Medicare Supplemental Insurance, also known as Medigap, is an additional insurance policy that can be purchased by seniors to supplement their existing Medicare coverage. While Medicare is the country's health insurance program for individuals aged 65 and over, it may not cover all medical expenses. This is where Medicare Supplemental Insurance comes into play, as it can help cover the gaps left by Medicare Part A and Part B, including medical-related needs such as doctor visits, hospital stays, and lab work. This additional coverage can provide peace of mind and help seniors avoid unnecessary out-of-pocket costs. Furthermore, Medicare Supplemental Insurance offers flexibility in choosing healthcare providers and enrollment periods, making it a popular option for seniors who want to ensure they have comprehensive protection as they age. However, it is not the only insurance option for seniors, and long-term care insurance is another important consideration for covering costs associated with assisted living and daily care activities.

| Characteristics | Values |

|---|---|

| Purpose | Fills the gap left by other insurance types, including Medicare Part A and Part B, to avoid unnecessary out-of-pocket costs |

| Provider Network | Does not restrict users to in-network or out-of-network providers |

| Enrollment | Users can change or enroll in a plan at any time of the year, and plans are guaranteed renewable |

| Coverage | Extends coverage for medical-related needs, including doctor visits, hospital stays, and lab work |

| Cost | Cost varies based on income and other factors; it may be more cost-effective to pay out-of-pocket for certain expenses |

| Age Requirements | No age restrictions, unlike Medicare, which is generally for people 65 or older |

| Alternatives | Long-term care insurance covers costs for assistance with daily living activities and can be purchased at any age |

Explore related products

What You'll Learn

![]()

Filling gaps in Original Medicare coverage

Medicare is the US health insurance program for people aged 65 or older. There are four types of Medicare coverage, known as "parts". Medicare Part A covers hospital insurance, while Part B covers medical insurance. However, Medicare may not cover everything the insured person needs. This is where Medicare supplemental insurance comes in.

Medicare supplemental insurance is an additional insurance policy that can be purchased from a private company. It helps fill the gap left by other insurance types, covering the remaining balance of out-of-pocket costs. It can extend coverage protections, ensuring policyholders are thoroughly protected and giving them peace of mind.

One of the benefits of Medicare supplemental insurance is that it does not limit your network of providers. This helps keep your care cohesive and consistent, allowing you to keep your provider as long as they are working with Medicare patients. Additionally, users can change or enrol in a plan at any time of the year, and the plans are guaranteed to be renewable. This is especially beneficial for those with pre-existing medical conditions or those who develop new conditions while enrolled, as their coverage will not be jeopardized.

While Medicare supplemental insurance can be a major help for older adults, it is not the only insurance type worth considering. Long-term care insurance, for example, can help cover the cost of care for assistance with daily living activities such as dressing, bathing, and daily care. It can also be useful for those who need financial assistance with nursing homes, assisted living facilities, or home caretakers.

In conclusion, Medicare supplemental insurance can be a valuable addition to Original Medicare coverage, helping to fill gaps in protection and giving policyholders peace of mind. However, it is important to consider other types of insurance, such as long-term care insurance, to ensure that all potential needs are covered.

Florida State Employee Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Avoiding restrictions on provider networks

