

Navigating Medical Insurance Claims in the USA

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is private health insurance that adds on to Original Medicare (Part A and B). It helps pay for the out-of-pocket costs that Original Medicare doesn't cover.

Medicare Supplement Insurance provides additional coverage to your Original Medicare benefits. It helps cover the out-of-pocket costs, such as copayments, coinsurance, and deductibles, that Original Medicare doesn't cover. It also offers nationwide coverage and is "guaranteed renewable", meaning your policy cannot be canceled if you pay your premium.

The best time to enroll is during your Medicare Supplement Open Enrollment period, which is a six-month period that starts the first month you are 65 or older and enrolled in Medicare Part B. During this time, you cannot be denied a policy based on health reasons, and insurance companies must offer the same price as those in good health.