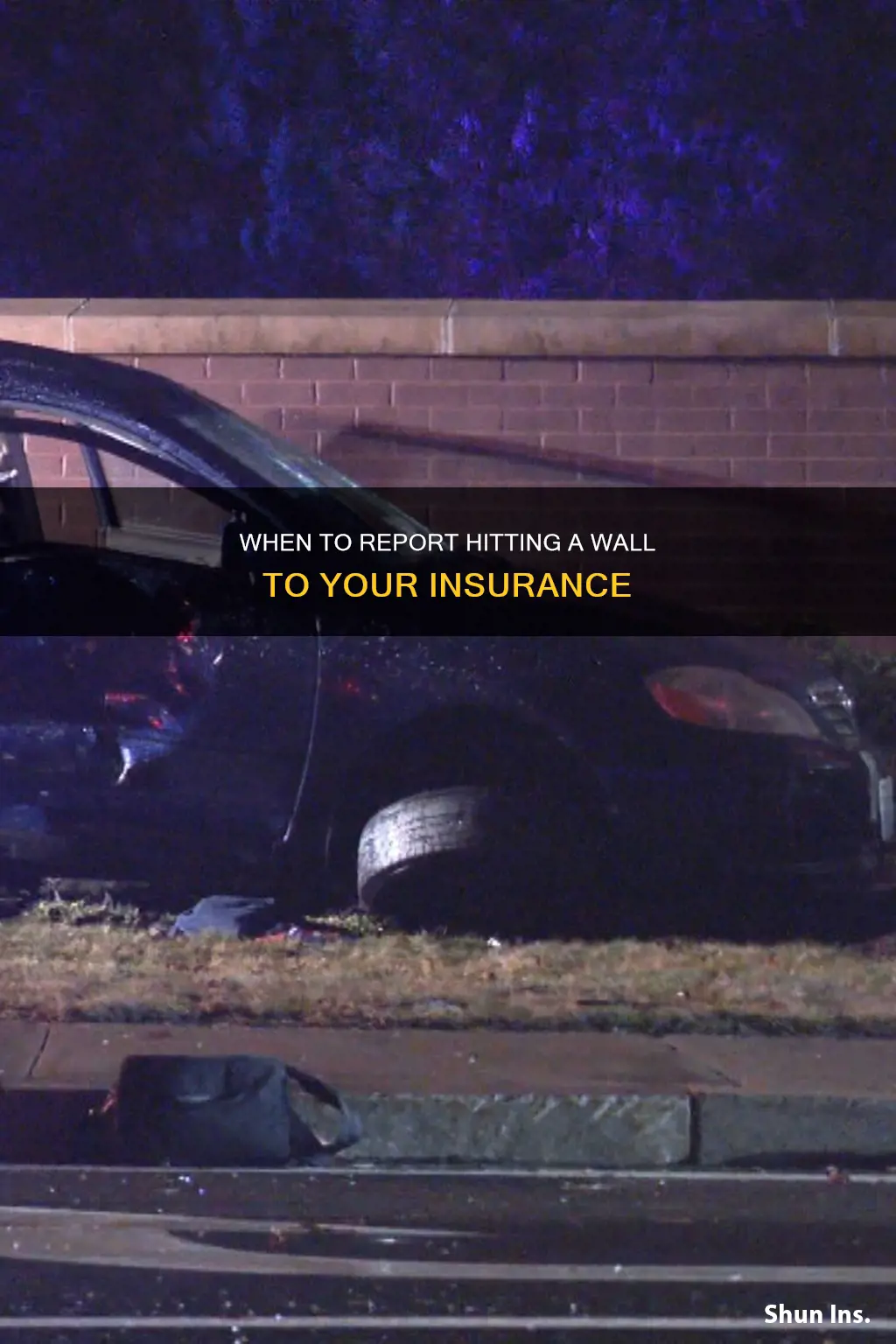

If you've hit a wall with your car, you may be wondering whether or not to report it to your insurance company. This can be a complex situation and the answer may depend on several factors, including the extent of the damage, whether there were any injuries, and who owns the wall. It's important to understand your insurance coverage and the potential implications of filing a claim or not reporting the incident. Even if the damage is minor, it's generally recommended to notify your insurance company to prepare for any potential third-party liability claims and to avoid any legal issues.