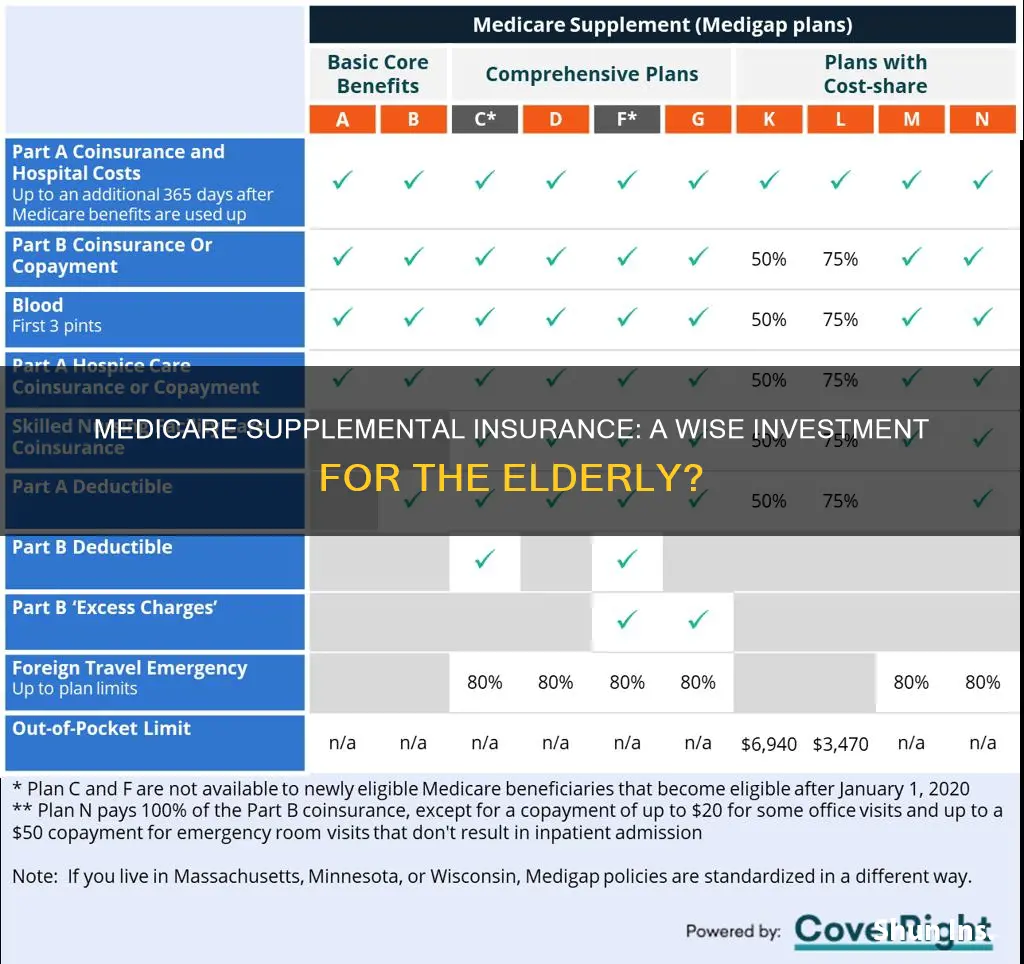

Medicare Supplement Insurance, also known as Medigap, is an additional insurance option that can be purchased from a private insurance company. It helps cover the out-of-pocket costs associated with Original Medicare (Parts A and B). Medigap policies are standardised, meaning that policies with the same letter offer identical basic benefits, regardless of the insurance company providing them. This ensures that beneficiaries can access a consistent level of care across different providers.

When considering Medicare Supplement Insurance, it is essential to understand the restrictions on provider networks. Original Medicare typically allows beneficiaries to see any doctor or healthcare provider who accepts Medicare. However, some Medicare Advantage plans offered by private companies may impose restrictions on provider networks. This means that beneficiaries may be limited to seeking care only from providers within the plan's network.

To avoid restrictions on provider networks, it is advisable to carefully review the terms and conditions of different Medicare Advantage plans before enrolling. Beneficiaries should ensure that their preferred doctors and healthcare providers are included in the plan's network. It is also important to be aware of any changes in the plan's provider network over time, as Medicare negotiates contracts with Medicare Advantage plans annually, which may result in fluctuations in the available benefits and providers.

Additionally, beneficiaries should be mindful of their guaranteed issue rights when considering Medicare Supplement Insurance. Under certain circumstances, individuals have a guaranteed right to purchase a Medigap policy without restrictions, such as pre-existing condition waiting periods or exclusions. For example, individuals who lose Medicaid due to changes in their financial situation have a guaranteed issue right to buy a Medicare supplement policy within 63 days of their coverage ending.

In conclusion, while Medicare Supplement Insurance can provide valuable additional coverage, it is important to carefully consider the potential restrictions on provider networks associated with different plans. Beneficiaries should review plan details, compare benefits, and be aware of their guaranteed issue rights to make informed decisions that ensure continued access to their preferred healthcare providers.

Health Insurance Fraud: Undisclosed Medical Conditions

You may want to see also

Explore related products

![]()

Peace of mind and stress reduction

Medicare supplemental insurance (also known as Medigap) is additional insurance that can be purchased from a private company to help fill these coverage gaps. It provides peace of mind and stress reduction by ensuring that seniors have comprehensive protection and avoiding unnecessary out-of-pocket costs. With Medigap, seniors can rest assured that they won't have to worry about financial burdens related to their healthcare.

One of the main advantages of Medicare supplemental insurance is that it covers medical-related needs that original Medicare might not fully cover, such as doctor visits, hospital stays, lab work, and more. This additional coverage ensures that seniors don't have to stress about unexpected medical expenses. Furthermore, Medigap policies can provide extended coverage protections, giving policyholders peace of mind knowing that they are thoroughly protected.

Another benefit of Medicare supplemental insurance is the flexibility it offers. Unlike some other insurance types, Medigap allows users to change or enroll in a plan at any time of the year, not just during specific enrollment periods. This flexibility is especially important for those with pre-existing medical conditions or those who develop new medical issues while enrolled. Medicare supplemental insurance guarantees renewable coverage, so seniors can have peace of mind knowing that their medical conditions won't jeopardize their ability to receive treatment.

While long-term care insurance and Medicare supplemental insurance serve different purposes, they can be complementary. Long-term care insurance covers costs associated with assistance in daily living activities, such as dressing, bathing, and cognitive decline, which may not be fully covered by Medicare. By having both types of insurance, seniors can ensure that they have comprehensive coverage for their medical and daily living needs, reducing financial stress and providing peace of mind as they age.

Colonial Accident Insurance: Comprehensive Coverage and Benefits

You may want to see also

Explore related products

![]()

Long-term care insurance vs. Medicare Supplemental Insurance

Medicare Supplemental Insurance, also known as Medigap, is an additional insurance policy that can be purchased from a private company to help cover the gaps in Original Medicare (Parts A and B) coverage. It helps pay for out-of-pocket costs, such as deductibles, coinsurance, and copayments, and can provide extended coverage protections for medical-related needs like doctor visits, hospital stays, and lab work. One of the advantages of Medigap is that it allows you to keep your preferred healthcare provider without being restricted by network guidelines. Additionally, Medigap policies can be purchased at any time of the year and are guaranteed renewable, which is beneficial for individuals with pre-existing medical conditions. However, Medigap generally does not cover long-term care expenses, such as nursing home care or assistance with daily living activities.

On the other hand, long-term care insurance serves a different purpose. It focuses on providing financial assistance for long-term care services, including medical and non-medical care for individuals with chronic illnesses or disabilities. Long-term care insurance typically covers the cost of assistance with daily living activities, such as dressing, bathing, and personal care. It can help seniors cover the costs of nursing homes, assisted living facilities, or home health care services. Unlike Medicare and Medigap, long-term care insurance does not have the same age restrictions and can be purchased by individuals under 65 who may need assistance earlier in life.

Both types of insurance serve distinct purposes and can be beneficial for seniors depending on their individual circumstances. While Medigap helps cover gaps in medical coverage, long-term care insurance ensures financial support for long-term care needs. Experts generally recommend having both types of insurance to achieve comprehensive protection during retirement. However, factors such as age, health status, financial situation, and existing coverage options like Medicaid or other retirement programs can influence the decision to purchase either or both types of insurance.

While Medicare Supplemental Insurance provides valuable coverage for out-of-pocket medical expenses, it may not be necessary for seniors who already have comprehensive medical coverage or those who are covered by programs like Medicaid. Additionally, healthy seniors who do not anticipate needing long-term care services may opt against purchasing long-term care insurance. It is important for individuals to carefully consider their personal needs, financial situation, and existing coverage before deciding whether to purchase Medicare Supplemental Insurance, long-term care insurance, or both.

Medical Insurance: Multi-State Coverage and Its Complexities

You may want to see also

Explore related products

![]()

Eligibility and enrolment periods

Medicare is the country's health insurance program for people aged 65 or older. However, you may also qualify if you have permanent kidney failure or receive disability benefits. There are four types of Medicare coverage, known as "parts". These include Part A (Hospital Insurance) and Part B (Medical Insurance).

Medicare supplemental insurance is an additional insurance policy that can be purchased from a private company to help fill the gap left by other insurance types and avoid unnecessary out-of-pocket costs. It can also extend coverage protections, giving policyholders peace of mind. It is important to note that Medicare supplemental insurance is not the only type of insurance worth considering. Long-term care insurance, for example, can be helpful for seniors who need financial assistance with nursing homes, assisted living facilities, or home caretakers.

To be eligible for Medicare supplemental insurance, you generally must already have Original Medicare – Part A and Part B. Unlike many other insurance types, Medicare supplemental insurance allows users to change or enrol in a plan at any time of the year, not just during select enrolment periods. This is especially beneficial for those with pre-existing medical conditions or those who develop such issues during their enrolment.

There are three enrolment periods for Medicare. It is recommended to sign up as soon as possible to avoid penalties or gaps in coverage.

Verify Your Medicare Insurance Coverage: Quick and Easy Steps

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is extra insurance purchased from a private health insurance company to cover out-of-pocket costs not covered by Original Medicare (Part A and Part B).

Medicare Supplemental Insurance can help cover medical-related needs, such as doctor visits, hospital stays, and lab work, that are not covered by Medicare. It can provide peace of mind by filling gaps in coverage and extending protection. Additionally, it offers flexibility by allowing users to change or enroll in a plan at any time of the year and guaranteeing renewable coverage, regardless of pre-existing conditions.

Long-term care insurance is an alternative or complementary option to Medicare Supplemental Insurance. It covers costs associated with assistance for daily living activities, such as dressing, bathing, and cognitive decline, which may not be covered by Medicare or Medicare Supplemental Insurance. It also does not have the same age restrictions, as it can be purchased before turning 65.

The decision to purchase Medicare Supplemental Insurance depends on various factors, including income, health status, and specific needs. While Medicare Supplemental Insurance can provide valuable coverage, it may not be necessary or cost-effective for everyone. It's important for seniors to carefully consider their financial situation, compare different insurance options, and assess their current and potential future health care needs.

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)