| Characteristics | Values |

|---|---|

| Should you report insurance if you hit a wall? | Yes, reporting the incident to your insurance company is recommended, even if you do not intend to file a claim. This helps your insurer prepare for a potential third-party liability claim from the wall's owner. |

| What if you don't own the wall? | Provide the wall owner with your auto insurance information so they can file a third-party claim through your liability property damage coverage. Not doing so could be considered a hit-and-run, leading to legal consequences. |

| What if you own the wall? | File a claim with your homeowner's insurance, which will work with your auto insurer to pursue coverage under your auto liability policy. |

| What if another vehicle caused you to hit the wall? | The other driver's liability coverage should cover the cost of repairing the wall and any injuries, up to their insurance coverage limits. |

| What if there is minor damage? | Filing a claim may not always make sense, especially if the damage is minor, as you will likely be found at fault, and your insurance premium may increase when your policy renews. |

Explore related products

What You'll Learn

![]()

Reporting the incident to your insurance company

If you have hit a wall with your car, you should report the incident to your insurance company. The first thing to do is to make sure that anyone involved in the accident is safe and call the police. Take photos of the incident, including your car and the wall, and note the location, date, time, and any other relevant factors. If you don't own the wall, it is important to identify yourself to the owner and provide them with your auto insurance information so they can file a third-party claim. Not doing so could be considered a hit-and-run, which can have serious legal implications.

If you decide to file a claim with your collision insurance for vehicle damage, your policy can help cover the cost of repairing or replacing your car. However, in a single-vehicle accident, you will typically be found at fault, and you may experience an increase in your insurance premium when your policy renews. Therefore, it may not always make sense to file a claim, especially if the damage is minor.

Even if you choose not to file a claim, it is important to notify your insurance company about the event. This will help your insurer prepare for a potential third-party liability claim filed by the wall's owner. If you own the wall, your homeowners' insurance will work with your auto insurer to pursue coverage under your auto liability policy. In this case, you must submit a separate claim to your homeowner's insurance.

It is always recommended to get in touch with your insurance provider to discuss your options before making a decision. They can advise you on the best course of action based on your specific circumstances.

Farmers Insurance: Positioning for a Potential Acquisition?

You may want to see also

Explore related products

![]()

Collision coverage for damage to your car

Collision coverage is an optional standard auto insurance coverage that helps pay for the cost of repairs to your vehicle if it collides with another object or vehicle. It covers incidents involving objects or other cars and can be used regardless of who is at fault. Collision insurance does not cover damage to another person's vehicle or property, nor does it cover all damage to your vehicle. For example, it does not cover vandalism or theft.

If you have collision coverage and your car hits a wall, your policy may help pay to repair or replace your vehicle. Collision coverage will cover the damages to your vehicle, less your deductible, even if you are considered at fault for the accident. Collision coverage can also be used in the event of a hit-and-run accident where the responsible party flees the scene, or if an unidentified vehicle pushes yours into a wall. In this case, collision coverage can help cover the cost of repairing or replacing your vehicle.

If you don't own the wall, it's important to make sure the owner of the wall gets your auto insurance information so they can file a third-party claim via your liability property damage coverage. Not identifying yourself to the wall's owner could be considered a hit-and-run, resulting in serious legal implications. Your liability coverage will only cover the wall; you will need collision coverage for damage to your vehicle and medical payments coverage or personal injury protection to cover bodily injuries.

It's important to note that collision coverage is not required by state law, and you may not need it if you own an older vehicle. Choosing not to purchase collision coverage leaves you financially responsible for repairing or replacing your vehicle in the event of a collision. However, if your vehicle is financed or leased, your lienholder may require you to have collision and comprehensive coverage to protect their investment.

Home Hazard Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Third-party liability claims

If you hit a wall with your car, you should notify your insurance company about the incident. This will help them prepare for a potential third-party liability claim from the wall's owner. If you own the wall, your homeowners insurance will collaborate with your auto insurer to pursue coverage under your auto liability policy.

If you don't own the wall, make sure to provide the wall's owner with your auto insurance information so they can file a third-party claim via your liability property damage coverage. Not doing so could be considered a hit-and-run, resulting in serious legal consequences.

The other driver's liability coverage should cover the cost of repairing the wall, your car, and any injuries to you or your passengers, up to their liability coverage limits. If the other driver did not physically collide with you but you hit a wall while trying to avoid their vehicle, the claims process may be more complex. Insurers will assess the police report to assign fault for the damage caused.

If you decide not to file a claim for damage to your car, your medical payments coverage or personal injury protection (PIP) may still be able to provide reimbursement for any injuries you or your passengers suffer as a result of the collision with the wall.

Understanding Farmers Insurance for Planting: A Guide to Agricultural Coverage

You may want to see also

Explore related products

![]()

Hit-and-run implications

If you hit a wall and flee the scene without providing your insurance information, this could be considered a hit-and-run. The implications of a hit-and-run vary depending on the jurisdiction and the circumstances of the incident. In some places, a hit-and-run is considered a criminal offence, which can result in fines, imprisonment, or both. For example, in Canada, a hit-and-run is punishable by up to 5 years in prison. In Georgia, a hit-and-run resulting in vehicle damage or non-serious injuries is a misdemeanour, carrying up to 12 months of imprisonment. If the accident causes serious injury or death, it becomes a felony with a penalty of 1 to 5 years in prison.

In addition to criminal penalties, a hit-and-run can also result in administrative penalties, such as the suspension or revocation of your driver's license. In some jurisdictions, a hit-and-run can even lead to a lifetime revocation of a driver's license. Furthermore, insurance companies often increase insurance costs or void the policies of drivers involved in a hit-and-run.

It is important to note that the definition of a hit-and-run can vary. In most states, a hit-and-run is committed simply by leaving the scene of an accident, regardless of whether the driver caused the accident or not. However, in certain states, the driver must have known or had reason to know that the accident occurred and the resulting injuries or property damage for it to be considered a hit-and-run. Additionally, some states include collisions with animals in the definition of a hit-and-run.

Reporting Insurance Recovery to the IRS: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Medical coverage for injuries

If you've been in an accident and have hit a wall, it's important to understand what your insurance will cover. If you have collision insurance, your policy can help cover the cost of repairing or replacing your vehicle. You will need to submit a claim to your insurance company, and the specifics of what is covered will depend on the details of your policy.

If you or your passengers have sustained injuries, your medical payments coverage or personal injury protection (PIP) may be able to provide reimbursement for any medical costs incurred. If you don't have medical payments coverage or personal injury protection, your health insurance may cover your medical costs. However, your health insurance company may seek reimbursement if you receive money from the at-fault driver's insurer or another source. Additionally, certain treatments may not be covered by your health insurance.

If you don't own the wall, it is important to provide the owner with your auto insurance information so they can file a third-party claim through your liability property damage coverage. Your liability coverage will typically only cover the damage to the wall, not any bodily injuries. If another driver was involved in the accident, their liability coverage should cover the cost of repairing the wall, your vehicle, and any injuries, up to their liability coverage limits.

It is important to notify your insurance company about the accident, even if you choose not to file a claim. This will help prepare for any potential third-party liability claims and ensure you are following the terms of your policy. It is also recommended to document the incident by taking photos and recording the location, date, time, and any other relevant details.

Farmers Insurance Group: Is 21st Century Insurance Included?

You may want to see also

Frequently asked questions

Take photos of the incident, including your car and the wall, as well as noting the location, date, and time. If there are any injuries, ensure that the injured are safe and call the police. If you don't own the wall, contact the owner and provide them with your auto insurance information.

Yes, it is always better to notify your insurance company about the event. This will help prepare for any third-party liability claims that may be filed by the wall's owner.

Yes, your insurance premium will likely increase in most cases after hitting a wall. However, it is still recommended to contact your insurance company to discuss the specifics of your situation.

If the wall is on your property, you must submit a separate claim to your homeowner's insurance. This will allow your homeowner's insurance to work with your auto insurer to pursue coverage under your auto liability policy.

The other driver's liability coverage should cover the cost of repairing the wall and your vehicle, as well as any injuries, up to their liability coverage limits. Provide the other driver's insurer and the police with all the information you have about the incident, including evidence of damages and injuries.

![Collision [DVD + Digital]](https://m.media-amazon.com/images/I/910WYFKVLCL._AC_UY218_.jpg)